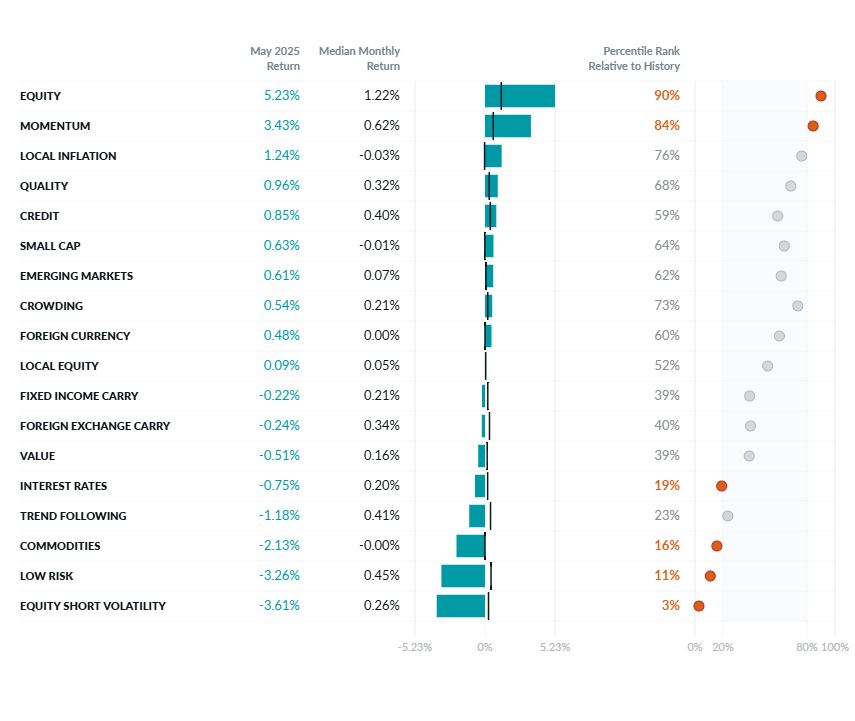

Let’s start by reviewing performance in May (Exhibit 1).

Exhibit 1: May Performance of the Two Sigma Factor Lens ©2025 Two Sigma Investments, LP. This image is for informational purposes only. See https://www.venn.twosigma.com/blog-disclaimer for more disclaimers and disclosures. Source: Venn by Two Sigma. The median and percentile columns measure the performance of each factor in the Two Sigma Factor Lens relative to the entire history of the factor in USD, using monthly data for the period August 1998 - May 2025.

©2025 Two Sigma Investments, LP. This image is for informational purposes only. See https://www.venn.twosigma.com/blog-disclaimer for more disclaimers and disclosures. Source: Venn by Two Sigma. The median and percentile columns measure the performance of each factor in the Two Sigma Factor Lens relative to the entire history of the factor in USD, using monthly data for the period August 1998 - May 2025.

Core Macro Factors

Equity Factor: This factor rose 5.23% in May, continuing its recovery from early April lows, supported by generally positive trade headlines and reduced tariff concerns. Additionally, since our market-cap-weighted global equity factor allocates over 60% to the U.S., a strong end to the U.S. earnings season provided a meaningful tailwind. According to FactSet's latest Earnings Insight report, 98% of S&P 500 companies have reported as of the end of May, with 78% reporting positive EPS surprises.1 The S&P 500 is also on track for year-over-year earnings growth of 13.3%.2

Interest Rates Factor: This factor declined 0.75% in May as global yields rose. Similar to our Equity factor commentary, the U.S. took center stage after Moody's downgraded U.S. debt due to tax cuts reducing revenues, ballooning debt, and rising interest rates increasing payments, among other factors. However, rising yields were more than just a U.S. phenomenon. In Japan, for example, the 10-year yield rose by almost 15%, or 18 bps, after a weak treasury auction.3

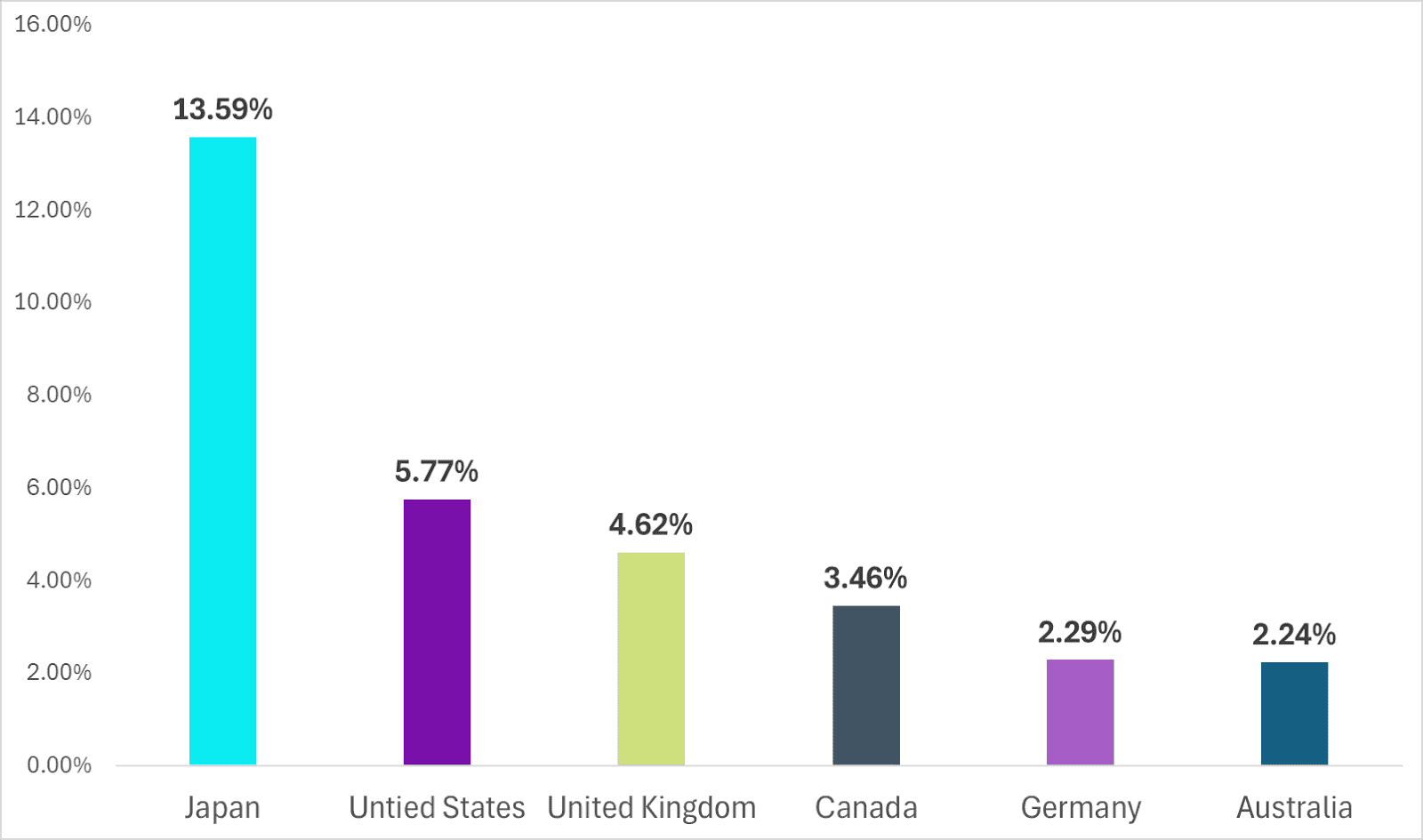

Exhibit 2: Percent Increase of 10-Yr Sovereign Bond Yields in May4

Source: Venn by Two Sigma and Bloomberg. Absolute yields to start and end the month were as follows: Japan 1.31%–1.49%, U.S. 4.16%–4.40%, United Kingdom 4.44%–4.65%, Canada 3.09%–3.20%, Germany 2.44%–2.50%, Australia 4.16%–4.26%.

Secondary Core Macro Factors

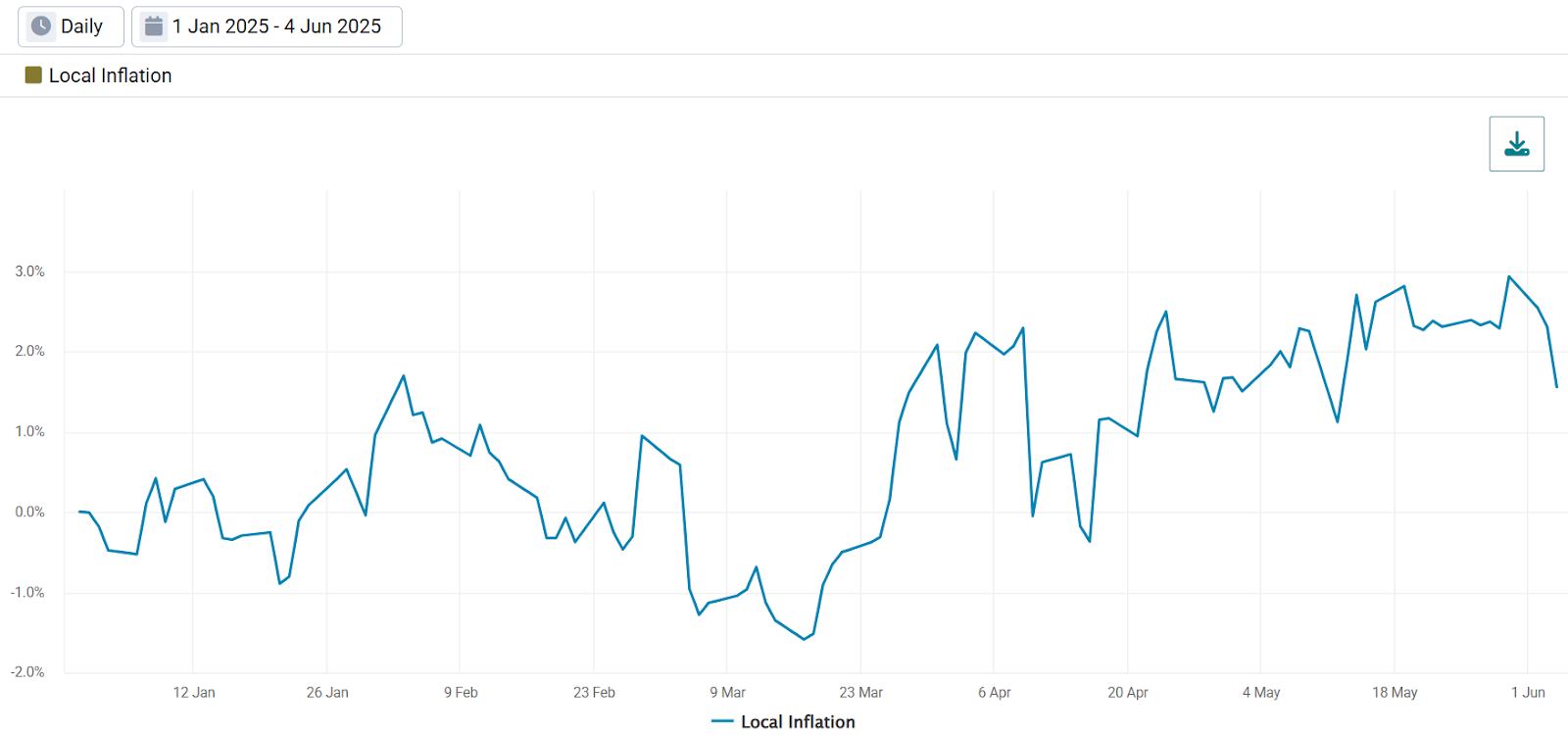

Local Inflation Factor: This factor gained 1.24% in May, implying that inflation hedges in U.S. bond markets have been adding value for investors. Our Local Inflation factor captures this dynamic above and beyond movements in our Equity, Interest Rates, Credit, and Commodities factors.

This positive return is likely due to the continued expectation that tariffs will add meaningfully to inflation in the future, despite higher inflation not yet materializing. Looking at Local Inflation factor performance YTD (Exhibit 3) strongly suggests that inflation hedges have been increasingly rewarded as trade wars became more concrete, around the end of Q1.

Exhibit 3: Local Inflation Factor Cumulative Return YTD

Source: Venn by Two Sigma

Source: Venn by Two Sigma

Macro Styles

Equity Short Volatility Factor: Our implementation of this factor measures the premium investors receive from providing insurance against higher volatility, above and beyond movements in equity markets themselves. This factor fell 3.61% in May and is now down more than 10% YTD, implying a meaningful increase in volatility relative to what would be expected given moves in our Equity factor. Unlike the Local Inflation factor that benefited as tariff negotiations started becoming real, the Equity Short Volatility factor suffered. This underscores the exceptional volatility that tariffs have introduced beyond what is captured by our Equity factor.

Exhibit 4: Equity Short Volatility Factor Cumulative Return YTD

Source: Venn by Two Sigma

Source: Venn by Two Sigma

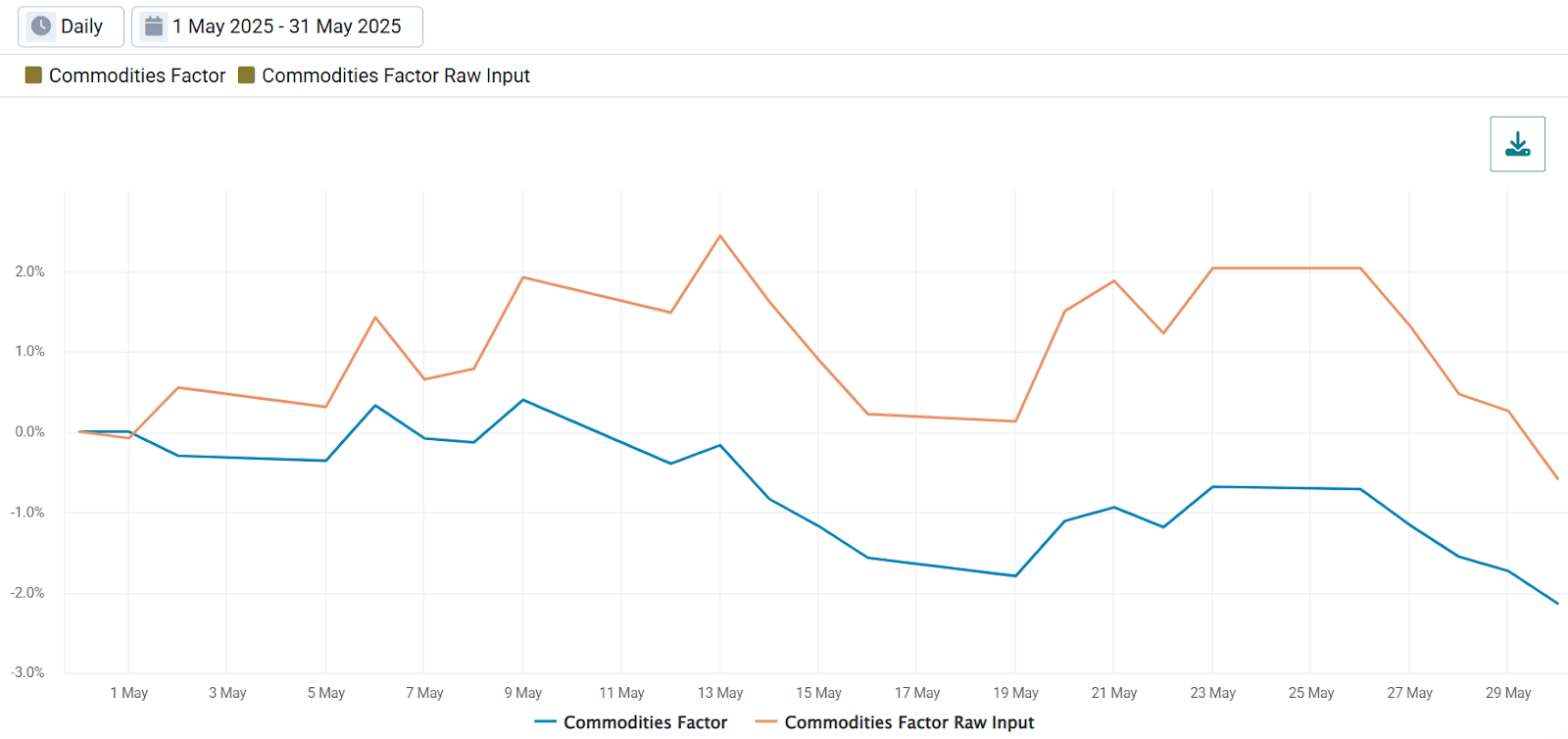

Commodities Factor: This factor had a historically difficult month, declining 2.13%, meaning institutional investors with this exposure also experienced a drag on returns. The raw input of our Commodities factor, before decorrelating it with Equity and Interest Rates factors, was down a more modest 0.58%. Put another way, for those not taking an independent factor approach, positive correlation with equities likely dampened the negative performance of commodities in May.

Exhibit 5: Commodities Raw Input and Final Factor Cumulative Return In May

Source: Venn by Two Sigma

Source: Venn by Two Sigma

Equity Styles

Momentum and Low Risk Factors: We have written about the negative correlation between these two factors a few times this year, which appears to have continued. In May, Momentum posted a historically strong month at 3.43%, and Low Risk a historically weak one at -3.26%. However, when looking at YTD returns, both are positive (Exhibit 6).

Exhibit 6: Momentum and Low Risk Cumulative Return YTD

Source: Venn by Two Sigma

Source: Venn by Two Sigma

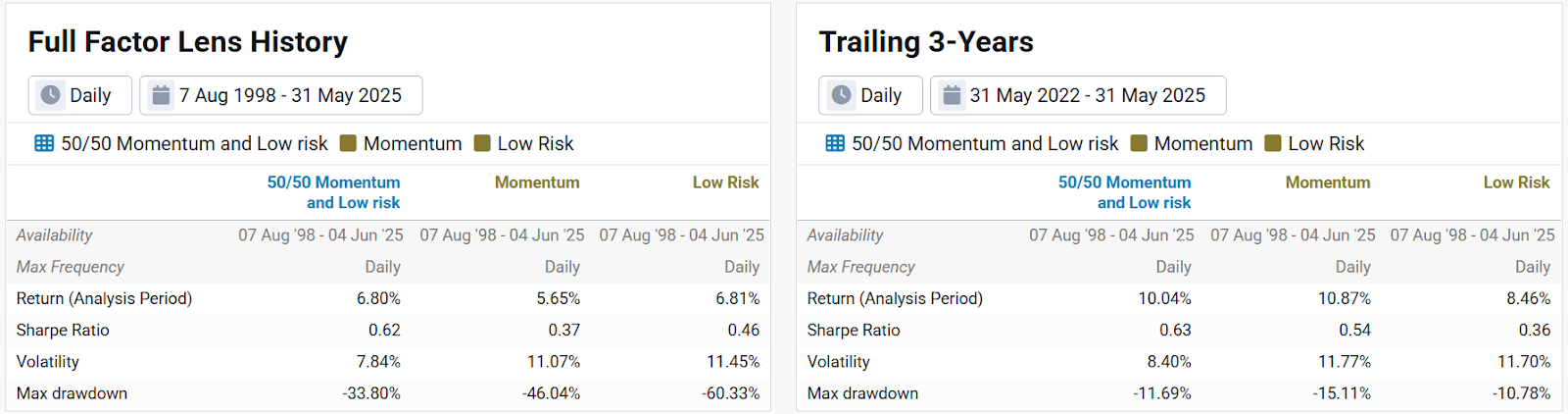

As a simple thought exercise, we combined these two factors into a 50/50 portfolio to look at performance and risk over both the long and short term. In both cases, combining these factors led to a significantly higher Sharpe ratio.

Going back to 1998, we observed a Sharpe ratio of 0.62 vs. 0.37 for Momentum alone, and 0.46 for Low Risk alone. This was achieved through similar returns but a roughly 30% reduction in volatility. While our factors are not directly investable, for an allocator, it may be worth considering how a portfolio with exposure to both of these factors might benefit over long periods of time.

Exhibit 7: Performance of a 50/50 Momentum and Low Risk Portfolio

Source: Venn by Two Sigma. Portfolio rebalanced quarterly.

Source: Venn by Two Sigma. Portfolio rebalanced quarterly.

References

4Id.

4As a side note, currency and bond movements in Japan, especially relative to the U.S., have us keeping a close eye on our Carry factors in the coming months!

References to the Two Sigma Factor Lens and other Venn methodologies are qualified in their entirety by the applicable documentation on Venn.

This article is not an endorsement by Two Sigma Investor Solutions, LP or any of its affiliates (collectively, “Two Sigma”) of the topics discussed. The views expressed above reflect those of the authors and are not necessarily the views of Two Sigma. This article (i) is only for informational and educational purposes, (ii) is not intended to provide, and should not be relied upon, for investment, accounting, legal or tax advice, and (iii) is not a recommendation as to any portfolio, allocation, strategy or investment. This article is not an offer to sell or the solicitation of an offer to buy any securities or other instruments. This article is current as of the date of issuance (or any earlier date as referenced herein) and is subject to change without notice. The analytics or other services available on Venn change frequently and the content of this article should be expected to become outdated and less accurate over time. Two Sigma has no obligation to update the article nor does Two Sigma make any express or implied warranties or representations as to its completeness or accuracy. This material uses some trademarks owned by entities other than Two Sigma purely for identification and comment as fair nominative use. That use does not imply any association with or endorsement of the other company by Two Sigma, or vice versa. See the end of the document for other important disclaimers and disclosures. Click here for other important disclaimers and disclosures.