Excellent performance is one reason private market AUM reached all-time highs in the first half of 2021, just under $10 trillion.1 But as more investors look to diversify their portfolios with these illiquid assets, more realize a significant challenge: data.

In public markets, investors typically utilize performance that is marked-to-market, in real-time, and daily. On the other hand, private market performance is typically smoothed, marked-to-value, lagged relative to public markets, and infrequent. Smoothed private asset returns may also artificially lower volatility and reduce the explainability of risk, the latter being an important and often overlooked consequence of smoothing. For investors looking to holistically analyze a portfolio that includes private assets, especially alongside public market investments, this data limitation poses a significant hurdle.

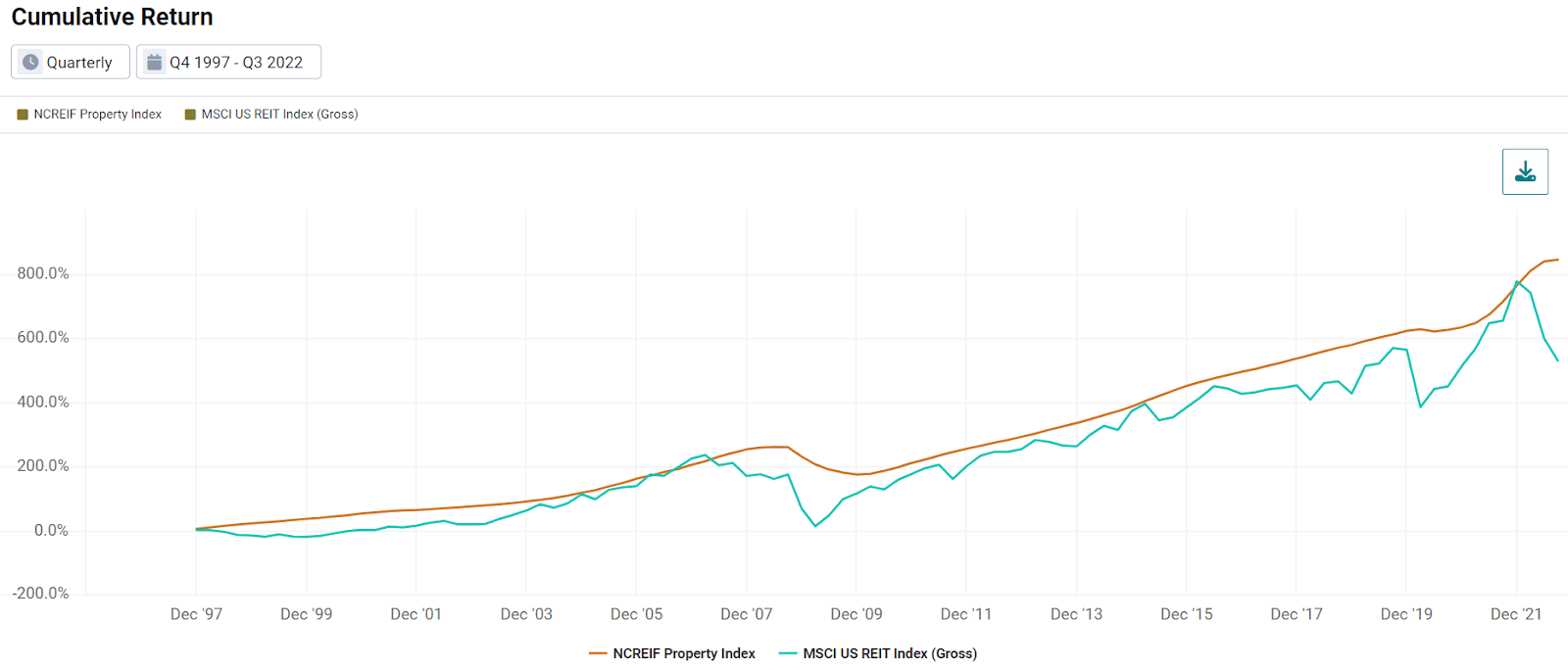

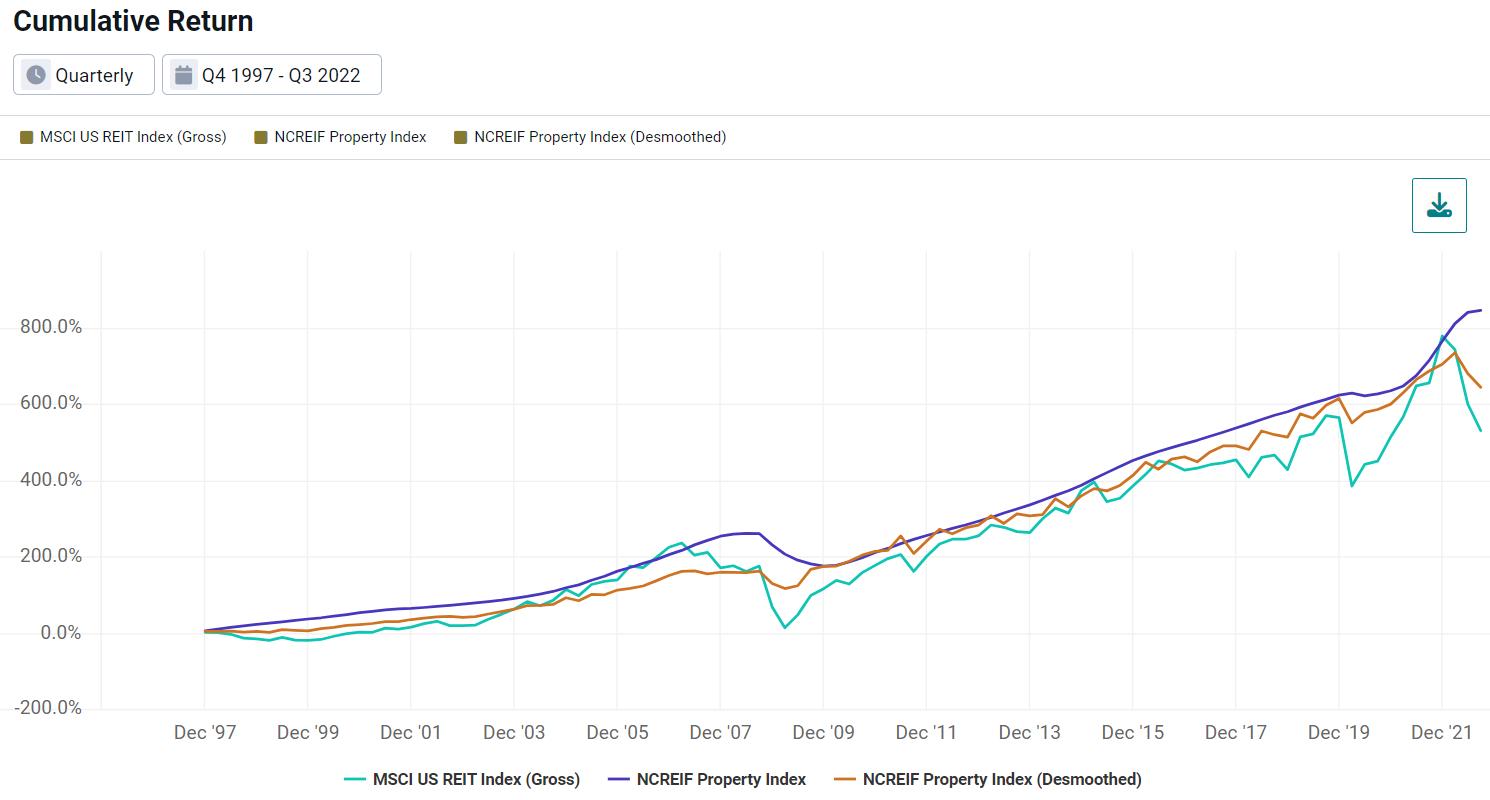

Take a classic private real estate example such as the NCREIF Property index and a public proxy.2 Focusing on the 2009 rebound, we see how private real estate began an upward movement multiple quarters after that of the public proxy. This is despite the notion that they are probably driven by the same movements in common risk factors, such as economic growth and interest rates.

Exhibit 1: Smoothed Private Real Estate Has Lagged Public Markets

Source: Venn by Two Sigma, Bloomberg. Period from Q4 1997 to Q3 2022. The NCREIF Property index represents private real estate while the MSCI US REIT index represents the public proxy.

Additionally, over this period the private real estate index exhibited a volatility of just 4.42% while the public proxy’s volatility was 21.13%. Understanding that these differences are not likely real, but rather the outcome of smoothed and infrequent private data, promotes a call to action.

How to View Private Asset Data Through a Public Lens

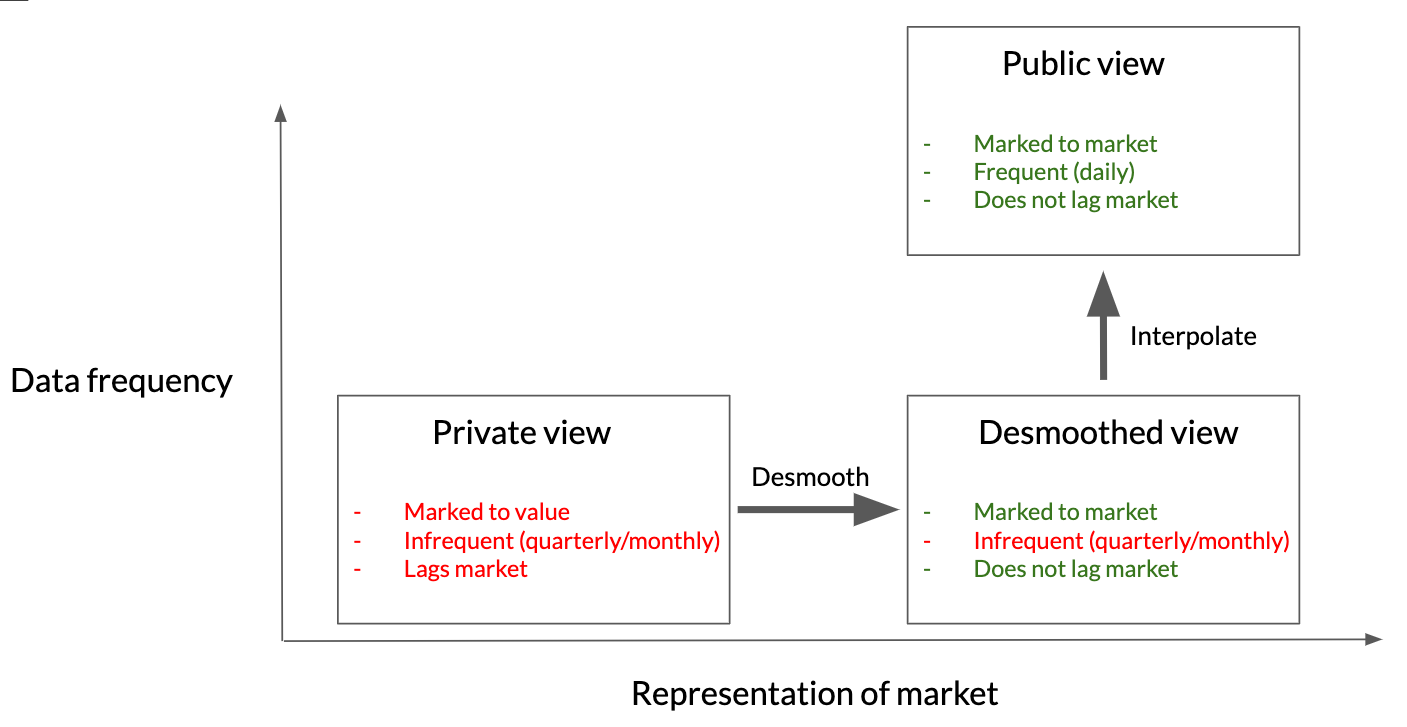

Public market data is frequent and marked to market. As a result, one way to potentially improve the quality of private asset returns is by making them look and feel more like a public market proxy. To accomplish this goal, Venn uses two statistical methods: desmoothing and interpolation.

Below you can see the role that each method plays on the journey to viewing private asset returns with a public lens. Specifically, desmoothing aims to reduce private market performance lag and mark it to the market, while interpolation aims to increase the frequency of data.

Exhibit 2: Utilizing Desmoothing and Interpolation to Take a Public View

Source: Venn by Two Sigma. For illustration purposes only.

More About Desmoothing

When we desmooth private asset returns, we follow the econometric model by Getmansky, Lo, and Marakov (2004).3 Put simply, we attempt to reverse-engineer the smoothing process by looking at the smoothed private asset performance and its regression-based relationship with an appropriate public market proxy.

What are some measures of success for a desmoothed return stream?

- An increase in volatility: Desmoothing returns may increase volatility by adjusting them to more accurately reflect public market volatility.

- A decrease in autocorrelation: High autocorrelation is a natural bias of smoothing. Decreasing the absolute magnitude of autocorrelation better reflects market reactions (by moving it closer to the autocorrelation of the public proxy) and indicates that past returns are now less similar to future returns.

- A decrease in residual contribution to risk: Venn’s Two Sigma Factor Lens is holistic, aiming to explain a large degree of portfolio variation. Smoothed private asset returns represent an unnatural market process that leads to larger amounts of unexplainable risk (residual). Desmoothing may reduce this unexplainable risk.

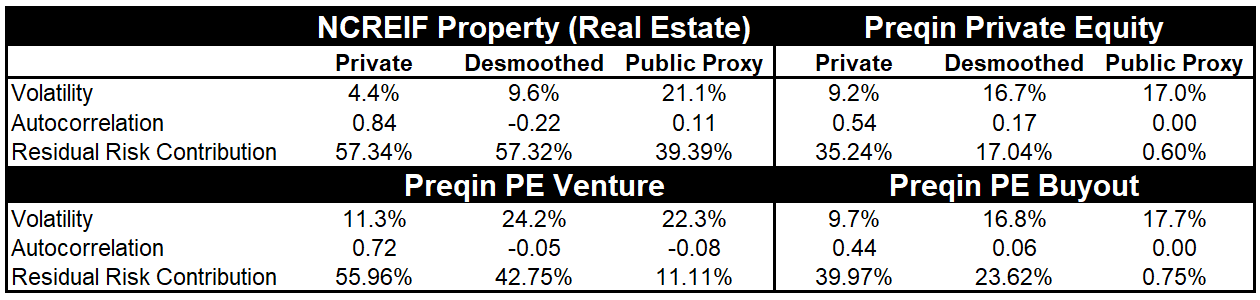

Given these three measures of potential success, we tested Venn’s desmoothing process on private real estate, equity, buyouts, and venture capital, and summarized our results below in Exhibit 3. In every instance, changes in all three measures met our expectations with volatility increasing, and autocorrelation and residual risk contribution decreasing.

Exhibit 3: Results From Desmoothing Various Private Asset Indexes

Source: Venn by Two Sigma, Bloomberg. Real Estate analysis from Dec 1997–Sep 2022. All other analysis from March 2001–March 2022. Public proxies are based on Preqin’s Public Market Equivalent “Pro Tips" and are as follows: Real Estate: MSCI US REIT index (4 lags used). Private Equity: S&P 500 index (4 lags used). PE Buyout: Russell 3000 index (4 lags used). PE Venture Capital: Russell 2000 index (5 lags used).

Using our example from Exhibit 1, below we show the output of our desmoothing feature on the private real estate time series. Notice how the orange line now rebounds at the same time as the public proxy in 2009.

Exhibit 4: Results from Desmoothing on Private Real Estate

Source: Venn by Two Sigma, Bloomberg. Period from Q4 1997 to Q3 2022. 4 lags used for desmoothing.

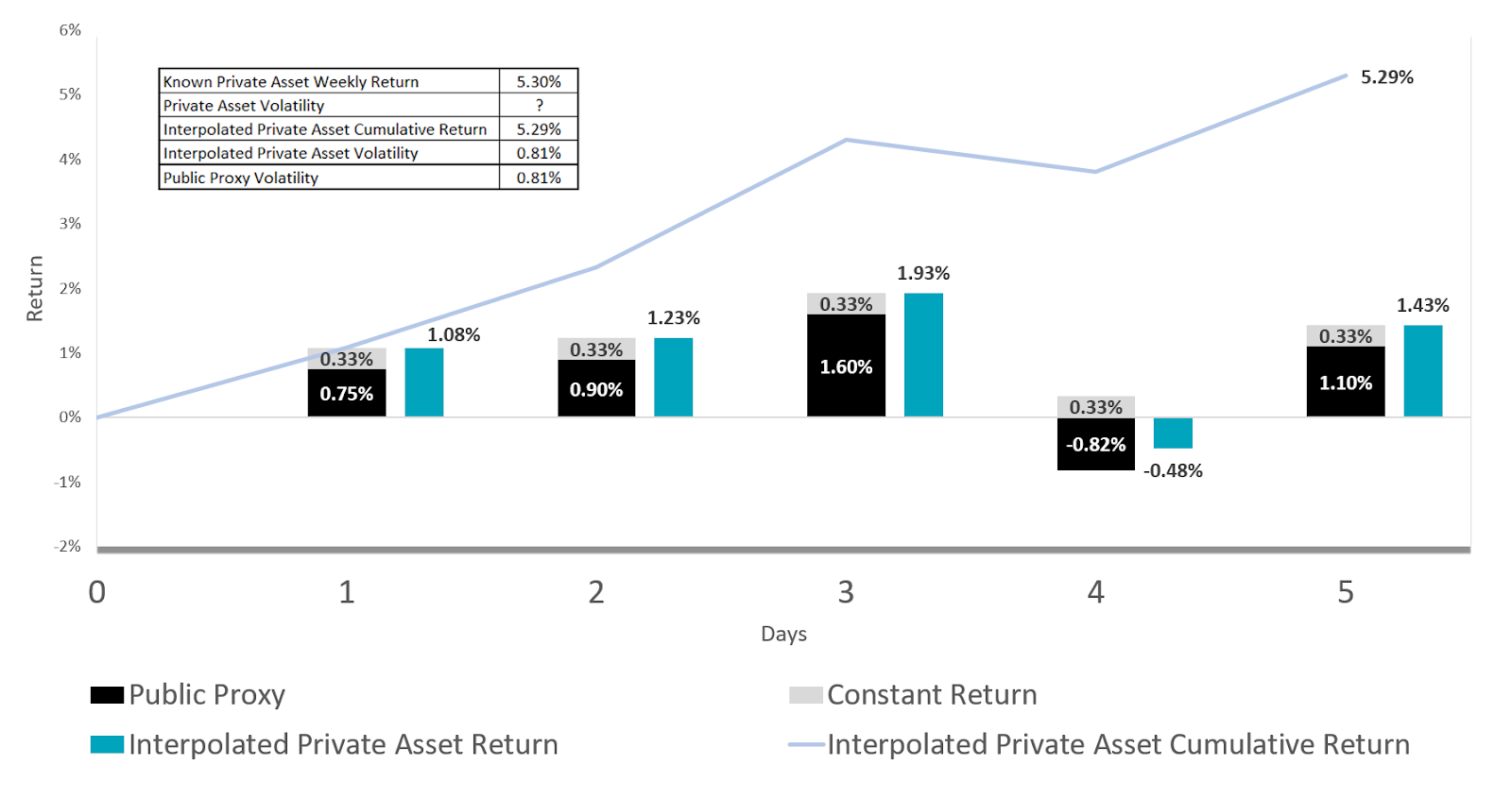

More About Interpolation

Despite the illustrated success of our desmoothing results, increasing the frequency of private asset returns is a separate task. Especially when considering consistency across data sets, it can be useful for allocators to convert their quarterly private assets returns into daily.

When interpolating, Venn:

- Adds a constant daily return to the chosen public proxy, such that taking the cumulative return should closely match the private asset’s return. Venn then uses that new daily return stream for the private asset. Below we provide an illustrative example of interpolation over a one week period.

Exhibit 5: Illustrative Example of Interpolation Over One Week

Source: Venn by Two Sigma. For illustration purposes only.

Our expectation is that the resulting, now-daily return series will approximate the original private asset’s return, but with a volatility that roughly matches the chosen public proxy.

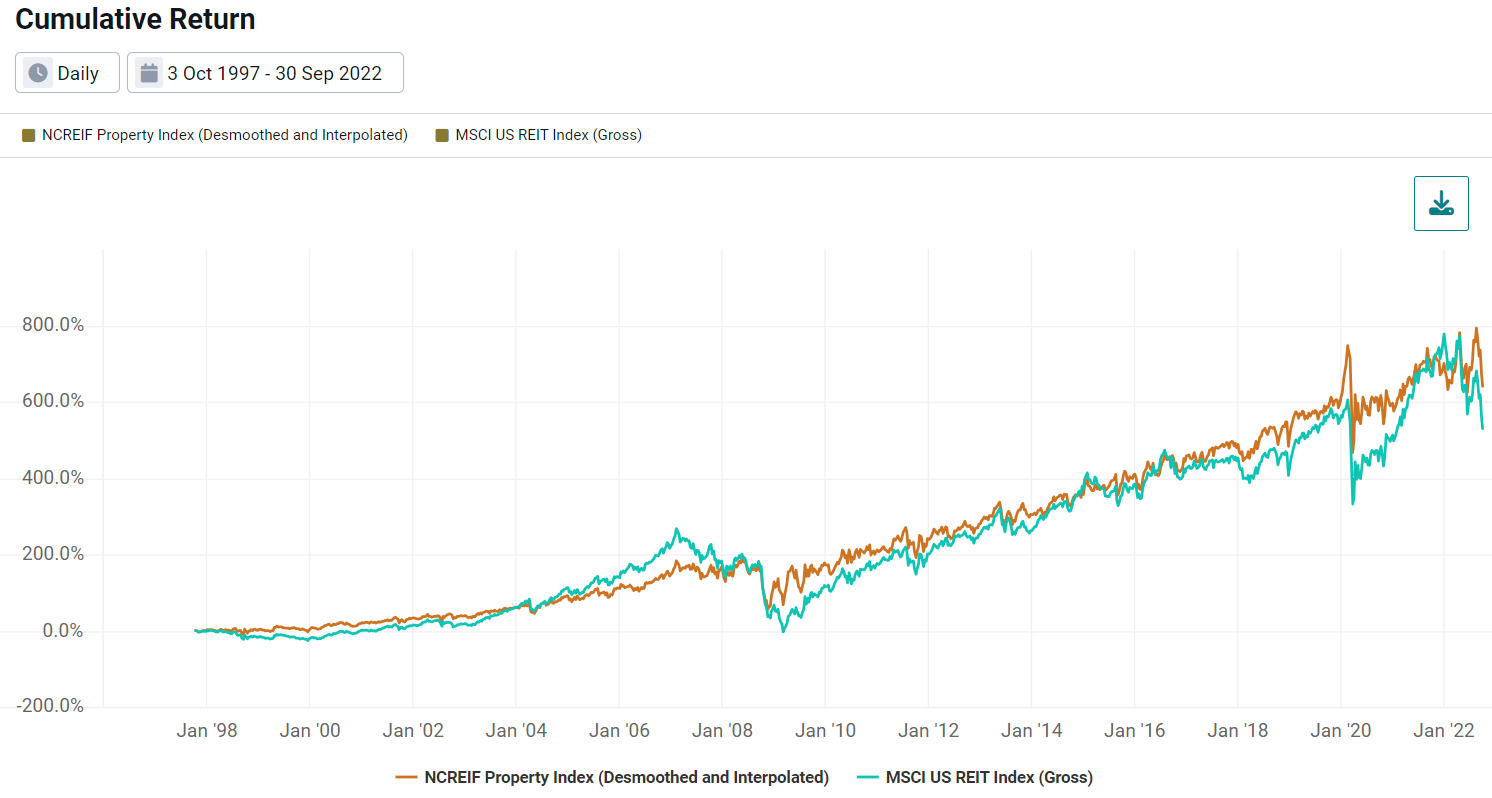

In Exhibit 6 we show the output of both desmoothing and interpolation on private real estate. Notice how this once smoothed quarterly time series now experiences market timing in-line with the public proxy from desmoothing, along with daily volatility incorporated from interpolation.

Exhibit 6: Results from Desmoothing and Interpolation on Private Real Estate

Source: Venn by Two Sigma, Bloomberg. Period from 10/3/1997 to 9/30/2022. 4 lags used for desmoothing.

(De)Smoother Sailing When It Comes to Private Asset Returns

Using Venn’s desmoothing technique on private asset returns, we revealed higher volatility while decreasing autocorrelation and residual risk contribution. Additionally, using interpolation, we were able to transform infrequent data into daily data.

Given that our clients continue to leverage Venn for multi-asset portfolio analytics, we are pleased they can use these features to view private assets with a familiar public lens. This may allow investors to better understand levels, timing and drivers of risk, but also may improve operational logistics when working with other daily holdings in the context of a multi-asset portfolio. When looking to conduct portfolio analytics that include private asset returns, we believe these two steps make for smoother sailing via a unified public lens.

View Full Recording of our Private Asset Lab Webinar Here

Proxies are for estimation purposes only and have many inherent limitations. The methodology for calculating potential proxies was chosen in our professional judgment, and will not always yield the most accurate available proxy. Our potential proxy suggestions are not a recommendation as to any portfolio, allocation, strategy, or investment nor an offer to purchase or sell any security. We suggest users do their own research to use the public proxy that best fits their own use case.

Exposure to risk factors is not a guarantee of increased performance or decreased risk. Past performance does not guarantee future results. This document presentation is for informational purposes only. Click here for Important Disclosure and Disclaimer Information.

References

1 For example, the Preqin Private Equity Index returned 36.5% in 2021 versus the Russell 3000 at 25.7%. It is important to note that these numbers are delayed and do not capture the drawdown generally seen in markets in 2022. Aum source: read more here.

2 Public proxy is the MSCI US REIT index.

3 Getmansky, Mila, Andrew W. Lo, and Igor Makarov. "An econometric model of serial correlation and illiquidity in hedge fund returns." Journal of Financial Economics 74.3 (2004): 529-609.

This article is not an endorsement by Two Sigma Investor Solutions, LP or any of its affiliates (collectively, “Two Sigma”) of the topics discussed. The views expressed above reflect those of the authors and are not necessarily the views of Two Sigma. This article (i) is only for informational and educational purposes, (ii) is not intended to provide, and should not be relied upon, for investment, accounting, legal or tax advice, and (iii) is not a recommendation as to any portfolio, allocation, strategy or investment. This article is not an offer to sell or the solicitation of an offer to buy any securities or other instruments. This article is current as of the date of issuance (or any earlier date as referenced herein) and is subject to change without notice. The analytics or other services available on Venn change frequently and the content of this article should be expected to become outdated and less accurate over time. Any statements regarding planned or future development efforts for our existing or new products or services are not intended to be a promise or guarantee of future availability of products, services, or features. Such statements merely reflect our current plans. They are not intended to indicate when or how particular features will be offered or at what price. These planned or future development efforts may change without notice. Two Sigma has no obligation to update the article nor does Two Sigma make any express or implied warranties or representations as to its completeness or accuracy. This material uses some trademarks owned by entities other than Two Sigma purely for identification and comment as fair nominative use. That use does not imply any association with or endorsement of the other company by Two Sigma, or vice versa. See the end of the document for other important disclaimers and disclosures. Click here for other important disclaimers and disclosures.

This article may include discussion of investing in virtual currencies. You should be aware that virtual currencies can have unique characteristics from other securities, securities transactions and financial transactions. Virtual currencies prices may be volatile, they may be difficult to price and their liquidity may be dispersed. Virtual currencies may be subject to certain cybersecurity and technology risks. Various intermediaries in the virtual currency markets may be unregulated, and the general regulatory landscape for virtual currencies is uncertain. The identity of virtual currency market participants may be opaque, which may increase the risk of market manipulation and fraud. Fees involved in trading virtual currencies may vary.