Recently we wrote about how factors on Venn by Two Sigma are orthogonal to each other, meaning that we create independent factors to decompose risk and return for investments and portfolios. In that post, we showed an example of how our equity factor appeared to be the largest driver of risk for a high-yield fixed income index. This emphasized the importance of using independent risk factors to understand diversification, rather than a traditional asset class framework.

In this piece, we get more specific on how we use a process called residualization to seek factor independence, provide an example of how it’s done, and share our thoughts on applying it more broadly within the Two Sigma Factor Lens.

Using Residualization to Unbias “Home Bias”

Residualization can be a mouthful, but it’s a surprisingly simple concept. Much in the way that residue is what's “left over,” the goal of residualization is to isolate leftover risk after accounting for other entangled or correlated risks.

Let’s take an example such as our Local Equity Factor. This factor aims to capture equity home bias, or the tendency to invest in domestic over foreign equity. In our view, global equity risk1 muddies the waters when trying to isolate the impact of our Local Equity Factor on portfolios. Remove the relationship with global equity, and we believe you are left with an independent risk factor that helps explain performance of an investor’s local equity market.

Now let’s take a look at how we conduct the residualization process2 for the worst day in our Local Equity Factor’s history, Black Monday, or October 19th, 1987.

- Step 1: Quantify the relationship of global equities with US equities.3 This is done by considering global equity performance and running a regression to measure US equities’ sensitivity to that performance (more specifically, US equities’ trailing 3-year beta to global equities). 4

- Step 2: Remove global equities’ relationship by subtracting it from US equity performance.

Source: Venn by Two Sigma. For illustration purposes only.

After accounting for the relationship with global equities, we see above that US home bias in portfolios was a headwind on the infamous Black Monday. Specifically, our Local Equity Factor was down more than -6%.

While this example highlights how residualization can isolate an individual risk factor, we believe the benefits of residualization are even greater when applied across a holistic set of risk factors. It can also be especially useful for individual factors that might benefit from being residualized to multiple other factors.

This leads to a discussion about residualization across the broader Two Sigma Factor Lens.

Expanding Residualization to Broader and More Entangled Risks

The Two Sigma Factor Lens aims to provide a practical framework to analyze risk in investments and portfolios, via the use of a curated list of independent factors. To achieve this, we approach residualization with a tier system, which ultimately seeks low to zero correlations across our risk factor pairs over time.

Related to the chart below:

- Tier 1 Core Macro Factors are considered to be the most liquid and are not residualized against anything.

- Tier 2 Core Macro Factors are residualized against Tier 1 Core Macro Factors.

- Tier 3 Secondary Core Macro Factors are residualized against both Tier 2 and Tier 1 Core Macro Factors.

- Local Equity, Equity Short Volatility and Foreign Exchange Carry are only residualized against the Equity Factor, while Fixed Income Carry is only residualized against the Interest Rates Factor.

- Trend Following and our equity styles: Low Risk, Momentum, Quality, Value, Small Cap, and Crowding, undergo no residualization.

- Trend Following is intended to capture active managers' short- to medium-term trend-following behavior, which can take long or short directional risk in different factors at different times. Trend following positioning does not provide the consistency to benefit from residualization.

- Equity styles generally exhibit naturally low correlations across the factor lens, but importantly are designed to be equity market neutral in their construction rather than through residualization.

- Trend Following is intended to capture active managers' short- to medium-term trend-following behavior, which can take long or short directional risk in different factors at different times. Trend following positioning does not provide the consistency to benefit from residualization.

The Two Sigma Factor Lens Residualization Approach to Seek Independent Factors

Source: Venn by Two Sigma. For illustration purposes only.

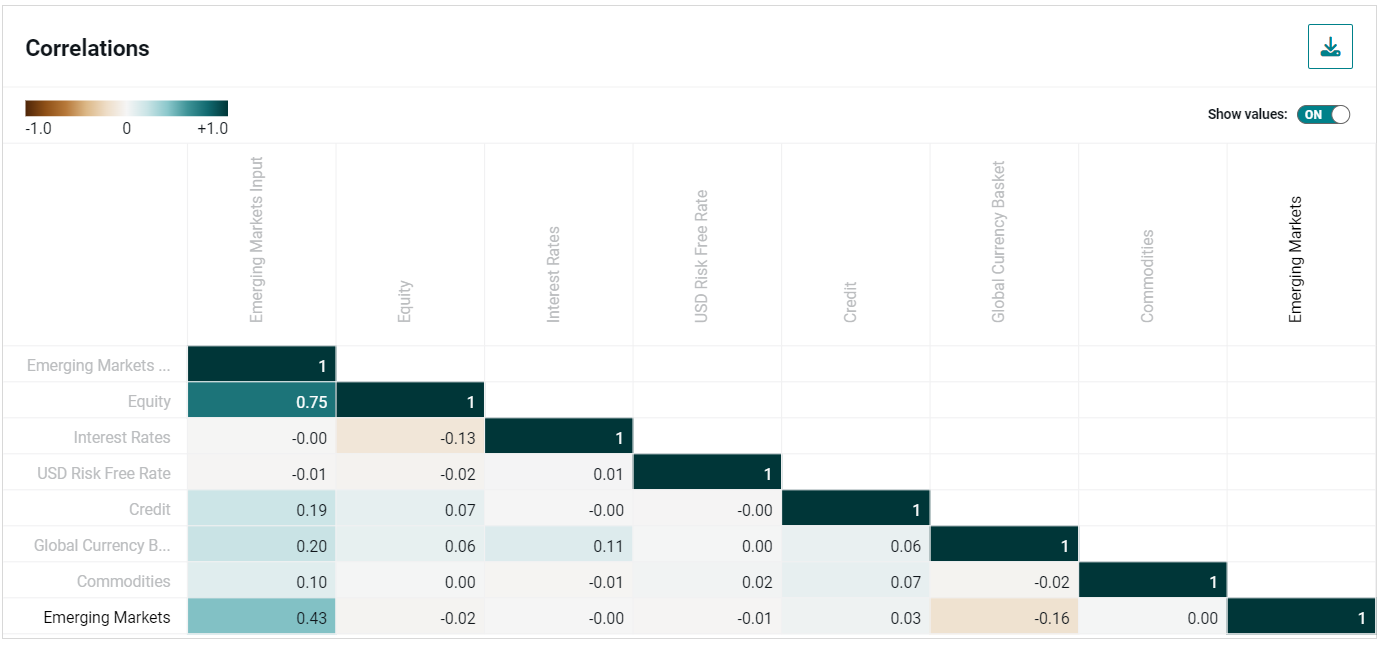

As an example, our Emerging Markets (EM) Factor represents EM risk that is above and beyond embedded Equity, Interests Rates, Credit, and Commodities risk. We believe that without residualization, it can be difficult to understand the true impact of EM exposure on investments without mistaking it for a mix of these other factors.

This is evidenced by examining the properties of our EM Factor before residualization. Specifically, its correlation with our Equity Factor is a meaningful 0.75 historically (as shown in the correlation matrix below), which implies significant overlapping risk. After residualization, the EM Factor has a correlation of virtually 0 with our Equity Factor. Working from the raw input, rather than the residualized Emerging Markets Factor, may lead to less informed and less precise asset allocation decisions.

Correlations of Emerging Markets to Inputs Before and After Residualization

- Emerging Markets Input = Before Residualization

- Emerging Markets = After Residualization

Source: Venn by Two Sigma. The chart displays a correlation matrix for the Emerging Markets Factor in the Two Sigma Factor Lens over its full history from 11/9/1994–11/23/2023

What are Expected Results from Applying this Residualization System?

When analyzing assets in Venn, this residualization process has the effect of increasing the amount of risk assigned to higher-order factors such as Equity and Interest Rates. For example, the large majority of risk correlated to equity returns (such as moves driven by shocks to global growth expectations or investor risk aversion) will be consolidated in Equity Factor exposure, regardless of what asset initially generated that risk. This is intended to provide a truer picture of the total risk contribution of assets, avoiding the illusion of diversification from similar risks contributed by many different asset classes.

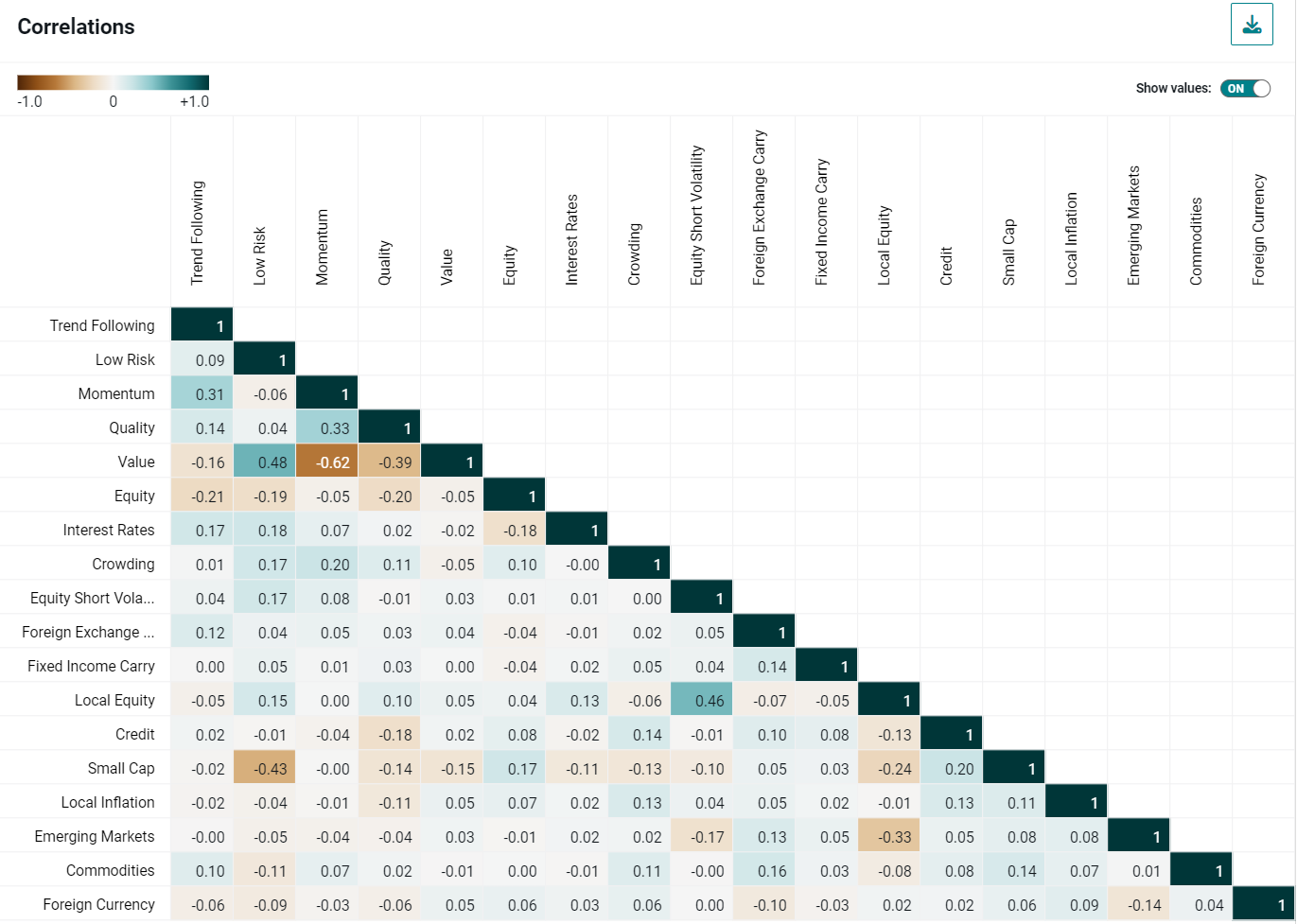

Another result is that virtually all correlations between our factor pairs are low or close to zero over their full shared histories. We believe this makes analyzing multi-asset portfolios and interpreting sources of risk a more reliable and straightforward exercise. Put another way, relatively dispersed exposure to multiple factors in the Two Sigma Factor Lens suggests that the portfolio is diversified among many independent sources of return.

Source: Venn by Two Sigma. The chart displays a correlation matrix for all 18 factors in the Two Sigma Factor Lens over their full history from 10/3/1997–11/23/2023

Combining Technology and Quantitative Insights to Get More Clear on Risk

A difficult challenge for allocators is not only to holistically analyze multi-asset portfolios, but also to disentangle how unique sources of risk affect their portfolio sleeves, managers, or individual holdings. Venn by Two Sigma uses residualization to quantify these unique sources of risk, and helps identify where in the portfolio they can be found.

References

1 This refers to Venn’s Equity Factor, which is represented by currency hedged global equities.

2 For illustration purposes we removed consideration of the risk-free rate which is typically accounted for in the factor construction and residualization process.

3 This example is given using the USD lens of the Two Sigma Factor Lens. As a result, the Local Equity Factor captures a home bias from investing in US equities over foreign equities.

4 Specifically, Venn’s residualization involves a rolling multivariate, exponentially-weighted regression using rolling 5-day returns. The lookback period is 3 years, and the half-life is 6 months. We use a shorter time horizon for the rolling residualization window than most institutional investor time frames. Our research indicated that this specification was a long enough lookback period such that the factor relationships weren't overly sensitive or noisy. And it was short enough to capture changes in factor relationships during volatile market environments like 2008 or the recent COVID-19 market crisis.

This article is not an endorsement by Two Sigma Investor Solutions, LP or any of its affiliates (collectively, “Two Sigma”) of the topics discussed. The views expressed above reflect those of the authors and are not necessarily the views of Two Sigma. This article (i) is only for informational and educational purposes, (ii) is not intended to provide, and should not be relied upon, for investment, accounting, legal or tax advice, and (iii) is not a recommendation as to any portfolio, allocation, strategy or investment. This article is not an offer to sell or the solicitation of an offer to buy any securities or other instruments. This article is current as of the date of issuance (or any earlier date as referenced herein) and is subject to change without notice. The analytics or other services available on Venn change frequently and the content of this article should be expected to become outdated and less accurate over time. Any statements regarding planned or future development efforts for our existing or new products or services are not intended to be a promise or guarantee of future availability of products, services, or features. Such statements merely reflect our current plans. They are not intended to indicate when or how particular features will be offered or at what price. These planned or future development efforts may change without notice. Two Sigma has no obligation to update the article nor does Two Sigma make any express or implied warranties or representations as to its completeness or accuracy. This material uses some trademarks owned by entities other than Two Sigma purely for identification and comment as fair nominative use. That use does not imply any association with or endorsement of the other company by Two Sigma, or vice versa. See the end of the document for other important disclaimers and disclosures. Click here for other important disclaimers and disclosures.

This article may include discussion of investing in virtual currencies. You should be aware that virtual currencies can have unique characteristics from other securities, securities transactions and financial transactions. Virtual currencies prices may be volatile, they may be difficult to price and their liquidity may be dispersed. Virtual currencies may be subject to certain cybersecurity and technology risks. Various intermediaries in the virtual currency markets may be unregulated, and the general regulatory landscape for virtual currencies is uncertain. The identity of virtual currency market participants may be opaque, which may increase the risk of market manipulation and fraud. Fees involved in trading virtual currencies may vary.