You’ve just left an investment conference where a keynote speaker brilliantly outlined what could be the future of portfolio management. The "total portfolio approach" (TPA) sounded revolutionary—focusing on a factor lens to analyze holistic risk and outcomes, rather than rigid asset class buckets. The logic was sound and the slides were compelling.

But as the conference glow fades and you're back at your desk, reality sets in. Your spreadsheets are still organized by equities, bonds, real estate, and hedge funds. Your colleagues are still divided into asset class silos. A sophisticated factor lens was not included with the conference swag.

How do you actually go about implementing a total portfolio approach?

The TPA Implementation Gap

A factor lens is the foundation of a TPA and the core of Venn’s design – the essential engine that powers the entire system. It is the common language used to analyze risk across and within all asset classes. Despite this critical importance, it is difficult for most institutional allocators to design and build themselves. Even more challenging is procuring, cleaning, and updating the necessary data. Without a robust factor lens, a TPA remains an academic theory rather than a practical reality.

This gap between theory and practice was the direct inspiration for the inception of the Two Sigma Factor Lens, which evolved into the comprehensive Venn platform we offer today. Let’s explore three major barriers that prevent most investors from utilizing a total portfolio approach, and how Venn was designed to be a potential solution.

- The Factor Lens Barrier: Building and Maintaining a Statistically Sound Lens

- The Data Barrier: Analyzing Multi-Asset Portfolios Without Holdings Data

- The Workflow Barrier: Implementing TPA Analysis Within Existing Workflows

The Factor Lens Barrier: Building and Maintaining a Statistically Sound Lens

In a perfect world, each investor would develop a tailor-made factor lens unique to their portfolio, with no two approaches being the same. But the universe of potential risk factors is essentially infinite and filled with statistical complexities, making it difficult to know where to start. Even for the most sophisticated institutions, building and maintaining a factor lens is rarely realistic given the time, cost, and expertise required.

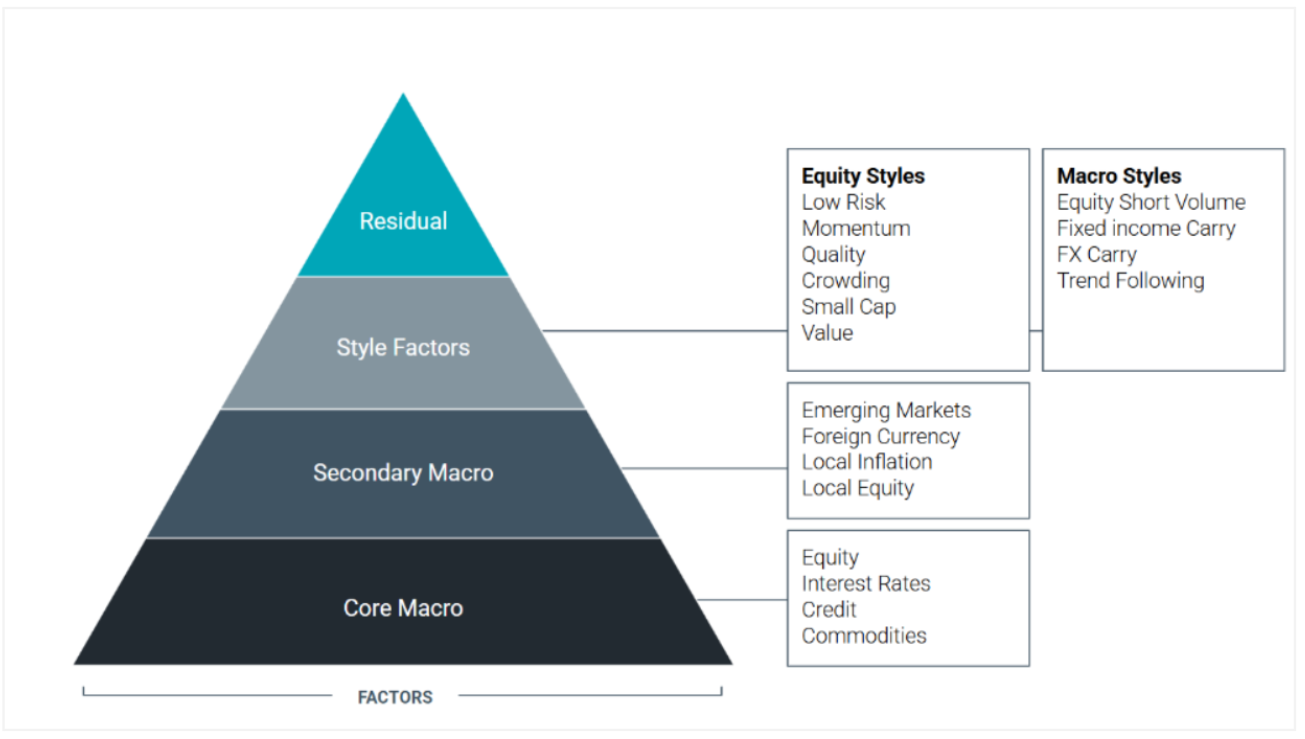

While some factor lenses include hundreds of factors and are intended for granular and tactical decision making, our research suggests that investors don't need an overwhelming number of factors to manage their portfolios. Just as a nutritional label distills countless food compounds into essential components to manage human health, we believe a practical factor lens should focus on the fundamental risks applicable to all portfolios.

Like a well-designed nutrition label, the Two Sigma Factor Lens aims to capture the essential information needed to understand portfolio outcomes in an intuitive way. Using just 18 factors, our lens has appeared to explain between 90% and 98% of return variation associated with typical institutional profiles.

This "less-is-more" approach achieves high explanatory power while helping investors see what matters. We believe that it is a universally applicable global perspective that any investor can use.

Exhibit 1: The Two Sigma Factor Lens is a Less-Is-More Approach

Source: Venn by Two Sigma. For illustration purposes only.

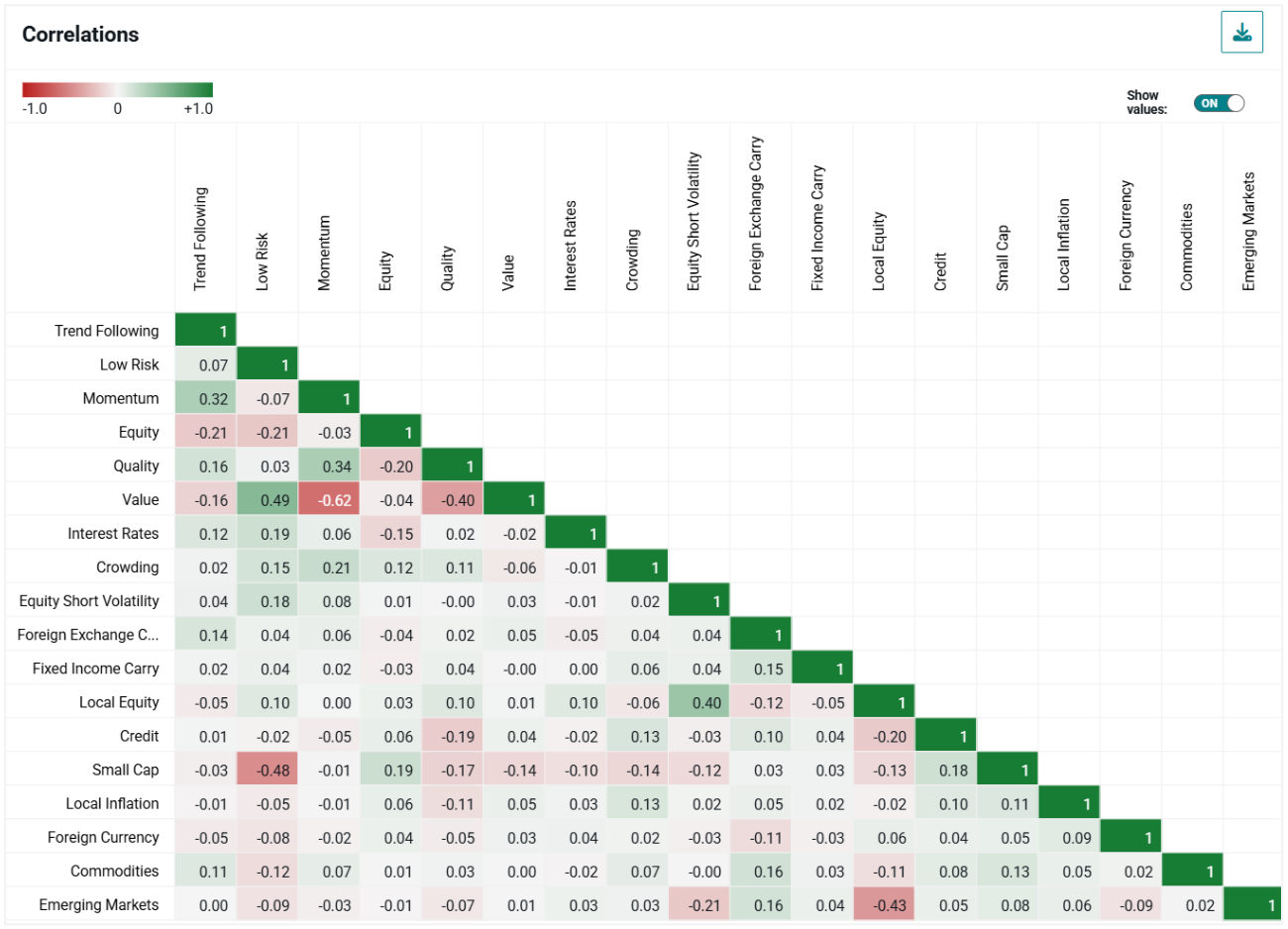

Equally challenging as factor selection is making sure that chosen risks work together efficiently. It is critical to seek broad independence between factors – otherwise, risk attribution becomes inaccurate, which can lead to imprecise allocation decisions.

The Two Sigma Factor Lens seeks to address this by ensuring factors maintain broad independence with each other (especially among macro factors) and implementing a tier system that consolidates overlapping risks into higher-tier factors. This provides allocators with a ready-to-use framework designed to produce intuitive, holistic, and academically rigorous insights. Whereas traditional asset class diversification often contains hidden correlations, a portfolio with exposure across various factors in the Two Sigma Factor Lens means diversification across truly independent sources of risk and return.

Exhibit 2: Uncorrelated Factors Lead to More Precise Allocation Decisions

Source: Venn by Two Sigma. Period from 8/7/1998 – 5/16/2025.

In our view, the off-the-shelf and ready to use nature of the Two Sigma Factor Lens effectively breaks down the factor lens barrier.

The Data Barrier: Analyzing Multi-Asset Portfolios Without Holdings Data

To conduct analysis that requires looking through to underlying positions, investment teams are reliant on fund managers sharing holdings in a transparent and timely manner.

For public equity and bond funds, allocators can conduct sophisticated analysis with few obstacles. But for hedge funds, SMAs, private assets, etc., allocators are often forced to rely on whatever limited analysis managers provide. This obstacle applies to holdings-based factor analysis as well, which is used by many providers. Without timely and transparent portfolio holdings data, holdings-based analysis can be a fragmented and inconsistent view of portfolio risk – the opposite of what a true TPA promises.

The Two Sigma Factor Lens was purpose-built to overcome this barrier through a returns-based approach. Rather than requiring hard-to-access holdings data, our regression-based methodology works with what allocators actually have – investment returns. Given that Venn supplies the factor return time series, this makes holistic factor analysis immediately accessible to subscribers once investment returns are uploaded or they access Venn-provided investments from our data library.

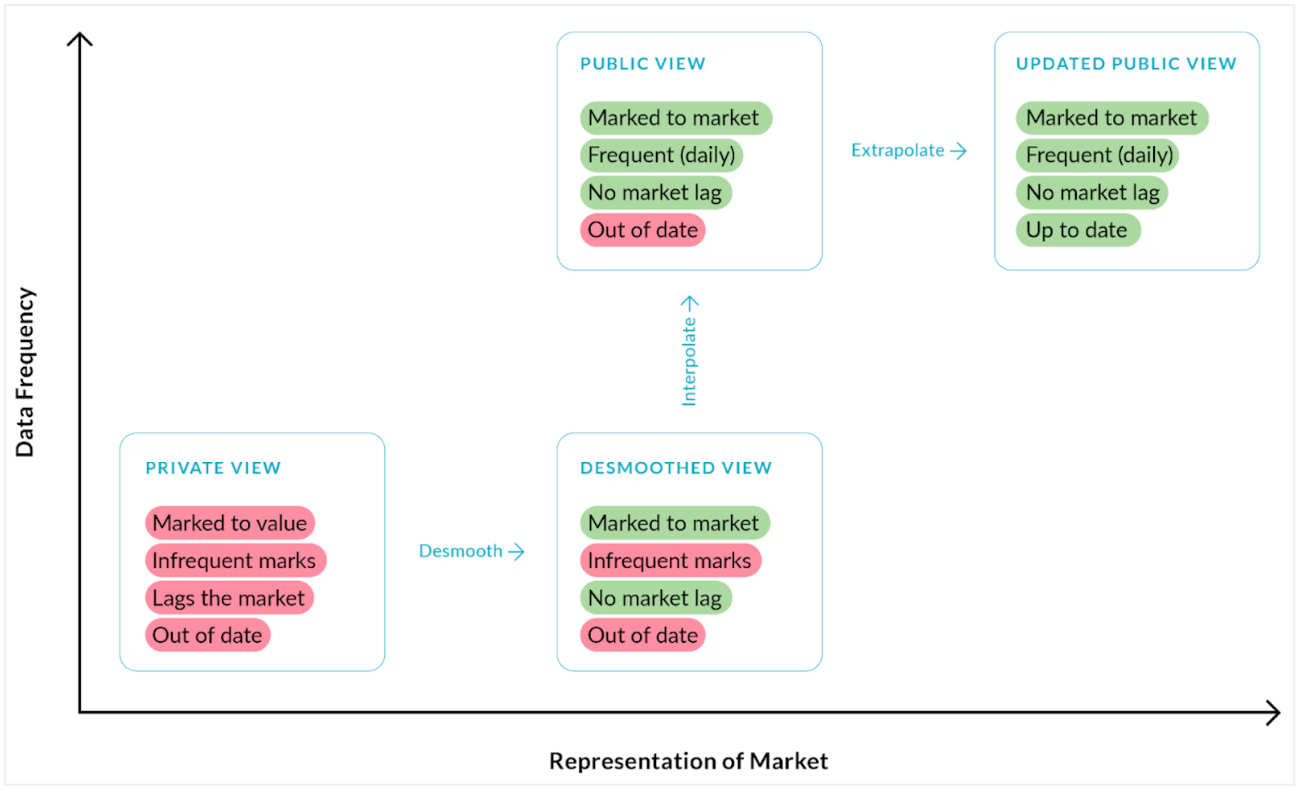

In cases where returns data is imperfect, techniques for enhancing it are readily available. For example, Venn can implement proxy methods such as backfilling or interpolation to extend limited history or convert quarterly returns to daily. Extrapolation can be used to estimate the current value of an asset even if it is multiple quarters out of date, preventing one outdated position from limiting total portfolio analysis.

For private assets, time-weighted returns often exhibit artificially low volatility and lag behind public markets. Return desmoothing can adjust for these biases. By combining desmoothing with other proxying techniques, you can even bring private investments into the same analytical framework as liquid public assets, allowing them to be analyzed on equal footing – a critical requirement for any true total portfolio approach.

Exhibit 3: A Total Portfolio Approach Should Include Private Asset Solutions

Source: Venn by Two Sigma. For illustration purposes only.

In our view, a returns-based approach addresses the practical data reality for allocators, effectively breaking down the data barrier.

The Workflow Barrier: Implementing TPA Analysis Within Existing Workflows

Factor analysis can be easily trapped in static spreadsheets or complex systems that only quants can navigate. This creates bottlenecks where insights remain isolated rather than driving portfolio decisions across teams.

What’s more, when it comes to truly embracing a total portfolio approach, even the best analysis remains theoretical without practical implementation tools. A factor lens alone isn't enough—it needs to be embedded in workflows that enable teams to collaborate, explore insights, and communicate findings effectively.

Venn was designed specifically to overcome these workflow barriers through three key capabilities:

Seamless Collaboration Through Cloud Architecture: The cloud-based infrastructure of Venn transforms how investment teams work together on total portfolio analysis. When one team member creates a custom analysis or report, that intelligence is immediately available to everyone in the workspace. This shared knowledge environment eliminates duplicated efforts and ensures consistent analysis across the organization.

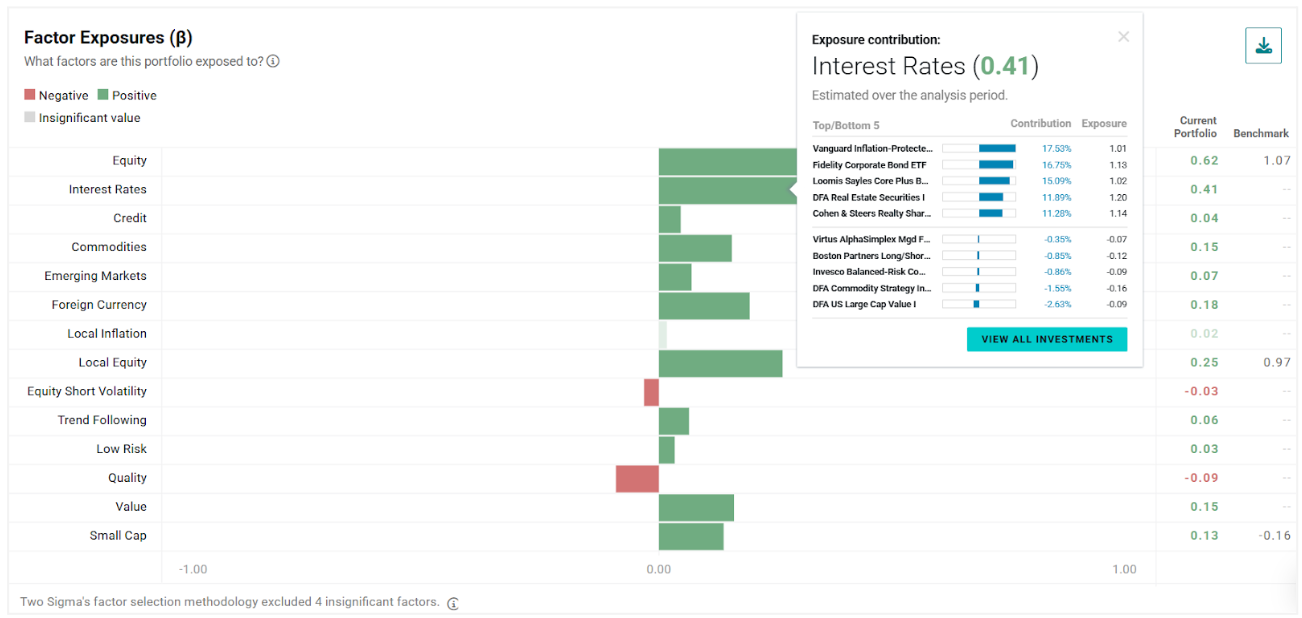

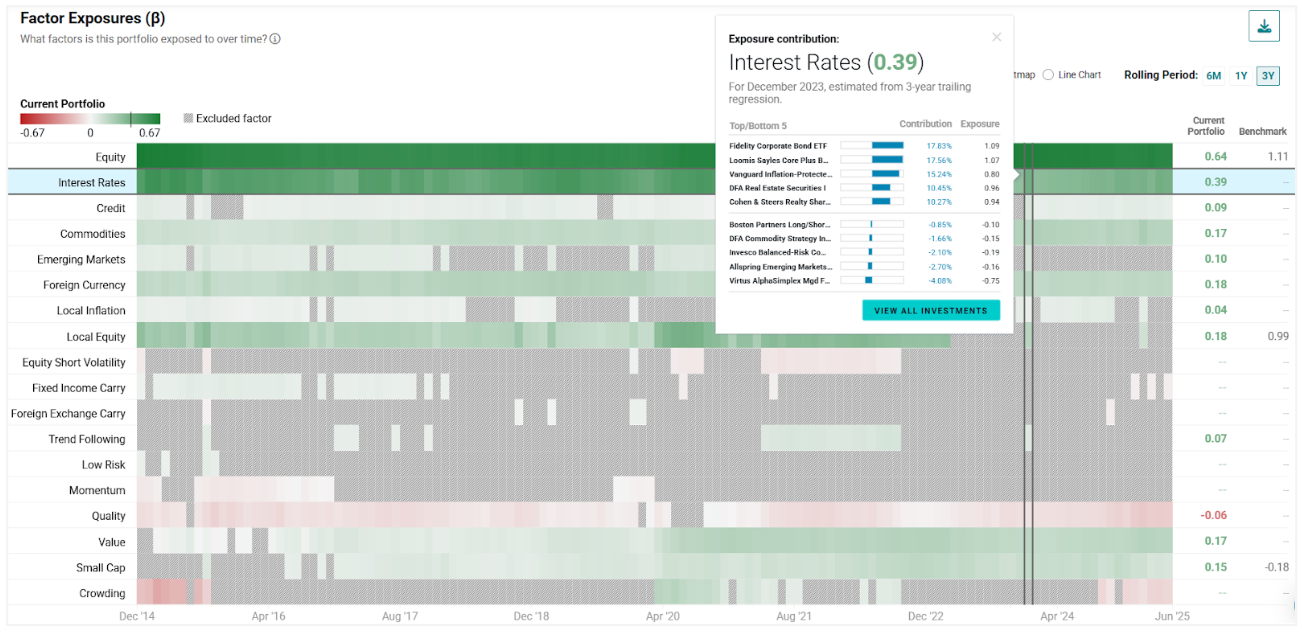

Interactive Visualization That Makes Factors Actionable: Understanding factor exposures is one thing—knowing what to do about them is another. Venn's interactive interface allows users to instantly drill down from portfolio-level insights to individual contributors. For example, clicking on a potentially concerning Interest Rates factor exposure immediately reveals which managers or investments are driving that exposure, facilitating targeted decision-making rather than guesswork.

Exhibit 4: An Interactive UX Leads to Actionable Portfolio Insights

Source: Venn by Two Sigma. For illustration purposes only.

This interactivity extends throughout the Venn platform—from rolling period analysis that reveals how active manager factor exposures change over time (Exhibit 5), to performance stress testing. Venn’s clean and modern interface transforms complex quantitative concepts into intuitive visuals that can help drive decision-making.

Exhibit 5: Visualizing Portfolio Evolution Through Factor Trend Analysis

Source: Venn by Two Sigma. For illustration purposes only.

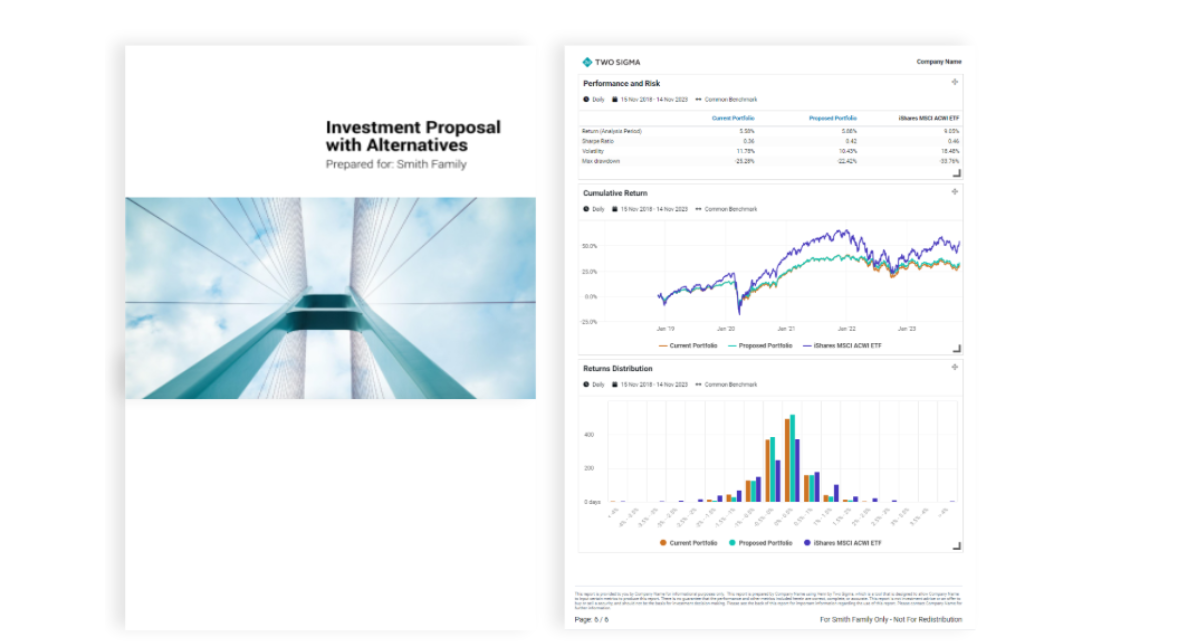

Comprehensive Reporting Beyond Just Factors: Effectively communicating a total portfolio approach is essential. Venn’s Report Lab furthers this goal by transforming analyses into polished, professional communications that bridge the gap between technical details and stakeholder understanding.

The drag-and-drop nature of Report Lab allows teams to create custom reports that combine factor insights with traditional performance metrics, including the ability to incorporate management fees, custom disclosures, and your firm’s branding. In fact, templates go beyond deep dives into a portfolio’s factor profile. They can be geared toward manager due diligence, performance reporting, comparing current and proposed portfolios, etc.

This unified approach eliminates the typical workflow where analysis happens in one system but must be manually transferred to presentation tools—a process that introduces delays and potential errors.

Exhibit 6: A Seamless Transition from Analysis to Storytelling

Source: Venn by Two Sigma. For illustration purposes only.

Venn’s design acknowledges that implementation is about more than just analytical capabilities – it's about making those capabilities accessible and actionable across investment teams. We believe Venn’s holistic and collaborative platform design effectively breaks down that typical workflow barrier.

Getting Started with a Total Portfolio Approach

Investment teams face three significant challenges to implementing a total portfolio approach: developing a robust factor lens, overcoming data limitations, and integrating factor analysis into everyday workflows. Rather than tackling each barrier in isolation, Venn offers a comprehensive solution that addresses these challenges simultaneously.

By combining an academically rigorous yet digestible factor lens with a returns-based implementation, Venn creates a seamless experience that can transform how investment teams operate. This allows allocators to move beyond theoretical discussions and into practical implementation, all within a platform designed to seamlessly integrate traditional and total portfolio workflows.

The journey to implementation is more straightforward than many believe. With the right tools, allocators can begin seeing their portfolios through a factor lens in minutes – not months – gaining insights that complement traditional asset class frameworks while revealing risks and opportunities that might otherwise remain hidden.

We encourage those who see the value in total portfolio thinking to explore how accessible implementation has become. Whether you're looking to completely transform your allocation process or simply add a complementary analytical lens, the tools now exist to turn conference inspiration into portfolio reality.

References to the Two Sigma Factor Lens and other Venn methodologies are qualified in their entirety by the applicable documentation on Venn.

This article is not an endorsement by Two Sigma Investor Solutions, LP or any of its affiliates (collectively, “Two Sigma”) of the topics discussed. The views expressed above reflect those of the authors and are not necessarily the views of Two Sigma. This article (i) is only for informational and educational purposes, (ii) is not intended to provide, and should not be relied upon, for investment, accounting, legal or tax advice, and (iii) is not a recommendation as to any portfolio, allocation, strategy or investment. This article is not an offer to sell or the solicitation of an offer to buy any securities or other instruments. This article is current as of the date of issuance (or any earlier date as referenced herein) and is subject to change without notice. The analytics or other services available on Venn change frequently and the content of this article should be expected to become outdated and less accurate over time. Any statements regarding planned or future development efforts for our existing or new products or services are not intended to be a promise or guarantee of future availability of products, services, or features. Such statements merely reflect our current plans. They are not intended to indicate when or how particular features will be offered or at what price. These planned or future development efforts may change without notice. Two Sigma has no obligation to update the article nor does Two Sigma make any express or implied warranties or representations as to its completeness or accuracy. This material uses some trademarks owned by entities other than Two Sigma purely for identification and comment as fair nominative use. That use does not imply any association with or endorsement of the other company by Two Sigma, or vice versa. See the end of the document for other important disclaimers and disclosures. Click here for other important disclaimers and disclosures.

This article may include discussion of investing in virtual currencies. You should be aware that virtual currencies can have unique characteristics from other securities, securities transactions and financial transactions. Virtual currencies prices may be volatile, they may be difficult to price and their liquidity may be dispersed. Virtual currencies may be subject to certain cybersecurity and technology risks. Various intermediaries in the virtual currency markets may be unregulated, and the general regulatory landscape for virtual currencies is uncertain. The identity of virtual currency market participants may be opaque, which may increase the risk of market manipulation and fraud. Fees involved in trading virtual currencies may vary