This report reviews how key risk factors responded to that rate cut, but let’s first review Two Sigma Factor Lens performance for the full month.

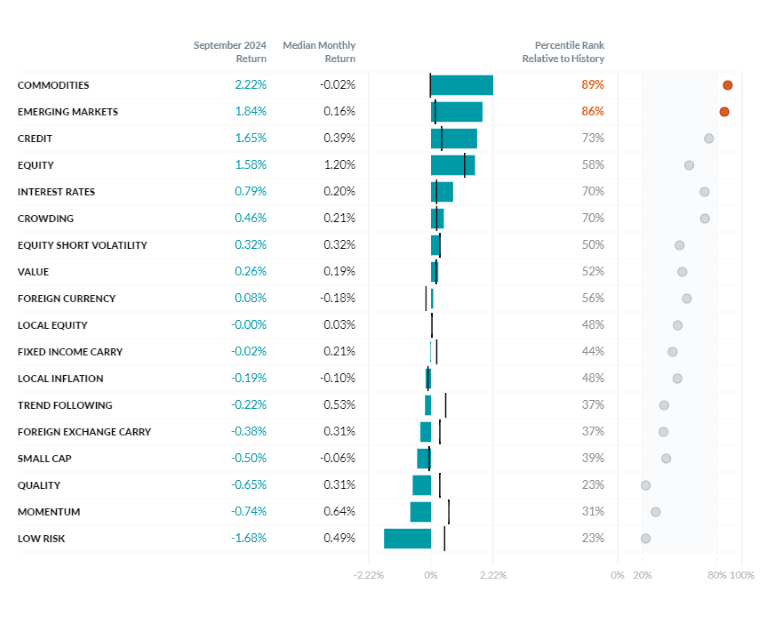

Exhibit 1: Two Sigma Factor Lens Performance in September

©2024 Two Sigma Investments, LP. This image is for informational purposes only. See https://www.venn.twosigma.com/blog-disclaimer for more disclaimers and disclosures.

Source: Venn by Two Sigma. The median and percentile columns measure the performance of each factor in the Two Sigma Factor Lens relative to the entire history of the factor in USD, using monthly data for the period Oct 1997 - September 2024

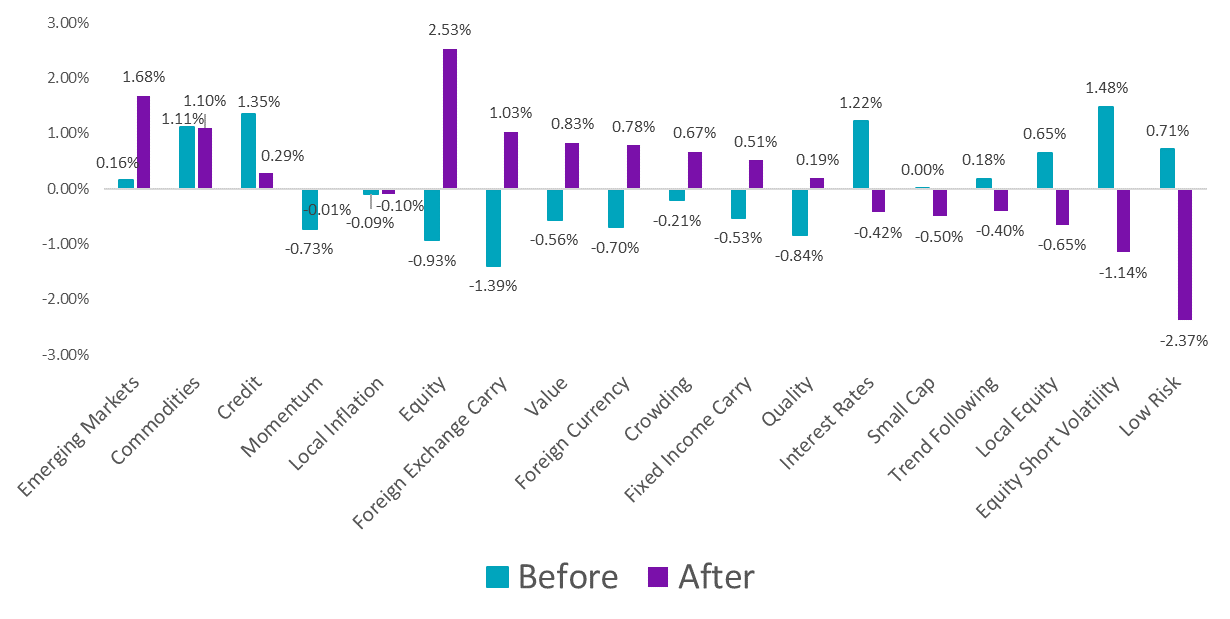

Two Sigma Factor Lens Performance Before and After the September Fed Cut

In Exhibit 2, we show performance of the Two Sigma Factor Lens before and after the cut, with some clear themes emerging. For example, of our 18 factors, 13 changed the sign of their performance before and after. This highlights the significant change in sentiment across these fundamental risks in the market.

Exhibit 2: Two Sigma Factor Lens Performance Before and After the U.S. Rate Cut

Source: Venn by Two Sigma

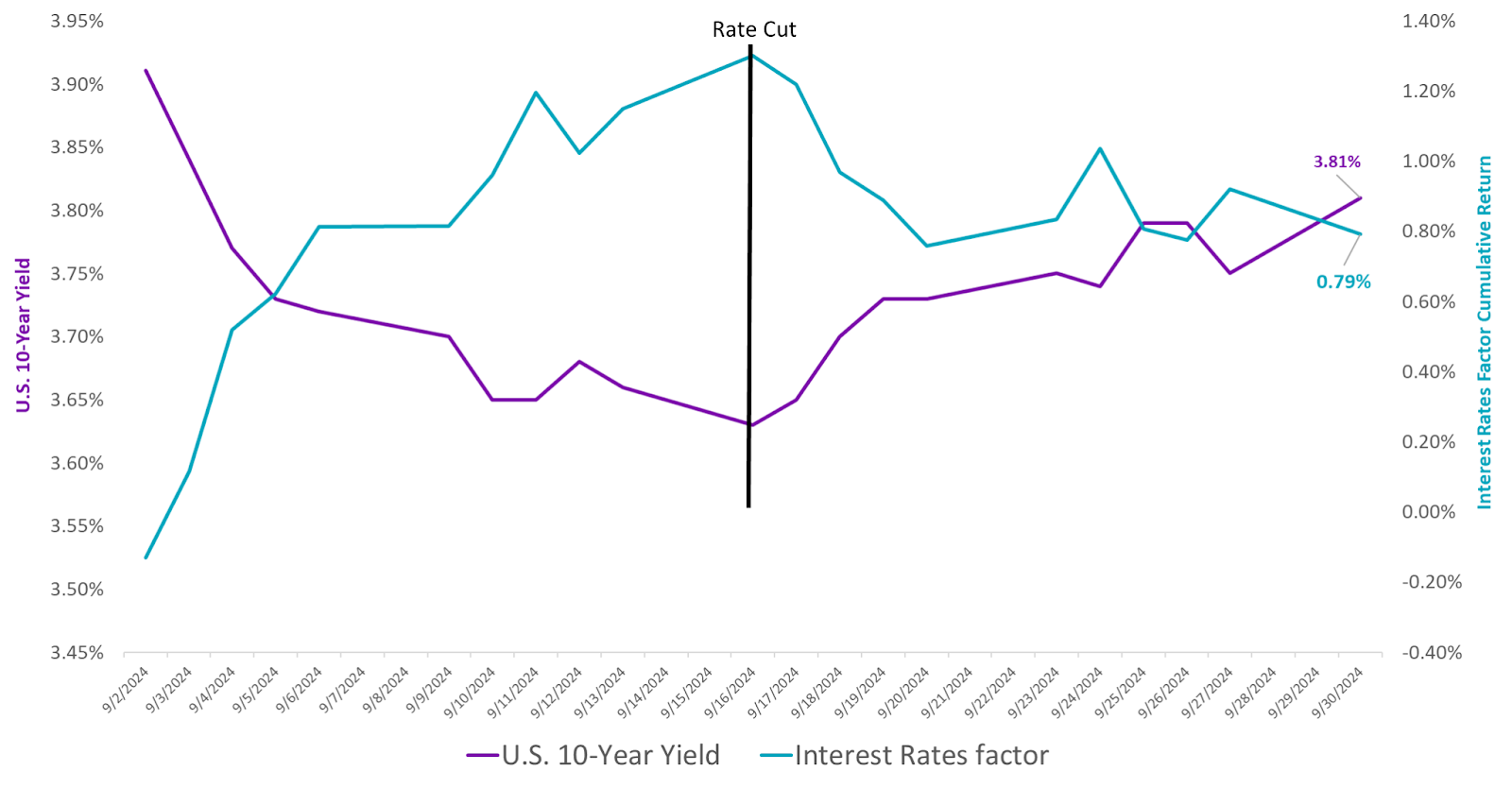

Interest Rates: The 10-year U.S. bond yield fell before the Fed cut, and rose after. This resulted in positive performance for our Interest Rates factor initially, followed by negative performance after the cut.2

Rising 10-year yields afterwards may indicate expectations of stronger economic growth or higher future inflation, which can decrease demand for long-term fixed income as investors seek higher returns elsewhere.

Exhibit 3: Interest Rates Factor September Performance

Source: Venn by Two Sigma and ST.LOUIS FED

Shorter-term yields, such as the 3-month T-Bill, fell both before and after, which ultimately led to a steeper U.S. yield curve. Many market participants have reported that the curve has finally “uninverted”. While true for the 10-year minus the 2-year, it is still inverted when using the 3-month yield on the short end. Side Note: the 10-yr minus the 3-month is the term spread signal used for our Fixed Income Carry factor.

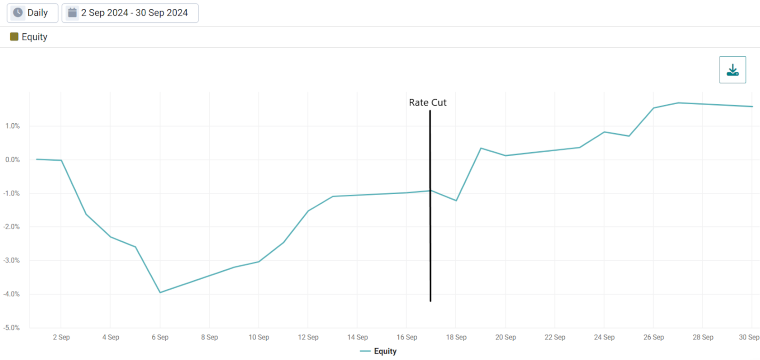

Equity: In Equity markets, reactions to the cut were a bit delayed. Risk appetite developed overnight rather than the day the cut occurred. Indeed, our Equity factor rallied 1.58% on the following day but fell 0.30% on the day of the announcement. This speaks to how equity markets were caught off guard by the size of the hike, but ultimately responded favorably.

Exhibit 4: Equity Factor September Performance

Source: Venn by Two Sigma

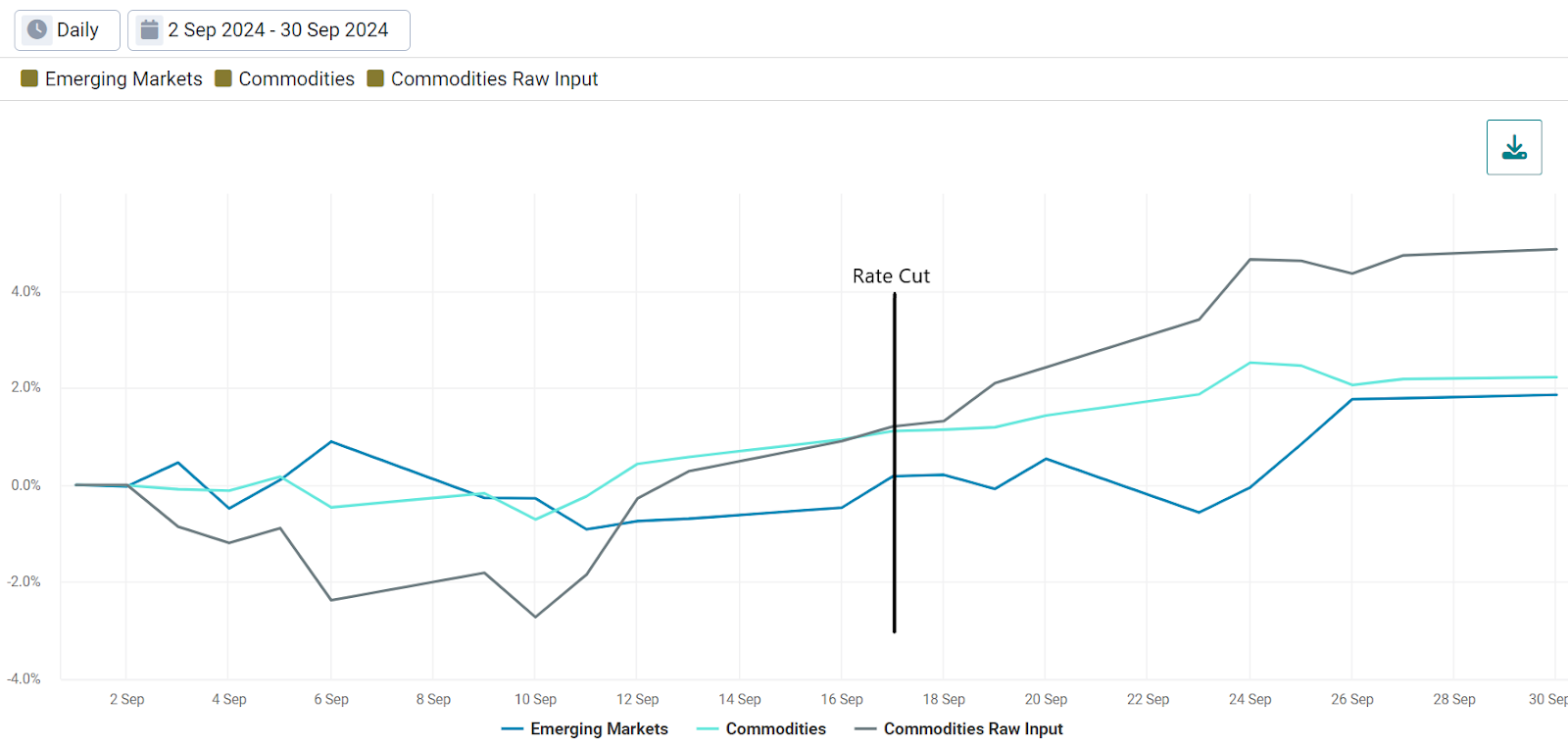

Emerging Markets and Commodities3: Both of these factors were positive throughout the month, despite the rate cut changing the market narrative. This consistency likely led to their differentiated performance (Exhibit 1), while other factors were less notable. For example, many factors in Exhibit 2 ended the month with near zero, or historically insignificant performance. Performance swings before and after the cut tended to cancel each other out.

In the case of our Emerging Markets factor, there was much more to the story. Its large rally came the week after the U.S. rate cut, and was driven by local stimulus in China.4 More specifically, Chinese equities were up 22.64% after the cut and through the end of the month.5

However, the consistency of our Emerging Markets factor in September goes beyond Chinese equity performance. For example, before the Fed cut, Chinese equities were down -0.97%, but our EM factor was still positive.

Our Commodity factor rose steadily throughout the month (after an initial dip), without a notable reaction to the Fed cut. This might seem counterintuitive given that many broad commodity indexes jumped on the news, but our Commodity factor is designed to measure the excess return beyond exposure to Equities, Interest Rates, and Currencies. Removing these entangled exposures facilitated smoother Commodities performance throughout the month (see the raw input in Exhibit 5).

In fact, as we mentioned in the Equity section, we also see a delayed reaction in our Commodity factor raw input, reacting sharply on the following trading day. This highlights how our raw input is entangled with equities before Venn decorrelates the two.

Exhibit 5: Emerging Markets and Commodities Factor September Performance

Source: Venn by Two Sigma

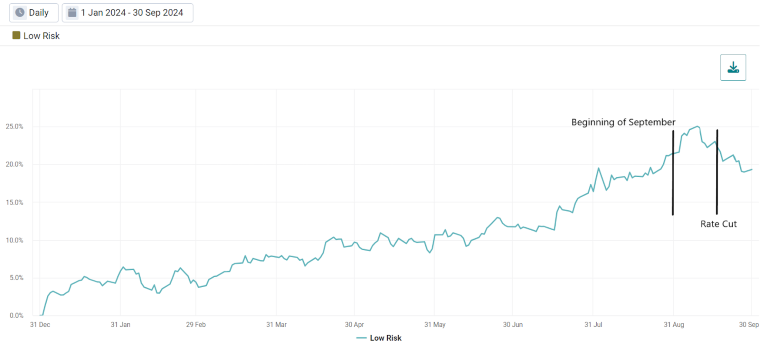

Low Risk: This factor exhibited meaningful volatility throughout the month, and while it fell the day of the Fed’s announcement, it had already been trending downward from its highs. It is worth noting that Low Risk is the best performing factor in our lens year-to-date (up 19.29%), outperforming the second-best factor (Equity) by almost 5%.

YTD performance may be surprising as many low risk exposures, such as low volatility equity ETFs, have underperformed market-cap weighted benchmarks.6 However, many low volatility exposures are naturally at odds with the Equity risk premium due to their lower equity beta. Our Low Risk factor is long/short and beta-neutral, aiming to be independent with our Equity factor. This seeks to create independent performance even when equity markets are rallying.

The beginning of the downward trend of our Low Risk factor in September may continue if investor optimism continues to show relatively more interest in higher risk securities.

Exhibit 6: Year-to-Date Low Risk Factor Performance

Source: Venn by Two Sigma

References

1 https://www.barrons.com/livecoverage/august-jobs-report-today?mod=article_inline

2 Our Interest Rates factor captures long exposure to 7-10 year currency hedged global bonds.

3 Both of these factors undergo residualization to seek independence with other factors in the Two Sigma Factor lens. More specifically, both are orthogonalized with Equity and Interest Rates. The Emerging Markets factor is also orthogonalized with our Commodity and Credit factors.

5 Chinese Equities: represented by the iShares MSCI China ETF (MCHI). As of 10/4/2024, China was 29.51% of the iShares MSCI Emerging Markets ETF (EEM).

6 For example, the iShares Minimum Volatility ETF (USMV) and the Invesco S&P 500 Low Volatility ETF (SPLV) were up 18.55% and 16.31% YTD respectively, while the S&P 500 was up 22.05%.

References to the Two Sigma Factor Lens and other Venn methodologies are qualified in their entirety by the applicable documentation on Venn.

This article is not an endorsement by Two Sigma Investor Solutions, LP or any of its affiliates (collectively, “Two Sigma”) of the topics discussed. The views expressed above reflect those of the authors and are not necessarily the views of Two Sigma. This article (i) is only for informational and educational purposes, (ii) is not intended to provide, and should not be relied upon, for investment, accounting, legal or tax advice, and (iii) is not a recommendation as to any portfolio, allocation, strategy or investment. This article is not an offer to sell or the solicitation of an offer to buy any securities or other instruments. This article is current as of the date of issuance (or any earlier date as referenced herein) and is subject to change without notice. The analytics or other services available on Venn change frequently and the content of this article should be expected to become outdated and less accurate over time. Two Sigma has no obligation to update the article nor does Two Sigma make any express or implied warranties or representations as to its completeness or accuracy. This material uses some trademarks owned by entities other than Two Sigma purely for identification and comment as fair nominative use. That use does not imply any association with or endorsement of the other company by Two Sigma, or vice versa. See the end of the document for other important disclaimers and disclosures. Click here for other important disclaimers and disclosures.