We recently discussed how unhedged global equities are exposed to movements in Foreign Currency, and a variety of other risks as well, such as Interest Rates.

In this follow-up piece, we apply similar factor analysis to the Vanguard Total World Bond ETF (BNDW), with a continued focus on currency-related insights from a U.S. perspective. Interestingly, this manager represents a unique ETF of ETFs structure. This makes returns-based factor analysis particularly useful as a way to see through individual fund holdings, identifying the manager’s overall approach to foreign currencies.

What’s Going On Under the Hood of This Global Bond Manager?

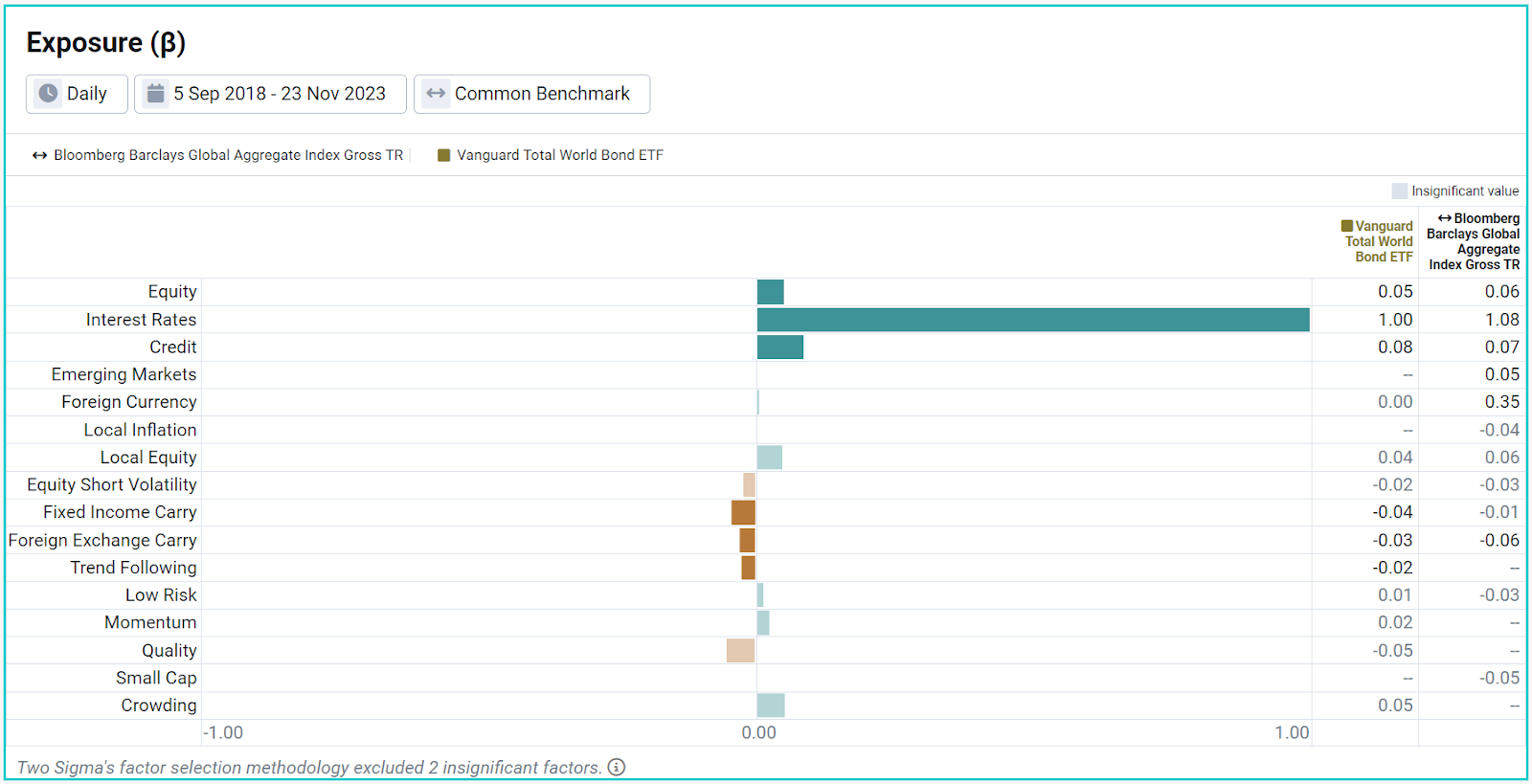

An intuitive place to start with a global bond fund is to compare its factor exposures side by side with a benchmark, such as the Bloomberg Barclays Global Aggregate Index.

As we can see in Exhibit 1, exposures are quite similar across the board. For example, the primary exposure for both the manager and benchmark is Venn’s Interest Rates factor at 1.00 and 1.08, respectively. This suggests that both may benefit when global rates fall.

One noticeable difference is that Foreign Currency was not selected as a relevant factor for the bond manager via Venn’s factor selection process. On the other hand, the global benchmark populated a meaningful exposure of 0.35.

Exhibit 1: Factor Exposure (ß)

Source: Venn by Two Sigma. Start date based on BNDW inception.

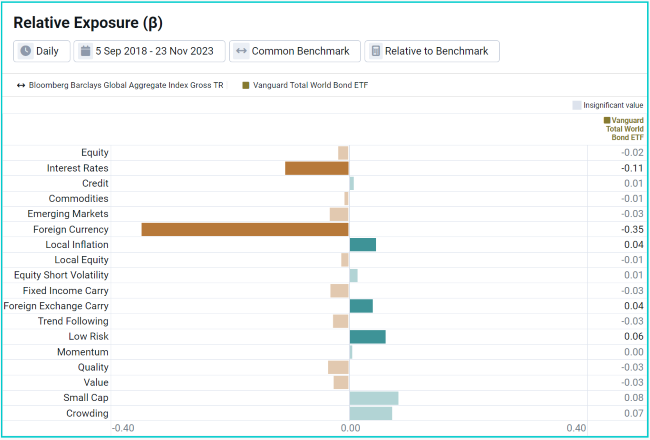

In Exhibit 2, relative analysis more distinctly highlights Foreign Currency as the prominent differentiator.1 Good questions to ask may be: “What could be causing this discrepancy, and how differentiating has it been in terms of risk and return?”

Exhibit 2: Relative Exposure (ß)

Source: Venn by Two Sigma. Start date based on BNDW inception.

Diving Deeper into Factor Analysis Results

At least in its name, there is no clear indication that this manager is employing a currency hedging strategy or some other method of neutralizing currency risk.

Upon further qualitative investigation, we found that of the ETFs that this fund of funds holds, one is currency hedged while the other holds only U.S. dollar-denominated bonds. This demonstrates the power of factor analysis, revealing this global bond manager’s lack of Foreign Currency exposure without needing more information about the top-level fund or its underlying ETFs. It also suggests that our unhedged benchmark may not be an appropriate benchmark.

But how much has Foreign Currency really mattered between the two?

Quantifying Differences with Factor Analysis

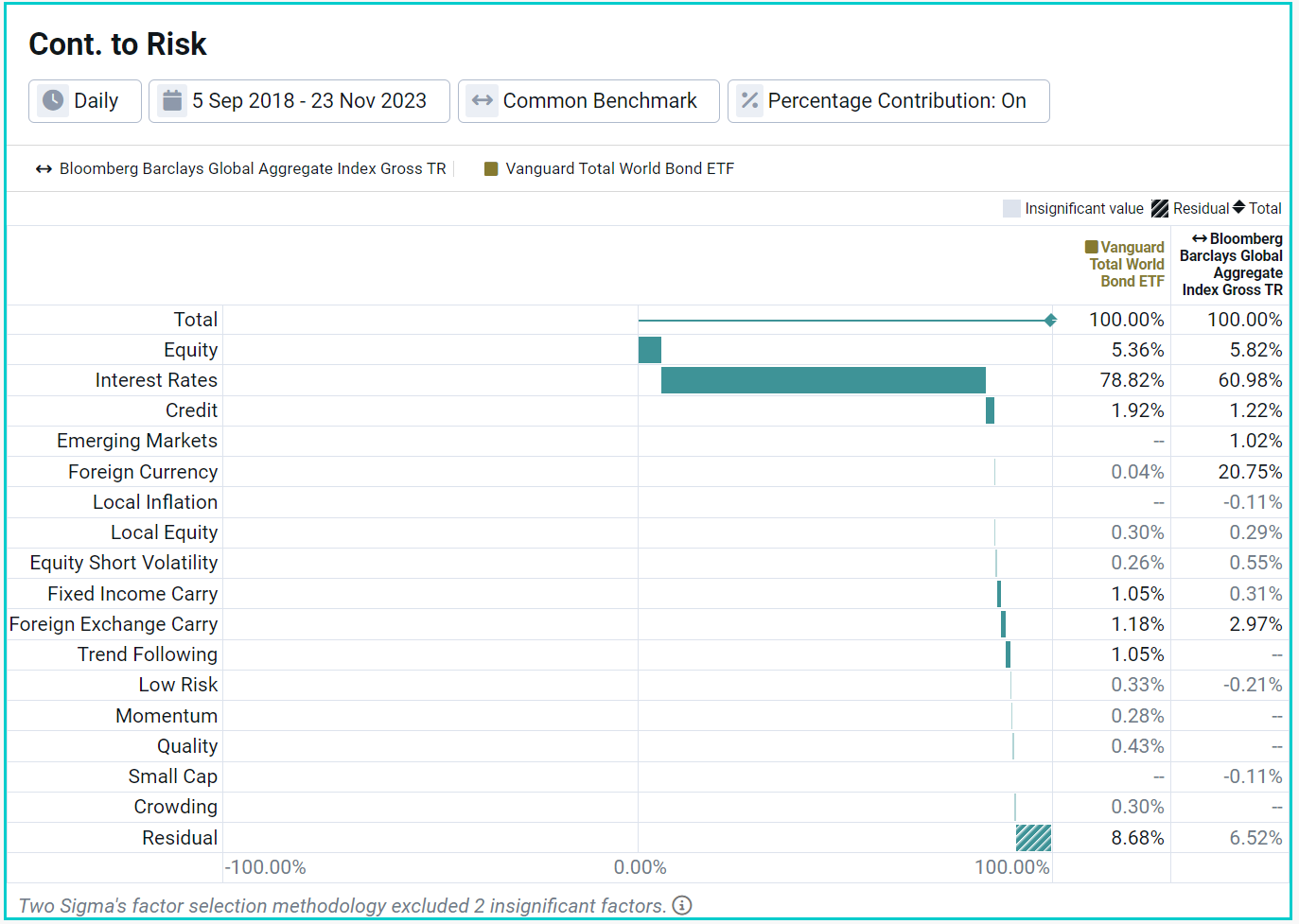

In Exhibit 3, we show how each of our factors has contributed to the total risk of each asset out of 100%. To set the stage, over the period we analyzed, the bond manager exhibited a standard deviation of 5.2%, while the global benchmark came in at 5.5%.

For example, despite Interest Rates exposure being quite similar for both of these managers (as shown in Exhibit 1), this factor drove roughly 80% of the bond manager’s risk, but only 60% of the global benchmark. This is partly because 20.75% of the risk for the global benchmark was driven by our Foreign Currency factor. That’s right, almost a quarter of the risk for the global bond benchmark was not driven by Interest Rates, but rather movements in global exchange rates.

Exhibit 3: Factor Contribution to Risk

Source: Venn by Two Sigma. Start date based on BNDW inception.

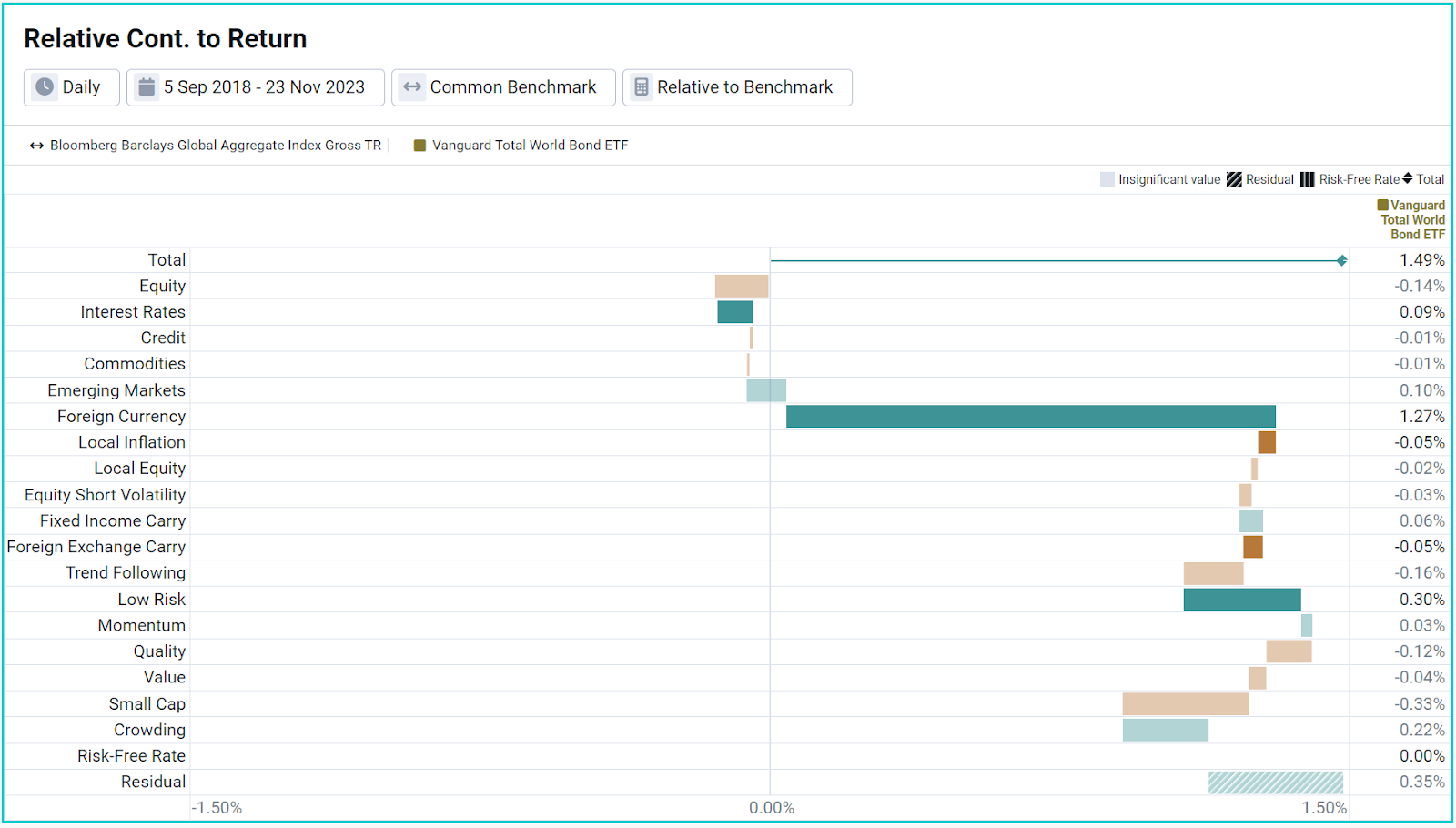

Switching back to a relative view, we found that Foreign Currency was a significant differentiator in terms of performance. More specifically, roughly 1.27% of average annualized excess return came from the bond manager simply not having Foreign Currency exposure compared to meaningful exposure for the benchmark. This makes sense as the U.S. dollar rose by 10.63% over the period analyzed,2 creating headwinds for unhedged exposures that invest by way of local currencies.

Exhibit 4: Factor Contribution to Excess Return

Source: Venn by Two Sigma. Start date based on BNDW inception.

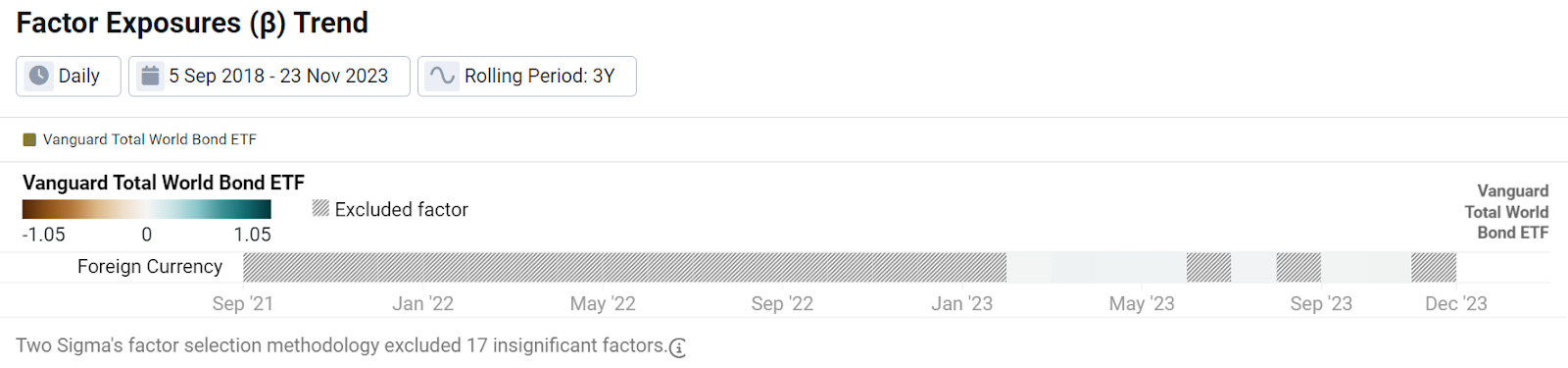

As a final check, let’s see how consistent a lack of Foreign Currency exposure has been for our selected manager. In Exhibit 5, we see that over rolling 3-year periods, our factor selection process excludes Foreign Currency for this manager a vast majority of the time. When the Foreign Currency factor is included, exposure is close to zero, signaling that indeed this fund of funds seems to consistently neutralize Foreign Currency.

Exhibit 5: Trend in Foreign Currency Exposure

Source: Venn by Two Sigma. Start date based on BNDW inception.

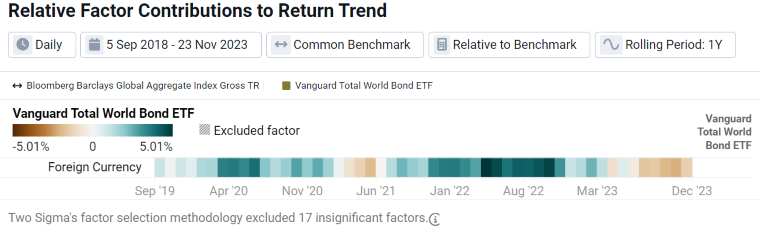

Exhibit 4 showed that less Foreign Currency exposure has led to outperformance over the full period. However, this shouldn't be the case over every point in time, as U.S. dollar performance relative to other currencies has undoubtedly ebbed and flowed. In Exhibit 5, we look at trends in excess returns to identify when Foreign Currency exposure was and wasn’t beneficial.

For example, over the 1-year period ending 8/31/2023, the USD was down -4.67% as foreign currencies relatively appreciated. As a result, Foreign Currency exposure led to a -1.54% drag on relative return for this manager vs the global benchmark.

Exhibit 6: Trends in Factor Contribution to Excess Return

Source: Venn by Two Sigma. Start date based on BNDW inception.

Factor Analysis: Truth Will Out

We show that when investing internationally, exposure to Foreign Currency can significantly affect resulting drivers of risk and return, and how returns-based factor analysis can be an efficient way to measure that exposure.

Understanding the effects of Foreign Currency on a portfolio, manager, or even benchmark can drive the difference between one asset allocation decision and another. Depending on the context, Foreign Currency can be a headwind or tailwind to returns, it can gobble up a portion of explained risk, or even work for or against the realized alpha of a manager or portfolio. Factor analysis can bring this information to the surface, which we believe may ultimately lead to more actionable asset allocation decisions.

References

1 An interesting side note: the global bond benchmark also has slightly higher Interest Rates exposure. One possible explanation for this has to do with its unhedged nature. In the predecessor piece to this, we discussed how Foreign Currency risk may be entangled with other factors, and how Venn will “pull” that exposure out and attempt to quantify it appropriately. In this case, various characteristics may affect the differences in Interest Rates exposure, but it may be that additional Interest Rates exposure for the benchmark represents what was pulled out of Foreign Currency through Venn’s residualization process.

2 This and other references throughout this piece to U.S dollar performance are referring to the U.S Dollar Index (DXY). This measures the performance of the U.S dollar relative to six major currencies.

This article is not an endorsement by Two Sigma Investor Solutions, LP or any of its affiliates (collectively, “Two Sigma”) of the topics discussed. The views expressed above reflect those of the authors and are not necessarily the views of Two Sigma. This article (i) is only for informational and educational purposes, (ii) is not intended to provide, and should not be relied upon, for investment, accounting, legal or tax advice, and (iii) is not a recommendation as to any portfolio, allocation, strategy or investment. This article is not an offer to sell or the solicitation of an offer to buy any securities or other instruments. This article is current as of the date of issuance (or any earlier date as referenced herein) and is subject to change without notice. The analytics or other services available on Venn change frequently and the content of this article should be expected to become outdated and less accurate over time. Any statements regarding planned or future development efforts for our existing or new products or services are not intended to be a promise or guarantee of future availability of products, services, or features. Such statements merely reflect our current plans. They are not intended to indicate when or how particular features will be offered or at what price. These planned or future development efforts may change without notice. Two Sigma has no obligation to update the article nor does Two Sigma make any express or implied warranties or representations as to its completeness or accuracy. This material uses some trademarks owned by entities other than Two Sigma purely for identification and comment as fair nominative use. That use does not imply any association with or endorsement of the other company by Two Sigma, or vice versa. See the end of the document for other important disclaimers and disclosures. Click here for other important disclaimers and disclosures.

This article may include discussion of investing in virtual currencies. You should be aware that virtual currencies can have unique characteristics from other securities, securities transactions and financial transactions. Virtual currencies prices may be volatile, they may be difficult to price and their liquidity may be dispersed. Virtual currencies may be subject to certain cybersecurity and technology risks. Various intermediaries in the virtual currency markets may be unregulated, and the general regulatory landscape for virtual currencies is uncertain. The identity of virtual currency market participants may be opaque, which may increase the risk of market manipulation and fraud. Fees involved in trading virtual currencies may vary.