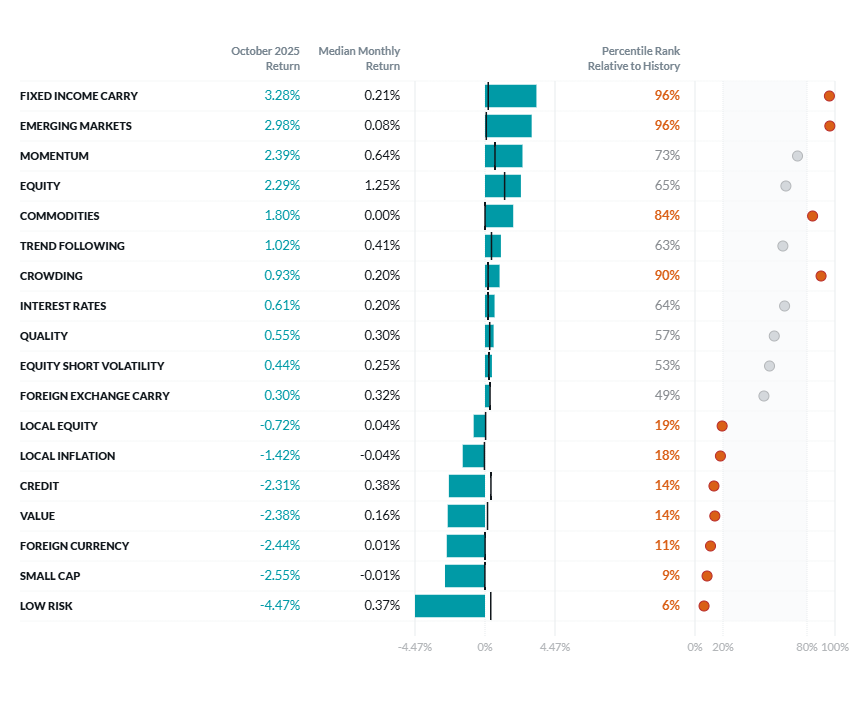

Exhibit 1: October Performance of the Two Sigma Factor Lens

©2025 Two Sigma Investments, LP. This image is for informational purposes only. See https://www.venn.twosigma.com/blog-disclaimer for more disclaimers and disclosures.

Source: Venn by Two Sigma. The median and percentile columns measure the performance of each factor in the Two Sigma Factor Lens relative to the entire history of the factor in USD, using monthly data for the period August 1998 - August 2025

With multiple factors posting outsized moves, we summarize highlights by category. For details on our factor categories, decorrelation process, and risk consolidation framework, see our past blog.

Tier 1 Core Macro Factors

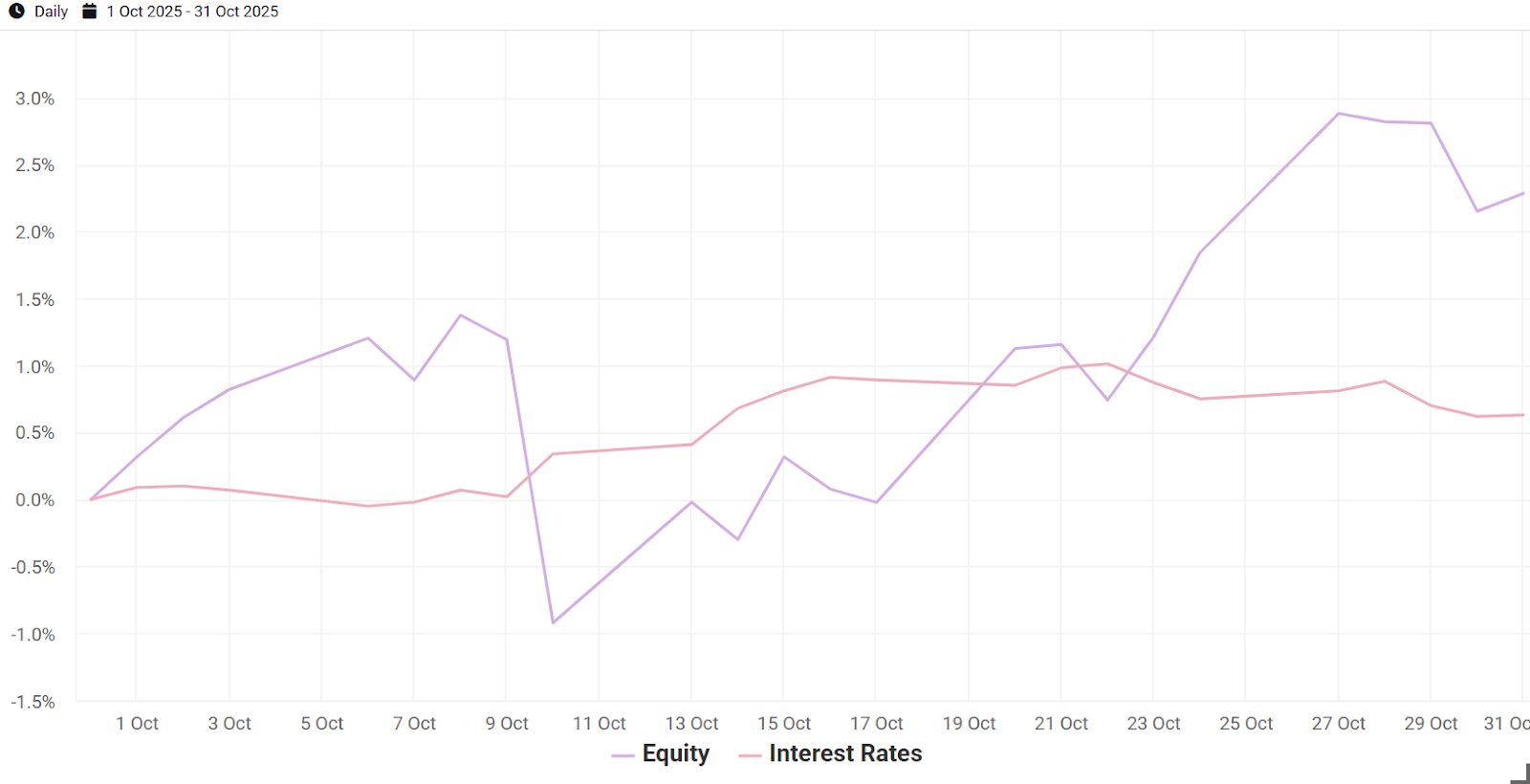

Equity and Interest Rates: While neither of these factors posted outsized monthly returns, both were volatile intra‑month and affected other factors through residualization. The Equity factor experienced a sharp two‑day drawdown around China’s rare‑earth export announcement. The Interest Rates factor rallied on the same news. However, after normalizing by long‑term volatility, we found that the Equity drawdown was roughly twice the magnitude of the Interest Rates rally. U.S. trade language quickly softened, helping to de-escalate tensions and support an Equity factor recovery.1

Exhibit 2: October Performance of Venn’s Equity and Interest Rates Factors

Source: Venn by Two Sigma.

Source: Venn by Two Sigma.

Tier 2 Core Macro Factors

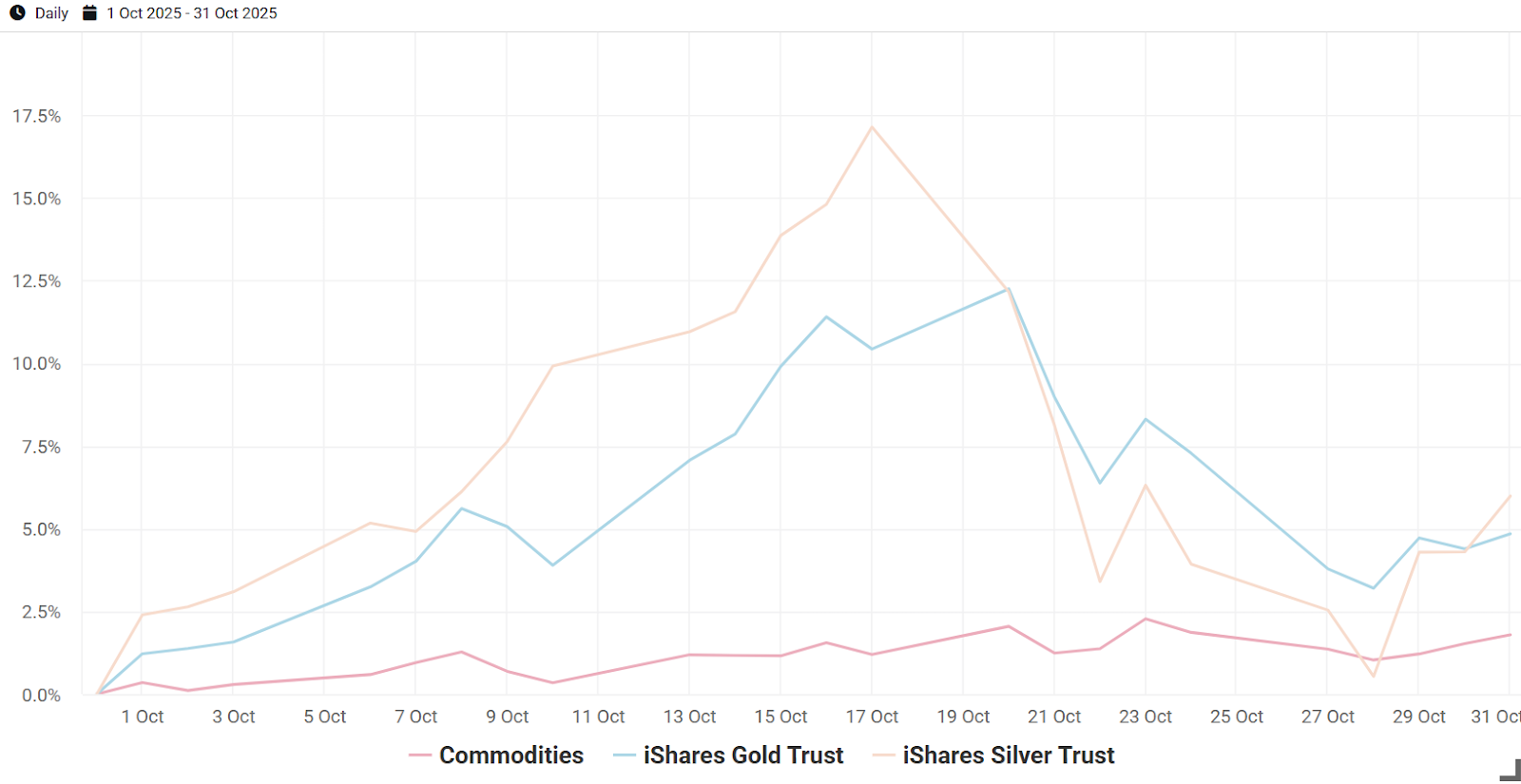

Commodities: Broad commodities benefited from strength in precious metals, though those assets lost much of their gains late in the month. Gold and Silver, which were approximately 19% and 6% of our Commodities factor’s raw input at the start of October, rose 4.85% and 5.99%, respectively. Demand drivers included their perceived roles as safe‑haven and inflation‑hedging assets, expectations for U.S. rate cuts, and continued central‑bank buying.

Exhibit 3: October Performance of Venn’s Commodities Factor and Gold and Silver

Source: Venn by Two Sigma.

Source: Venn by Two Sigma.

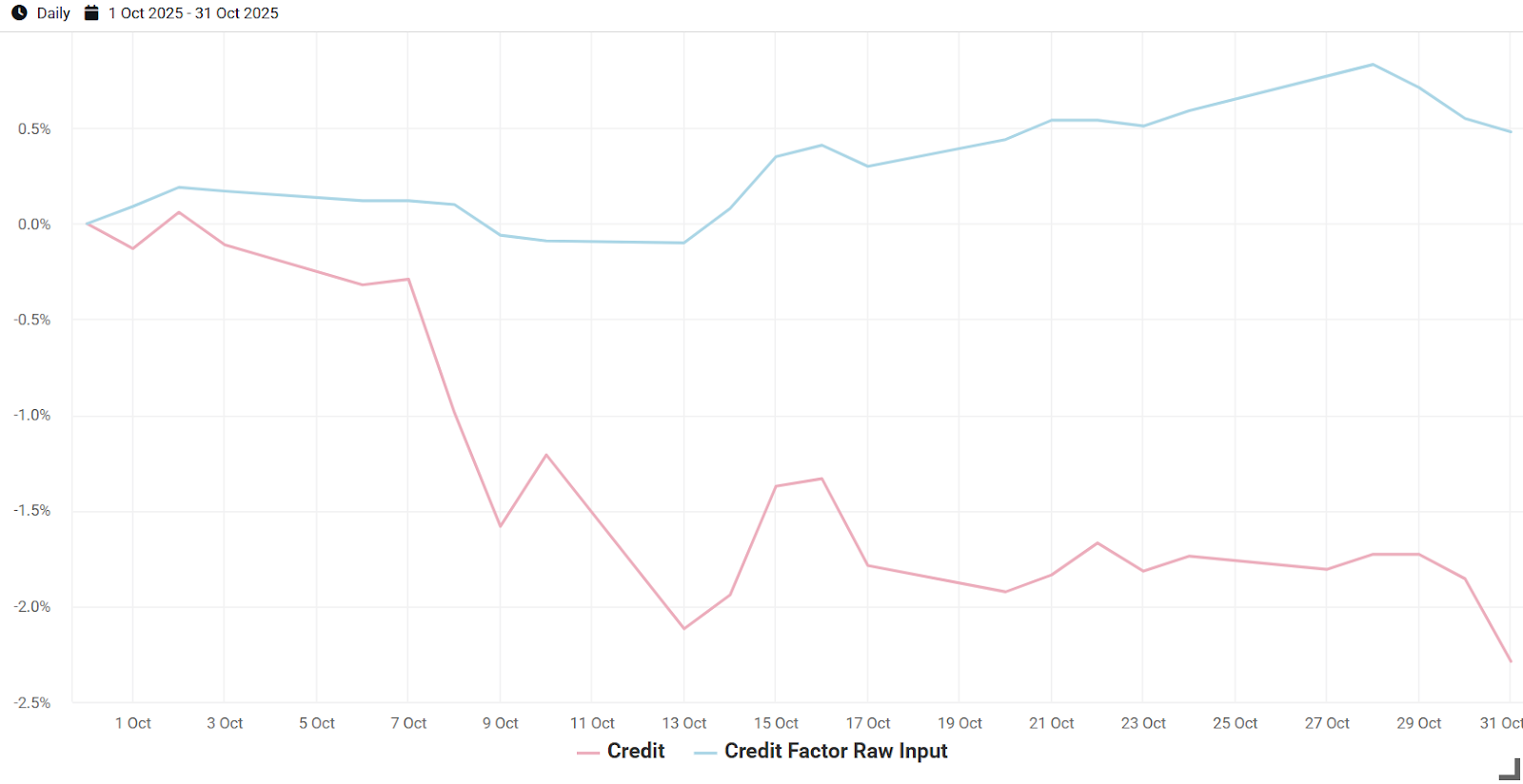

Credit: The raw input of our Credit factor was positive in October, returning 0.48%. However, after removing overlapping risk with our Equity and Interest Rates factors the factor turned deeply negative. Using our tier system, this suggests investors with credit exposure may have been compensated more for equity and rates beta than for exposure to corporate default risk. For portfolios seeking purer credit risk exposure, a factor‑aware, decorrelated approach may be critical to separate these exposures and clearly understand risk and return drivers.

Exhibit 4: October Performance of Venn’s Credit Factor and its Raw Input

Source: Venn by Two Sigma.

Source: Venn by Two Sigma.

Tier 3 Secondary Core Macro Factors

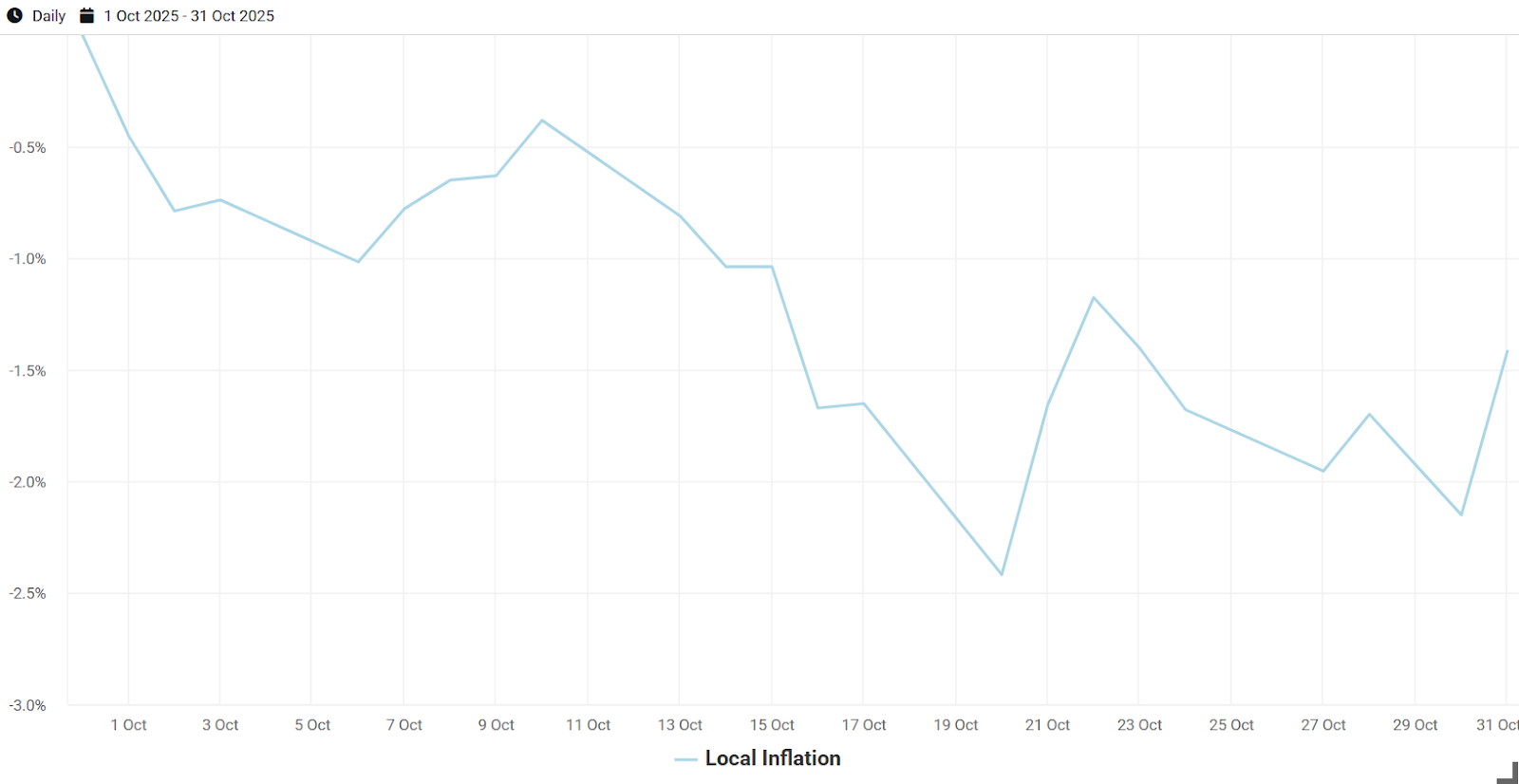

Local Inflation: In a recent piece, we detailed the Local Inflation factor’s interpretation, recent behavior, and portfolio use cases. In short, the factor reflects the value of a local hedge against unique inflation dynamics. It fell sharply in October, echoing September’s decline as inflation expectations softened.

Late in the month, Powell noted that a December rate cut was “far from a foregone conclusion”,2 which supported a modest rebound in our factor as he indirectly highlighted the potential near‑term role of a local inflation hedge.

Exhibit 5: October Performance of Venn’s Local Inflation Factor

Source: Venn by Two Sigma.

Source: Venn by Two Sigma.

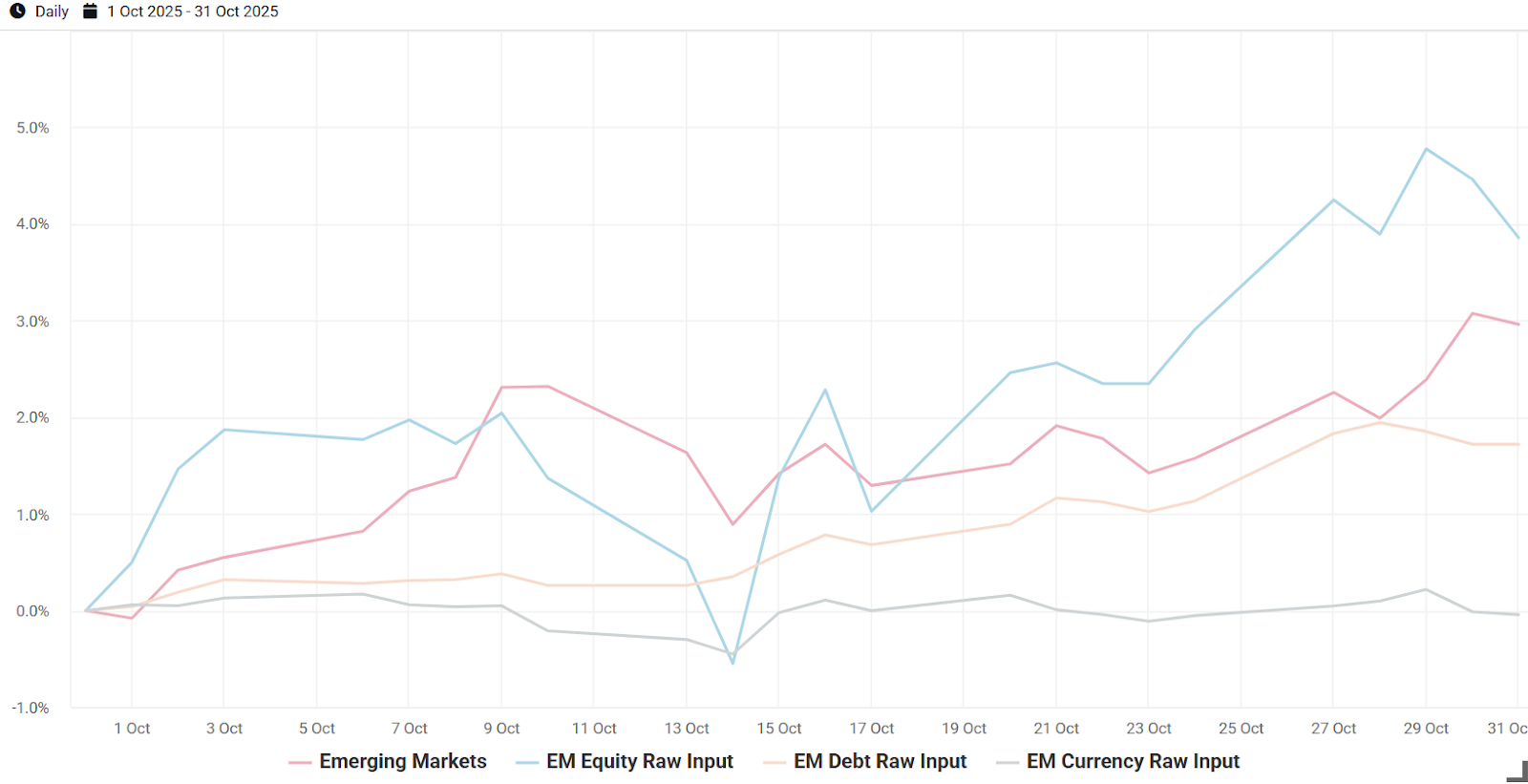

Emerging Markets: Designed to be decorrelated from higher‑tier macro factors, our Emerging Markets factor has historically not earned a persistent risk premium. October was quite the exception, with the factor rising 2.98%. The raw input consists of EM equities, debt, and currencies, of which the first two were positive.

Ongoing U.S. policy and growth concerns provided a relative tailwind to non‑U.S. equity markets, including EM (this is partly evidenced by negative Local Equity factor returns as well). Attractive real yields, supported by many EM central banks moving earlier on rate cuts, have likely boosted demand for EM debt.3 It would be easy to think that the falling USD benefited these raw inputs as well, but the USD actually rebounded in October, up 2.07% as measured by the DXY Index.4

Exhibit 6: October Performance of Venn’s Emerging Markets Factor and its Underlying Raw Inputs

Source: Venn by Two Sigma.

Source: Venn by Two Sigma.

Equity and Macro Style Factors

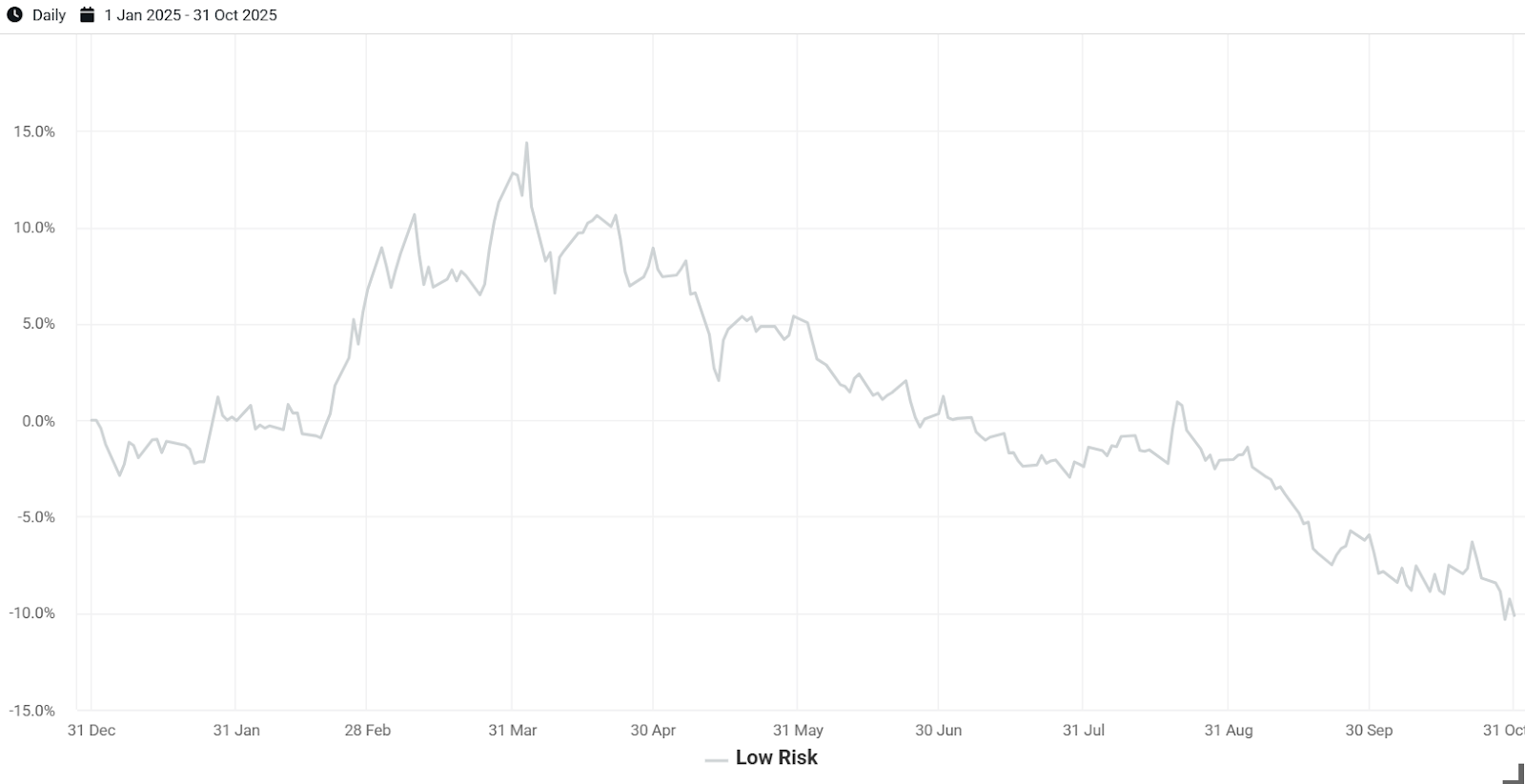

Low Risk: Venn’s equity styles are long/short exposures that aim to be market‑neutral over long periods. During the transition to a new U.S. administration and evolving tariff policy, Low Risk initially outperformed as investors favored lower‑volatility securities. As markets digested data on tariffs and inflation, and concerns about persistently higher inflation eased, the subsequent risk‑on rally weighed on Low Risk, which has trended lower since “Liberation Day”.

Exhibit 7: YTD Performance of Venn’s Low Risk Factor

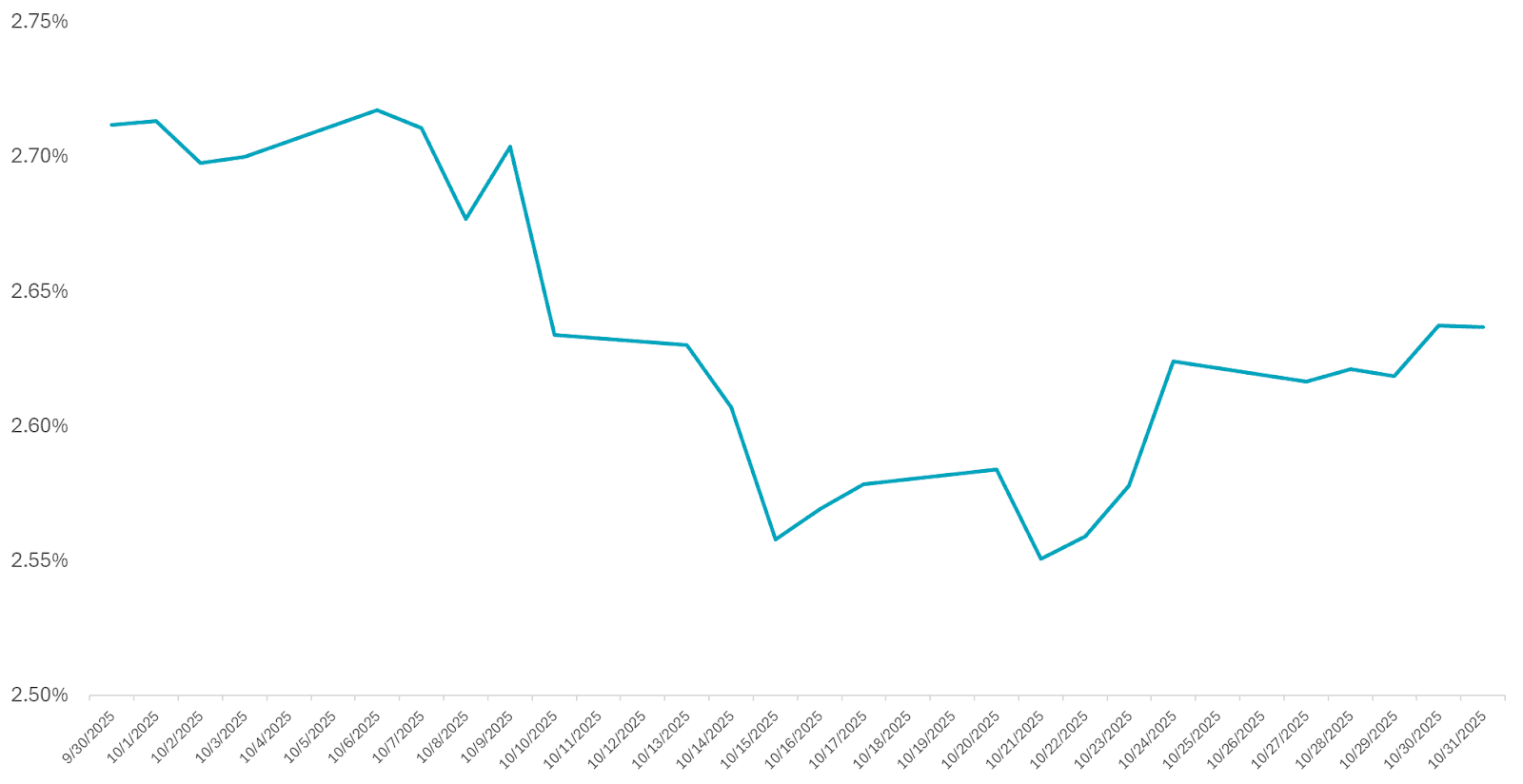

Fixed Income Carry: This factor captures return from being long higher‑yielding developed‑market 10‑year bond futures and short lower‑yielding ones, using each country’s term spread.

Looking at the raw input, a long position in the 10‑year German Bund drove most of the positive return in October. Bund prices rallied mid‑month as investors sought safe‑haven assets amid elevated U.S. and China trade tensions. Its yield also fell alongside rising expectations for an ECB rate cut by July 2026. The Bund often serves as a proxy for the broader euro area and can be sensitive to ECB policy.5

Exhibit 8: October Yields of the 10-Year German Bund

Source: Venn by Two Sigma, EDI.

Source: Venn by Two Sigma, EDI.

References

1 https://www.ft.com/content/c4b2c5d9-c82f-401e-b763-bc9581019cb7

5 https://fixedincome.fidelity.com/ftgw/fi/FINewsArticle?id=202510140445RTRSNEWSCOMBINED_6N3VU0MT_1

Exposure to risk factors is not a guarantee of increased performance or decreased risk. References to the Two Sigma Factor Lens and other Venn methodologies are qualified in their entirety by the applicable documentation on Venn.

This article is not an endorsement by Two Sigma Investor Solutions, LP or any of its affiliates (collectively, “Two Sigma”) of the topics discussed. The views expressed above reflect those of the authors and are not necessarily the views of Two Sigma. This article (i) is only for informational and educational purposes, (ii) is not intended to provide, and should not be relied upon, for investment, accounting, legal or tax advice, and (iii) is not a recommendation as to any portfolio, allocation, strategy or investment. This article is not an offer to sell or the solicitation of an offer to buy any securities or other instruments. This article is current as of the date of issuance (or any earlier date as referenced herein) and is subject to change without notice. The analytics or other services available on Venn change frequently and the content of this article should be expected to become outdated and less accurate over time. Two Sigma has no obligation to update the article nor does Two Sigma make any express or implied warranties or representations as to its completeness or accuracy. This material uses some trademarks owned by entities other than Two Sigma purely for identification and comment as fair nominative use. That use does not imply any association with or endorsement of the other company by Two Sigma, or vice versa. See the end of the document for other important disclaimers and disclosures. Click here for other important disclaimers and disclosures.