The Science of Finance

Venn is now part of Solovis, bringing together industry leading portfolio analytics and factor analysis for sophisticated investors.

Find out why clients of all sizes rely on us for our global multi-asset analytics, intuitive interface, and premium client service.

Select Clients*

The Power of Venn

Our SOC 2 certified platform offers a modern and intuitive approach to solving problems. Use Venn to:

- Analyze Public and Private Investment Options

- Conduct Manager Due Diligence

- Optimize Portfolio Construction

- Design Compelling Reports and Presentations

Thought Leadership

Market, Industry, and Analytical Insights

Client Spotlight

Ares Wealth Management Solutions needed a tool to help gain a more precise view of portfolio risk and diversification beyond traditional Excel-based models.

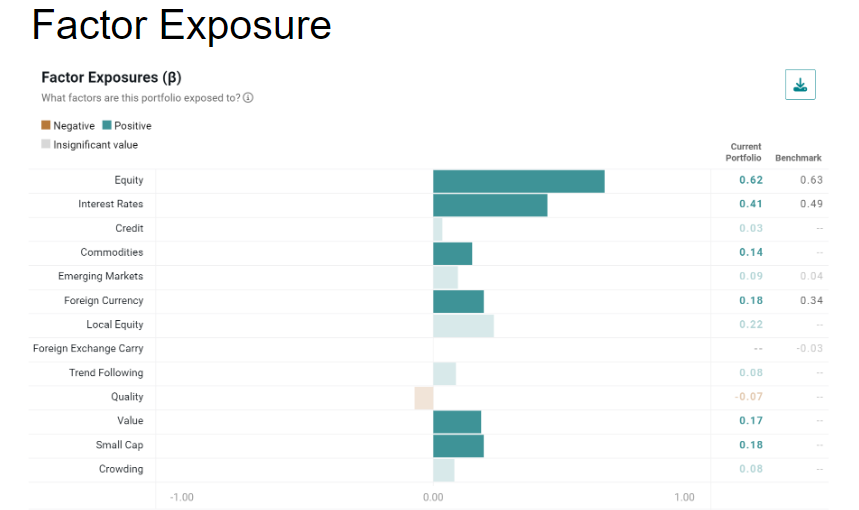

Analyzing Private Assets

Private asset returns are typically smoothed and infrequent, reducing transparency. Venn tools can help private assets look and feel more like a public market proxy.

Incorporating a Total Portfolio Approach

Incorporating a total portfolio mindset to asset allocation can give a broader and more precise view of risk and return drivers than an asset class approach alone.