Earlier this year we provided readers with two easy steps to view their private asset returns through a public lens. During our discussion, we reviewed the data challenges associated with private asset returns, as well as how desmoothing and interpolation techniques adjust private assets to account for movements in public markets. By combining these techniques, we showed how investors could reveal truer timing and levels of volatility, improve risk factor explainability, and increase data frequency to daily.1

Using these adjusted private asset returns, one can seamlessly integrate private and public assets together into holistic multi-asset portfolio analysis. However, private asset managers often report their valuations with a significant lag, such that their up-to-date data virtually never aligns with public markets. To address this, we are introducing extrapolation, or what we believe is the final piece to the puzzle to view private asset returns through a public lens.

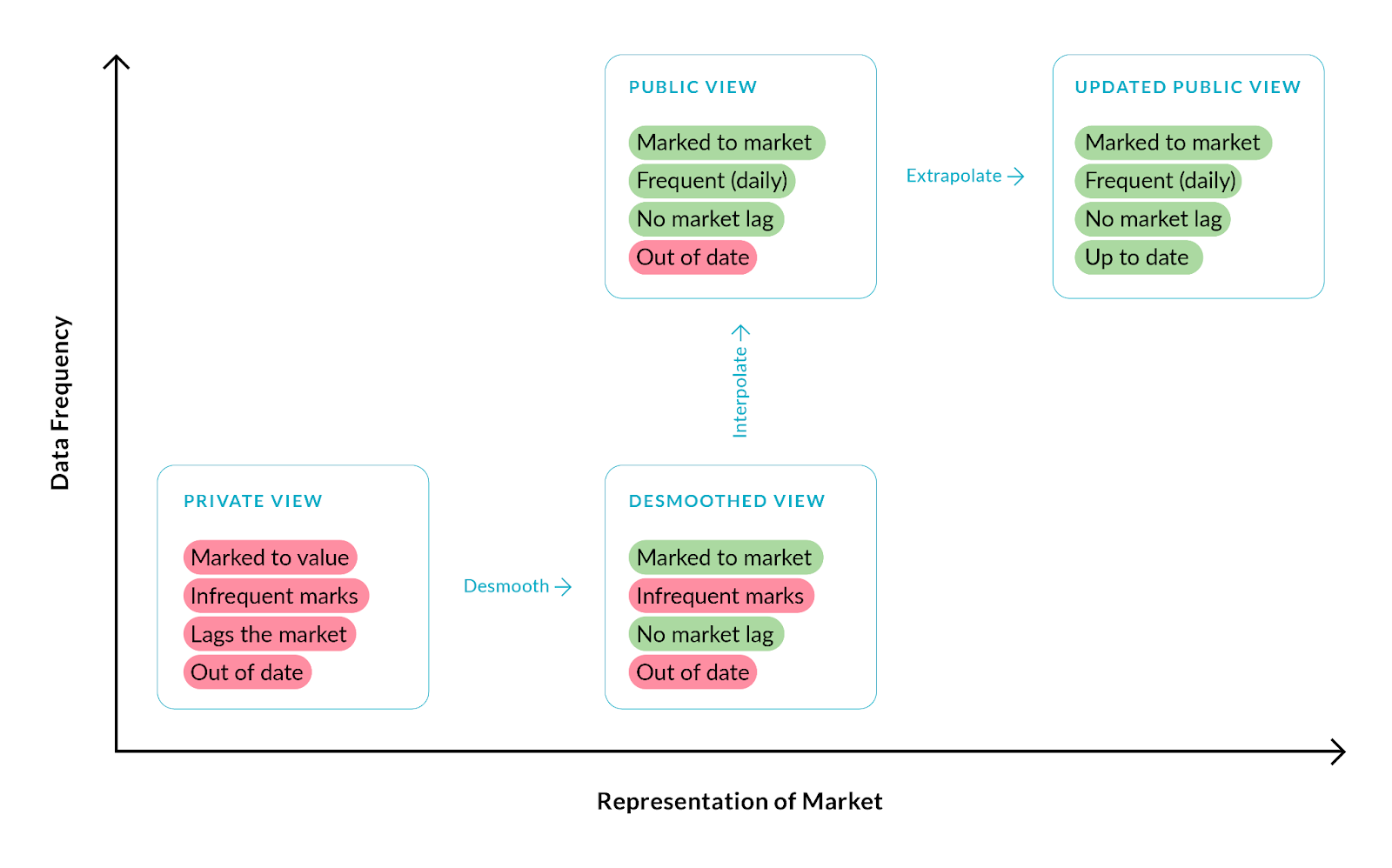

Exhibit 1: Introducing Extrapolation for Private Asset Returns

Source: Venn by Two Sigma. For illustration purposes only.

A Private Equity Case Study

Take, for example, the Preqin Private Equity index, which typically has artificially low volatility, exhibits delayed market reactions, is at a quarterly frequency, and can be out of date for quarters at a time. As we show below, desmoothing and interpolation helped to solve the first three of these issues by using the S&P 500 as a public proxy.2 However, the issue of out-of-date data remains with a current end date for the Preqin index of March 2023 (with this writing as of the end of July).

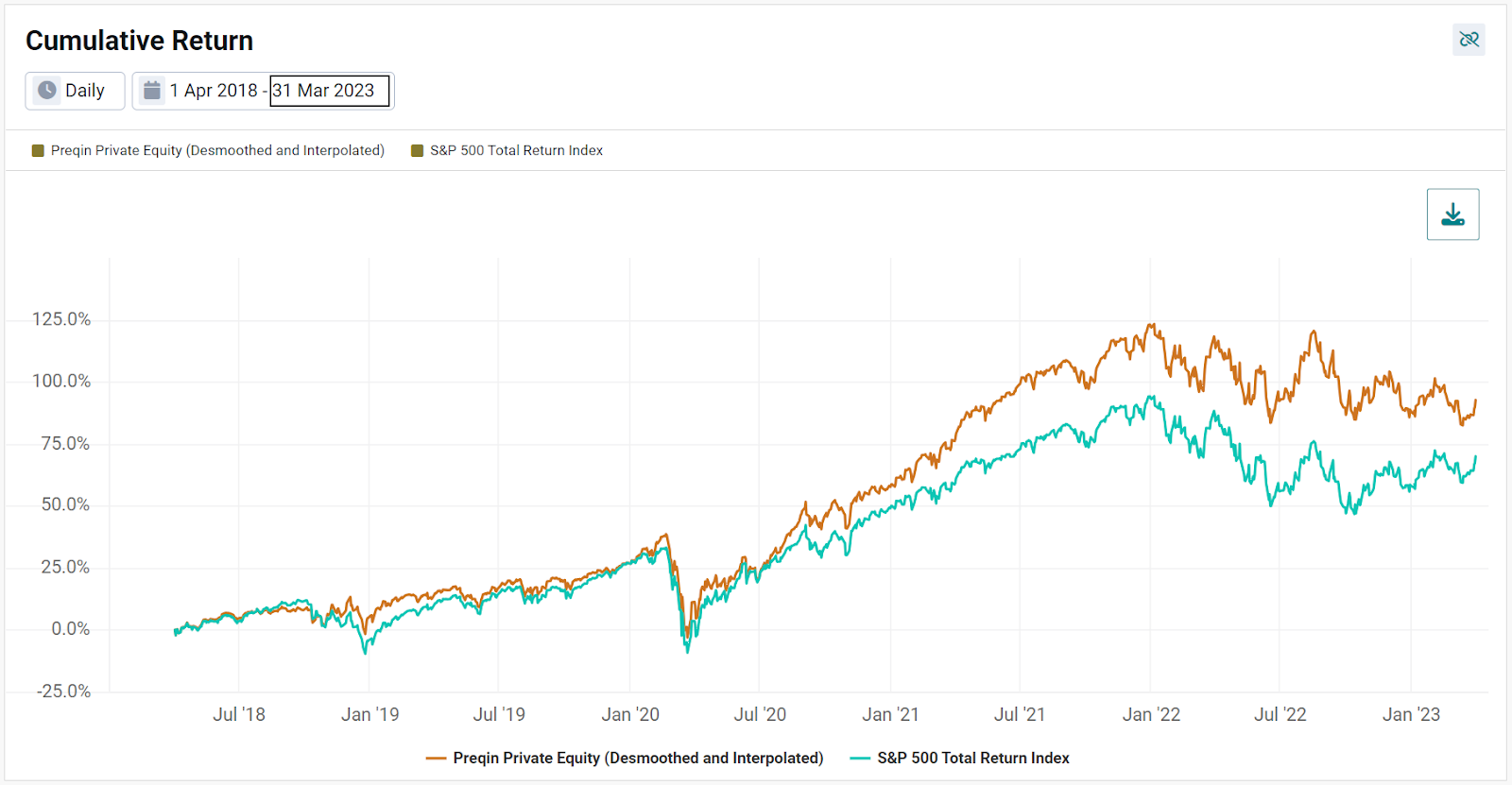

Exhibit 2: Desmoothed and Interpolated Preqin Private Equity Index, Trailing 5-Years

Source: Venn by Two Sigma. Public proxy used for desmoothing and interpolation on the Preqin Private Equity index was the S&P 500.

The early end date is especially problematic when trying to conduct multi-asset portfolio analysis where you are limited by the holdings with the least history. In this example, even if this private equity exposure was only 1% weight in our portfolio, we would be forced to conduct all analysis through March of 2023, a lag of more than four months. This is where extrapolation, or an educated estimate of missing valuations, can be a powerful tool to conduct portfolio analysis despite out-of-date data.

Extrapolation

Venn’s extrapolation feature provides up-to-date valuations for assets using a public proxy. Similar to desmoothing and interpolation, the spirit of leveraging a public proxy to estimate missing valuations is based on a belief that private markets are indeed exposed to many of the same systematic risk factors as public markets. Put another way, a private equity investment should react to shocks in risk factors, like economic growth or interest rates, much in the same way a public investment should.

As a result of this belief, we use regression techniques between historical private asset returns and a public market proxy to estimate where that private asset may be valued today. This results in estimated returns that may look and feel like the public proxy, but with an adjustment for the return that is unique to the private asset. Because those returns can first be desmoothed and interpolated, we believe the end result is an up-to-date public view that can help investors more accurately conduct multi-asset portfolio analysis or individual manager due diligence.

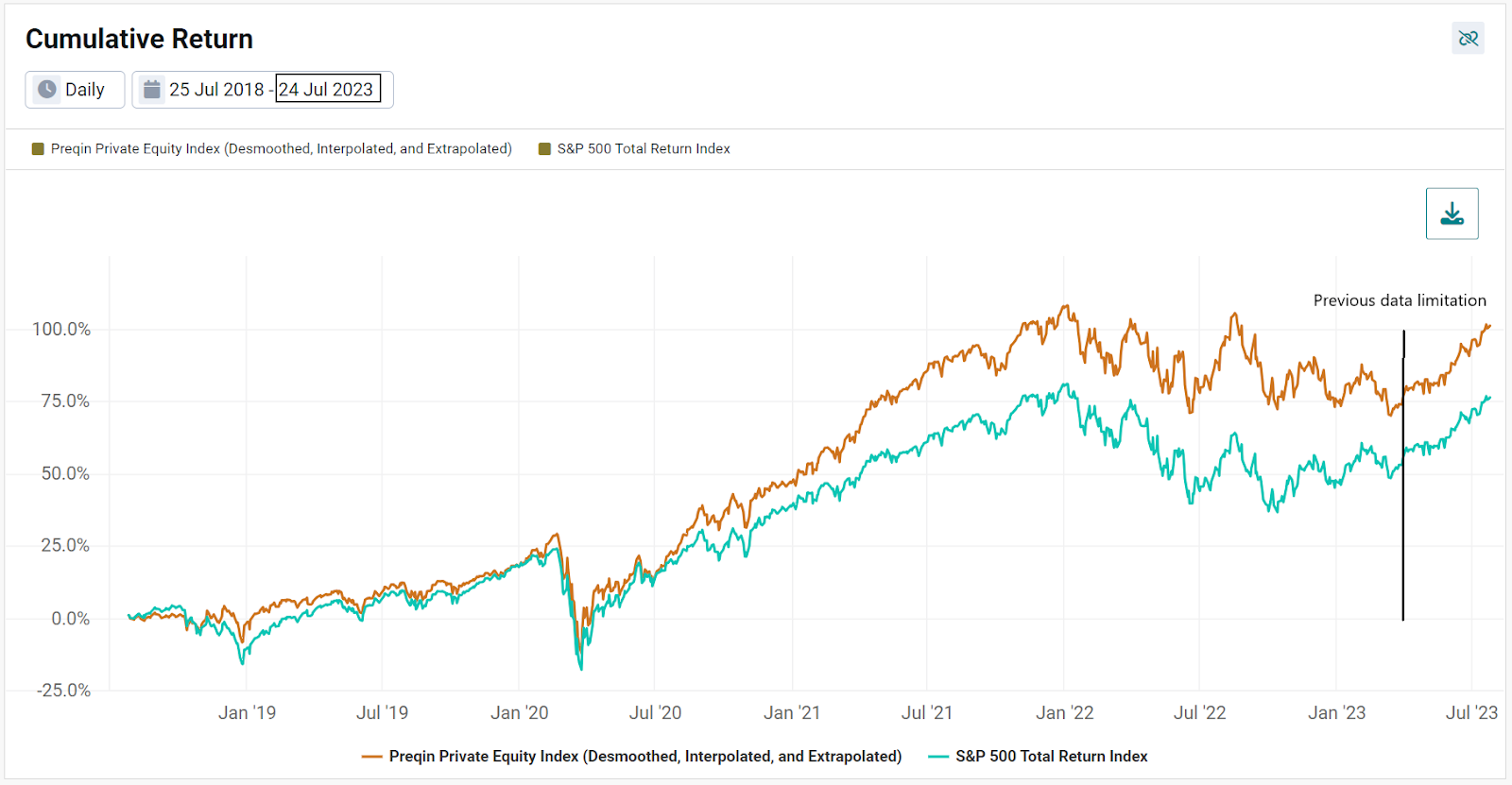

In Exhibit 3, we show the Preqin Private Equity index after desmoothing, interpolation, and extrapolation. Notice it does not have artificially low volatility or lag the market, is at a daily frequency, and importantly, is up to date. Extrapolating investment returns may be especially important in today's market environment due to the stark contrast between negative equity performance in 2022 and the rally we’ve seen thus far in 2023. The chart below illustrates how significantly markets rallied over the period that uses extrapolation, information that was not previously available.

Exhibit 3: Desmoothed, Interpolated, and Extrapolated Preqin Private Equity Index, Trailing 5-Years

Source: Venn by Two Sigma

Three Easy Steps to Take Your Private Asset Returns Public

Given that our clients continue to leverage Venn for multi-asset portfolio analytics, we are pleased they can use desmoothing, interpolation, and extrapolation features to view private assets with a familiar public lens.

All three together may allow investors to better understand levels, timing, and drivers of risk, while also improving operational logistics. We see the biggest benefit of using these techniques is to provide an easy path to analyzing private and public investments side by side in a multi-asset portfolio. If you are interested in adding desmoothing, interpolation, and/or extrapolation to your Venn subscription, please contact your account representative.3

View Full Recording of our Private Asset Lab Webinar Here

Extrapolation is for estimation purposes only and has many inherent limitations. Venn’s extrapolation methodology was developed in our professional judgment based on numerous assumptions and may not accurately forecast the value of a security, portfolio or investment. Extrapolation results are not a recommendation to buy, sell or hold any security, portfolio or investment or a recommendation of any investment strategy.

References

1 The increase of data frequency to daily is a function of interpolation. Interpolation adds a constant daily return to the chosen public proxy returns, such that taking the cumulative return should closely match the private asset’s return. Venn then uses that new daily return stream for the private asset

2 You can learn more about desmoothing and interpolation in the article we mentioned at the beginning of this piece: “Two Easy Steps to Take Your Private Asset Returns Public.”

3Additional fees may apply.

This article is not an endorsement by Two Sigma Investor Solutions, LP or any of its affiliates (collectively, “Two Sigma”) of the topics discussed. The views expressed above reflect those of the authors and are not necessarily the views of Two Sigma. This article (i) is only for informational and educational purposes, (ii) is not intended to provide, and should not be relied upon, for investment, accounting, legal or tax advice, and (iii) is not a recommendation as to any portfolio, allocation, strategy or investment. This article is not an offer to sell or the solicitation of an offer to buy any securities or other instruments. This article is current as of the date of issuance (or any earlier date as referenced herein) and is subject to change without notice. The analytics or other services available on Venn change frequently and the content of this article should be expected to become outdated and less accurate over time. Any statements regarding planned or future development efforts for our existing or new products or services are not intended to be a promise or guarantee of future availability of products, services, or features. Such statements merely reflect our current plans. They are not intended to indicate when or how particular features will be offered or at what price. These planned or future development efforts may change without notice. Two Sigma has no obligation to update the article nor does Two Sigma make any express or implied warranties or representations as to its completeness or accuracy. This material uses some trademarks owned by entities other than Two Sigma purely for identification and comment as fair nominative use. That use does not imply any association with or endorsement of the other company by Two Sigma, or vice versa. See the end of the document for other important disclaimers and disclosures. Click here for other important disclaimers and disclosures.

This article may include discussion of investing in virtual currencies. You should be aware that virtual currencies can have unique characteristics from other securities, securities transactions and financial transactions. Virtual currencies prices may be volatile, they may be difficult to price and their liquidity may be dispersed. Virtual currencies may be subject to certain cybersecurity and technology risks. Various intermediaries in the virtual currency markets may be unregulated, and the general regulatory landscape for virtual currencies is uncertain. The identity of virtual currency market participants may be opaque, which may increase the risk of market manipulation and fraud. Fees involved in trading virtual currencies may vary.