The key issue we wanted to address was that for many years, investors had been

relying on the assumption that combining different asset classes within a portfolio

was an effective way to maximize risk-adjusted returns. We believe, however, that

different asset classes may be exposed to the same systematic sources of risk,

or factors, which may lead an investor to believe that they are more diversified

than they actually are. In contrast, examining a portfolio through a factor lens may

identify overlapping sources of risk across asset classes. We believe that this allows

for more efficient management of portfolio risk and expected return.

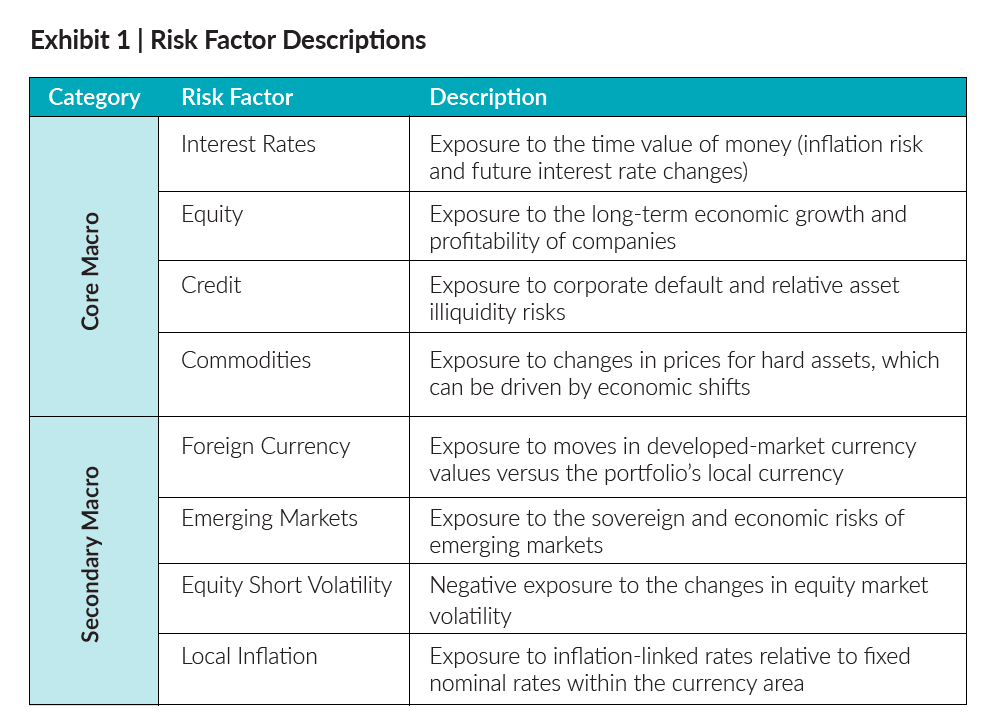

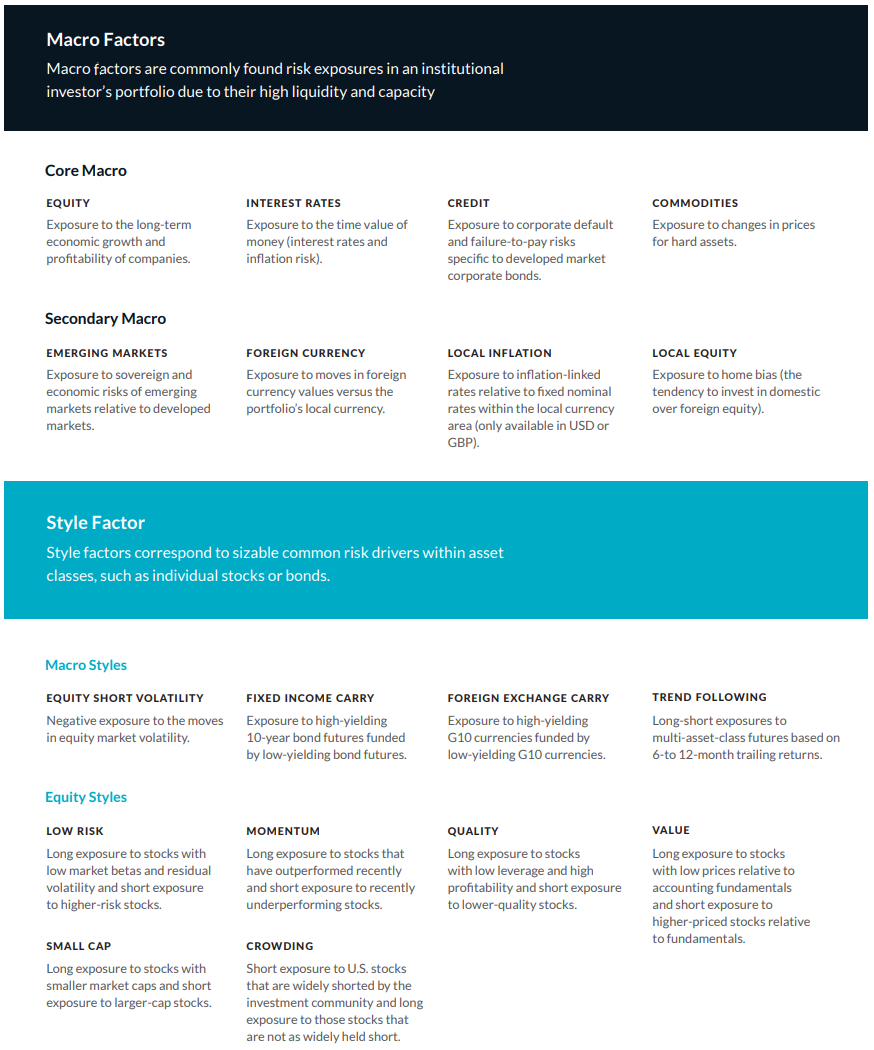

We debuted the Two Sigma Factor Lens with a set of 8 factors, split across Core

Macro and Secondary Macro categories. These original factors were specifically

designed to analyze multi-asset portfolios and were derived from returns of broad,

liquid, asset class proxy indexes (Exhibit 1 below).

Through the Two Sigma Factor Lens, we wanted to provide a set of actionable

factors that could collectively explain much of the cross-sectional and time-series

risk in typical portfolios.

Our 2018 paper went into detail on how to construct and assess these factors,

as well as how we could extend our lens to include additional factors that might

capture new sub-asset class or cross-sectional risks. The factor lens we laid out in

this paper, and our ongoing work to expand it, also formed the foundations of our

VennTM platform. Venn was originally designed as a cloud-based investment analysis

software, helping institutional investors evaluate and manage their multi-asset

class portfolios.

In the years since, we have extended the lens to include an additional 10 factors,

which we split between two new groupings: Macro Styles and Equity Styles. We

wanted to add new factors that could increase the explanatory power of the Factor

Lens by covering less common, but still sizable drivers of portfolio risk. These

additions were crafted to be orthogonal to existing factors, while still following

a similar research and construction methodology. Together, this expanded set of

factors was intended to even better capture and explain the risk attribution of

investment portfolios.

As our Factor Lens continued to expand, so too did the Venn platform. Venn was

officially launched to the external investment community in 2019, and has seen

broad-based growth in clients since. Originally designed for institutional allocators,

Venn soon expanded its client base to also include teams at: wealth managers,

family offices, asset managers, insurance companies, and investment consultants.

For many Venn clients, the platform became their entry point to a more transparent

understanding of risk across their investments and portfolios.

The current Two Sigma Factor Lens includes a broader holistic set of factors chosen

to identify risk and return drivers in both diversified portfolios and individual

investments. A thoughtfully chosen and constructed factor lens can assist with

answering questions such as what risks investors may be over- or underexposed to,

how their risk exposures differ from their benchmark, or what is driving their overall

and benchmark-relative returns.

Current Factor Lens

Today, our Factor Lens consists of the following 18 factors:

Even as we expanded the number of factors, the core principles we followed in constructing this lens remain unchanged. Just as when we first published our 2018

piece, we still believe today that the following four attributes should characterize

any factor lens that is ideally suited for portfolio and manager analysis:

- Holistic, by capturing the large majority of cross-sectional and time–series risks for typical institutional portfolios

- Parsimonious, by using as few factors as possible

- Orthogonal, with each risk factor capturing a statistically uncorrelated risk across assets

- Actionable, such that desired changes to factor exposure can be readily translated into asset allocation changes

We classify our current set of factors across four categories that we mentioned previously, starting from the more liquid and high capacity factors that often form the foundation of most institutional investors’ portfolios. The four categories are:

- Core Macro: The Core Macro factors are the most prevalent factors, and are

designed to consist of high-capacity, highly liquid factors that are considered

the principal drivers of asset class returns. - Secondary Macro: The Secondary Macro factors seek to identify key risks

that can cut across multiple asset classes in diversified portfolios, and are

considered to have lower capacity and liquidity than the Core Macro factors. - Equity Styles: Each Equity Style factor represents returns of a portfolio of

global stocks that is designed to be market-neutral and region-neutral, except

the Crowding factor, which is U.S.-focused. These factor portfolios also target

discrete, systematic characteristics shown by academic finance research¹ to

generate positive returns over time. - Macro Styles: Each of our Macro Style factors targets discrete, systematic

characteristics shown by academic research to generate positive returns over

time. Shortly after we added a few of these Macro Styles factors to our lens, we

published a piece in which we provided background on what these factors were

meant to capture, with a special focus on how Trend Following compares to one

of our Equity Styles factors, Momentum.

Although these newly added Style factors require more skill to capture and manage,

and are more costly to access than the Macro factors, they are still less expensive

and higher-capacity than “alpha”. Alpha can consist of idiosyncratic sources of return

(i.e., uncorrelated to other known factors) that are often limited in capacity and

have historically commanded higher fees. When using returns-based statistical

factor analysis, these idiosyncratic sources of return generally appear as “residual”

given their low correlation with known factors. However, not all residual return

represents true “alpha”. It can often just be uncompensated risk, and investors

should be careful when interpreting the residual from any statistical analysis of

historical performance.

A factor lens, such as the one we have been discussing here, can help determine

if an investment is indeed providing residual risk and return as opposed to simple

exposure to a combination of macro and style factors.

Finally, we believe that any outputs from the factor analysis we discuss here should

be translatable into asset allocation insights. For this reason, we constructed each of

these individual factors to be “investible,” meaning there should be a relatively stable

relationship between individual factors and a readily investible set of liquid assets.

To find more statistical and economic evidence for the factor lens we originally

constructed, including both quantitative and qualitative tests of our factor lens, please refer to our original paper from 2018, as well as our follow-up from 2019 that estimated long-term expected returns to each of the factors in our lens.

Conclusion

In the years that have followed our 2018 publication, “Introducing the Two Sigma Factor Lens”, we have continued to build upon our original framework of

systematically identifying, and then constructing, a practical set of risk factors.

Today, the Two Sigma Factor Lens contains 18 factors, with the latest addition

coming in 2020. Through our work on the Venn platform, we’ve also seen this

lens find broad applications among a multitude of client types. As we continue to

research and expand upon this lens, we maintain our founding principles: that risk

factors should be holistic, parsimonious, orthogonal, and actionable. Together, these

criteria continue to guide us through construction and expansion of a flexible risk

factor lens that we believe can be used broadly across the investment community.

We will address further applications of our factor lens in future publications, and

encourage those interested in seeing these applications in action to please contact

the Venn team through our website.

References

1 For more information on the academic research we cite, and the construction methodology of our factors, please reference the Two Sigma Factor Lens FAQ we have prepared here: https://help.venn.twosigma.com/en/articles/1392786-two-sigma-factor-lens-faq

This article is not an endorsement by Two Sigma Investor Solutions, LP or any of its affiliates (collectively, “Two Sigma”) of the topics discussed. The views expressed above reflect those of the authors and are not necessarily the views of Two Sigma. This article (i) is only for informational and educational purposes, (ii) is not intended to provide, and should not be relied upon, for investment, accounting, legal or tax advice, and (iii) is not a recommendation as to any portfolio, allocation, strategy or investment. This article is not an offer to sell or the solicitation of an offer to buy any securities or other instruments. This article is current as of the date of issuance (or any earlier date as referenced herein) and is subject to change without notice. The analytics or other services available on Venn change frequently and the content of this article should be expected to become outdated and less accurate over time. Any statements regarding planned or future development efforts for our existing or new products or services are not intended to be a promise or guarantee of future availability of products, services, or features. Such statements merely reflect our current plans. They are not intended to indicate when or how particular features will be offered or at what price. These planned or future development efforts may change without notice. Two Sigma has no obligation to update the article nor does Two Sigma make any express or implied warranties or representations as to its completeness or accuracy. This material uses some trademarks owned by entities other than Two Sigma purely for identification and comment as fair nominative use. That use does not imply any association with or endorsement of the other company by Two Sigma, or vice versa. See the end of the document for other important disclaimers and disclosures. Click here for other important disclaimers and disclosures.

This article may include discussion of investing in virtual currencies. You should be aware that virtual currencies can have unique characteristics from other securities, securities transactions and financial transactions. Virtual currencies prices may be volatile, they may be difficult to price and their liquidity may be dispersed. Virtual currencies may be subject to certain cybersecurity and technology risks. Various intermediaries in the virtual currency markets may be unregulated, and the general regulatory landscape for virtual currencies is uncertain. The identity of virtual currency market participants may be opaque, which may increase the risk of market manipulation and fraud. Fees involved in trading virtual currencies may vary.