The weakening USD has made headlines thus far in 2025. Since mid-January, it's fallen

just shy of 11% against a basket of major currencies.1 Since 1971, declines of this

magnitude or greater over a similar timeframe have occurred only 2.5% of the

time.2 This has likely benefited U.S. investors with unhedged international exposure, as

their assets are held in non-USD currencies.

But here's what's surprising: our research shows that some assets’ volatility have

become less driven by our Foreign Currency factor, not more. By separating pure

currency movements from interest rate-driven effects, the Two Sigma Factor Lens

reveals how these factors can shift their roles as primary drivers of risk.

This piece highlights a practical example of how Foreign Currency and Interest Rates

factors can interact, while demonstrating a broader truth: fundamental drivers of risk

change with market conditions, even when asset class labels stay the same. We hope

to highlight how looking beyond headlines to monitor shifting factor relationships is

critical for effective portfolio management.

Setting the Stage: Why International Bonds Tell the Story

Let's begin by examining our Foreign Currency factor through unhedged international

government bonds and equities.3

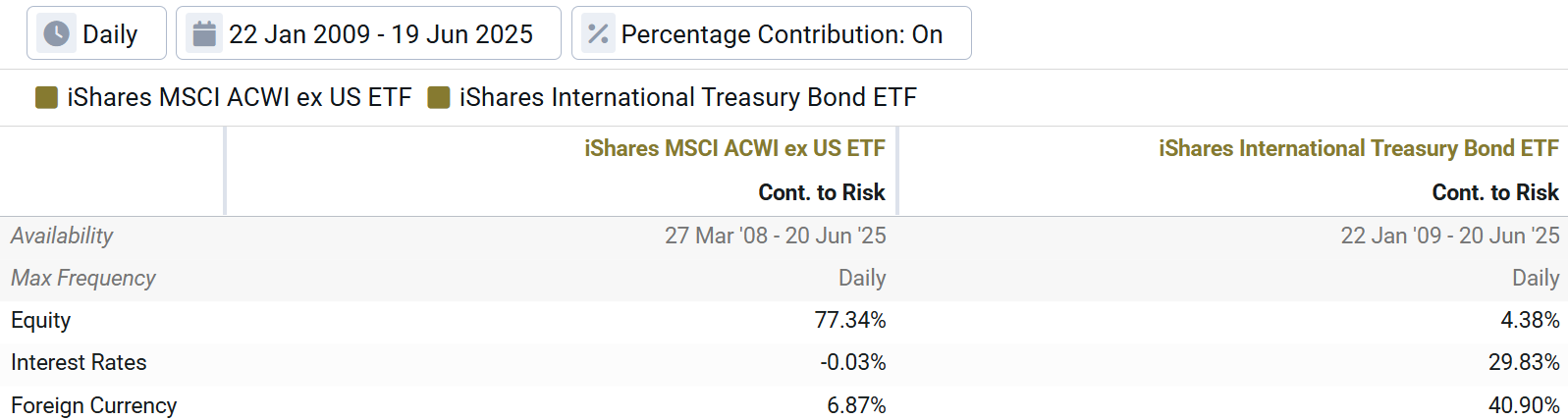

Using Venn's Two Sigma Factor Lens in Exhibit 1, we find that our Foreign Currency

factor explains 6.87% of international equity volatility, but a dominant 40.90% for

international bonds. While this is just an analytical appetizer, the idea that a bond fund's

risk can be mostly driven by our Foreign Currency factor may be surprising to some

investors.

Exhibit 1: Venn’s Foreign Currency Factor Explains the Majority of Unhedged

International Bond Risk

Source: Venn by Two Sigma. The table includes Equity and Interest Rates (Tier 1 Macro Factors) and our Foreign Currency factor

only; percentages do not sum to 100% due to excluded factors.

Why does our Foreign Currency factor explain more risk for unhedged bonds than

equities? This is mainly due to the relatively lower volatility of bonds, which allows

currency risk to have greater relative impact.

This international bond fund is the perfect case study for what happens next. While our

Foreign Currency factor has historically dominated its risk profile, our Interest Rates

factor has always played a meaningful secondary role, but is this still true today?

The Big Shift: Interest Rates Become The Primary Driver of Risk

Here's where it gets interesting. Our trend analysis in Exhibit 2 tells a completely

different story than the static numbers in Exhibit 1.

Looking at our rolling 3-year factor analysis, the Foreign Currency factor peaked when

explaining roughly 70% of international bond risk around 2017–2019. It then reversed,

dropping to roughly 20% today. At the same time, our Interest Rates factor surged from

15% to nearly 50%.

Exhibit 2: Rolling 3-Year Factor Contribution to Risk for the iShares International

Treasury Bond ETF (IGOV)

%20.png)

Source: Venn by Two Sigma from 1/22/2009–6/19/2025. This chart only includes Interest Rates and Foreign Currency factors and

will not add up to 100%.

Put simply: In our example, while USD weakness makes headlines, the explanatory

power of our Foreign Currency factor actually declined meaningfully, while our Interest

Rates factor has been explaining more risk.

This demonstrates how fundamental drivers of risk can evolve as markets digest new

regimes around trade, inflation, and geopolitical developments. Whether investors have

direct international bond exposure, or diversified multi-asset portfolios, it may be time to

reassess their drivers of risk.

The Early Warning: Factor Models May See What Headlines Miss

Digging deeper into Exhibit 2, the changing trends between our Foreign Currency and

Interest Rates factors began as early as 2017–years before the latest inflation surges,

rate hiking cycles, or USD volatility.

This shows how factor models can capture subtle changes in correlations and relative

volatilities that may reveal fundamental shifts earlier than traditional analysis or

headlines. This early detection matters because by the time a risk regime changes,

portfolios may have already experienced significant unintended exposures.

Identifying these trends as early as 2017 demonstrates how factor decomposition can

find structural changes in market dynamics that otherwise might remain hidden.

The Bottom Line: Why This Matters for Your Portfolio

This isn't just a technical curiosity, this analysis has real portfolio implications.

USD weakness only tells part of the risk story. While currency moves capture attention,

our analysis reveals that our Interest Rates factor has quietly become the more

prominent driver of international bond risk, a shift that began taking place years before

recent market volatility.

This example illustrates a fundamental truth about modern markets: risk factor

relationships are not static.

What drove portfolio volatility in 2015 may not drive it today, even within the same asset

class.

For institutional investors, this suggests that ongoing factor analysis may be essential

for staying ahead of evolving market dynamics and identifying shifting trends earlier.

Whether managing international bonds or diversified multi-asset portfolios, investors

should reassess how their fundamental risk exposures have evolved, especially in

current markets.

References

1Source: Bloomberg using the DXY Index. Period from 1/13/2025–6/25/2025.

2Source: Bloomberg. Using the DXY Index, 2.5% refers to the percentage of 118 trading-day rolling periods since 1971 that posted declines equal to or greater than the 1/13/2025–6/25/2025 period.

3International government bonds represented by the iShares International Treasury Bond ETF (IGOV) and international equities represented by the iShares MSCI ACWI ex US ETF (ACWX).

Exposure to risk factors is not a guarantee of increased performance or decreased risk. References to the Two Sigma Factor Lens and other Venn methodologies are qualified in their entirety by the applicable documentation on Venn.

This article is not an endorsement by Two Sigma Investor Solutions, LP or any of its affiliates (collectively, “Two Sigma”) of the topics discussed. The views expressed above reflect those of the authors and are not necessarily the views of Two Sigma. This article (i) is only for informational and educational purposes, (ii) is not intended to provide, and should not be relied upon, for investment, accounting, legal or tax advice, and (iii) is not a recommendation as to any portfolio, allocation, strategy or investment. This article is not an offer to sell or the solicitation of an offer to buy any securities or other instruments. This article is current as of the date of issuance (or any earlier date as referenced herein) and is subject to change without notice. The analytics or other services available on Venn change frequently and the content of this article should be expected to become outdated and less accurate over time. Two Sigma has no obligation to update the article nor does Two Sigma make any express or implied warranties or representations as to its completeness or accuracy. This material uses some trademarks owned by entities other than Two Sigma purely for identification and comment as fair nominative use. That use does not imply any association with or endorsement of the other company by Two Sigma, or vice versa. See the end of the document for other important disclaimers and disclosures. Click here for other important disclaimers and disclosures.