When making informed asset allocation decisions, investors ideally combine information about the past with educated views about the future. To help them do this, Venn provides portfolio and investment-level forecasts using the Two Sigma Factor Lens methodology.

We believe our long-term annualized factor returns are a neutral starting point for return expectations for long investment horizons under the assumption that our factors tend to be mean-reverting and stable over long periods. We also account for investments’ recent factor exposures and residual returns when calculating forecasts.

Forecast Return Calculation

forecast return = (factor exposures x factor returns) + residual return + cash return1

Venn’s default forecast returns are meant to serve as a potential baseline for making forward-looking asset allocation decisions. However, we recognize that investors have a myriad of investment outlooks and capital market assumptions that are often dynamic in nature.

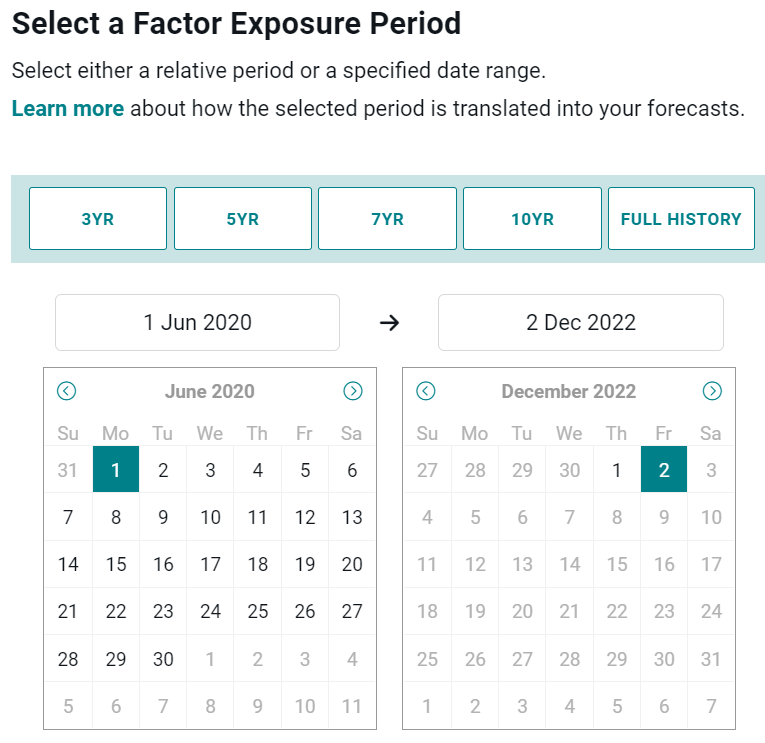

Customizing Forecasts: Factor Exposures

Venn allows users to customize the factor exposure period. The default exposure period is the latest 3 years (or at least 12 months depending on data availability), which users can adjust to any period of time. This may be especially useful for clients who would like to remove abnormal market movements (e.g., early 2020 due to the Covid-19 pandemic) from the default factor exposure period.

Source: Venn by Two Sigma. For illustrative purposes only.

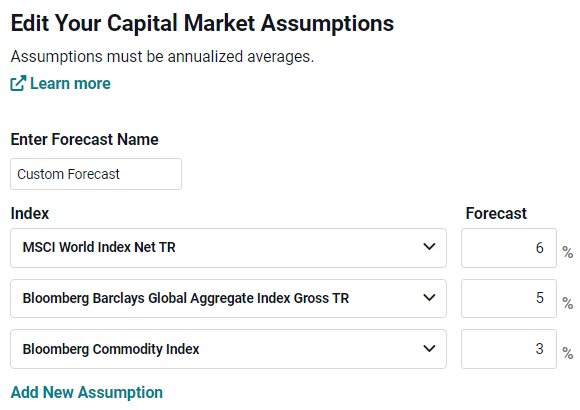

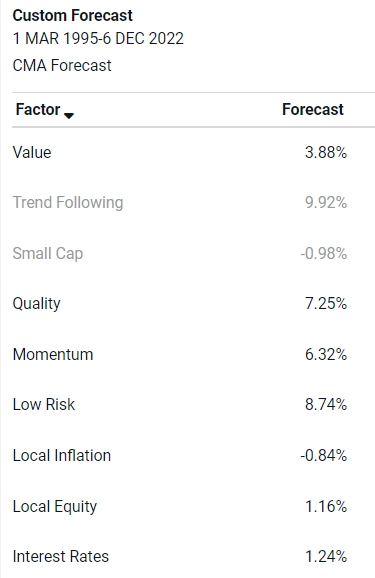

Customizing Forecasts: Factor Returns

Users can input their own capital market assumptions by assigning expected return values to select market indices. We then translate these views into custom factor return forecasts for the factors within the Two Sigma Factor Lens.

⇨

⇨

Source: Venn by Two Sigma. For illustrative purposes only.

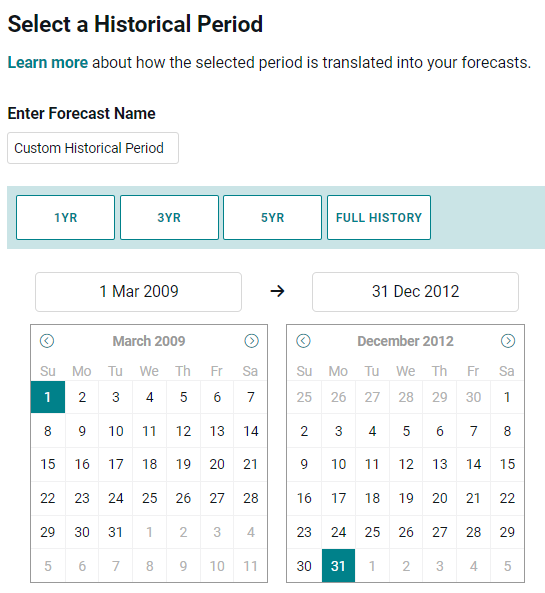

Alternatively, users can choose to customize the historical lookback periods for factor returns. Venn’s default lookback period for factor return forecasts goes back to March 1, 1995, but users can modify the default to choose any period of time to reflect their forecast views. For example, one could choose to generate forecasts based on the recovery period following the Global Financial Crisis.

Source: Venn by Two Sigma. For illustrative purposes only.

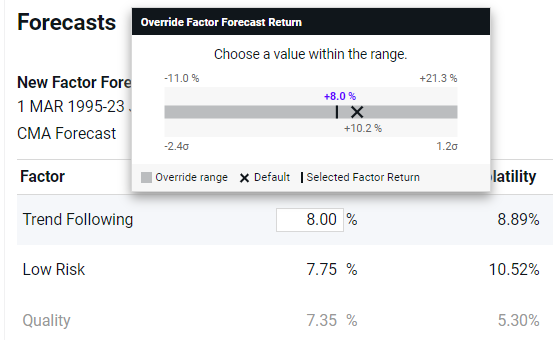

Additionally, clients have the ability to directly override factor return forecasts. Whether or not they choose to implement the above customization options, this feature allows users to directly modify the default or updated factor return forecasts. For example, a user may input a custom forecast return for the Trend Following factor.

Source: Venn by Two Sigma. For illustrative purposes only.

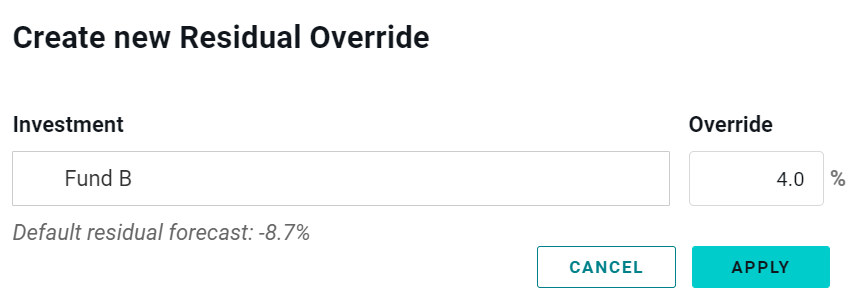

Customizing Forecasts: Residual Return

Clients also have the flexibility to override forecast residual returns. Residual is the component of an investment’s return that is unexplained by the Two Sigma Factor Lens. While this is the closest metric that Venn has to “alpha,” it is important to note that residual can also represent other known, unknown, or indescribable factors that are simply not included in our factor lens. The default residual forecast is an investment’s most recent residual return (either 3 years or at least 12 months depending on data availability).

Users can customize the residual return to impart specific views on residual forecasts that are not reflective of recent periods. For example, one may wish to adjust a residual forecast for a fund that recently implemented a manager change based on poor performance.

Source: Venn by Two Sigma. For illustrative purposes only.

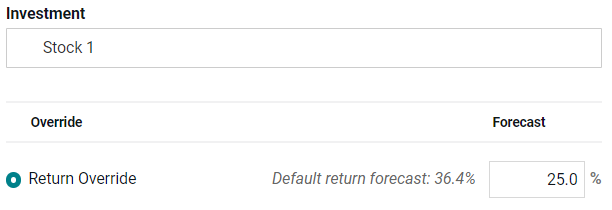

Customizing Forecasts: Investment-Level Return

Another Venn feature enables clients to modify investment-level forecast returns. This allows users to input their views for any individual investments in their portfolios. For example, a user might have an alternate view on an equity stock’s forecast and can override the default with their own forecast return.

Source: Venn by Two Sigma. For illustrative purposes only.

Venn by Two Sigma has a wide range of clients with a multitude of investment beliefs and market assumptions. We aim to provide a stable foundation for forecast metrics using long-term annualized factor returns while giving clients the flexibility to reflect their own views. Ultimately, we believe factor-based forecasting with customizability may help allocators make more informed asset allocation decisions.

References

1 Venn factor returns are considered net of cash so cash return must be added back when forecasting investment returns

This article is not an endorsement by Two Sigma Investor Solutions, LP or any of its affiliates (collectively, “Two Sigma”) of the topics discussed. The views expressed above reflect those of the authors and are not necessarily the views of Two Sigma. This article (i) is only for informational and educational purposes, (ii) is not intended to provide, and should not be relied upon, for investment, accounting, legal or tax advice, and (iii) is not a recommendation as to any portfolio, allocation, strategy or investment. This article is not an offer to sell or the solicitation of an offer to buy any securities or other instruments. This article is current as of the date of issuance (or any earlier date as referenced herein) and is subject to change without notice. The analytics or other services available on Venn change frequently and the content of this article should be expected to become outdated and less accurate over time. Any statements regarding planned or future development efforts for our existing or new products or services are not intended to be a promise or guarantee of future availability of products, services, or features. Such statements merely reflect our current plans. They are not intended to indicate when or how particular features will be offered or at what price. These planned or future development efforts may change without notice. Two Sigma has no obligation to update the article nor does Two Sigma make any express or implied warranties or representations as to its completeness or accuracy. This material uses some trademarks owned by entities other than Two Sigma purely for identification and comment as fair nominative use. That use does not imply any association with or endorsement of the other company by Two Sigma, or vice versa. See the end of the document for other important disclaimers and disclosures. Click here for other important disclaimers and disclosures.

This article may include discussion of investing in virtual currencies. You should be aware that virtual currencies can have unique characteristics from other securities, securities transactions and financial transactions. Virtual currencies prices may be volatile, they may be difficult to price and their liquidity may be dispersed. Virtual currencies may be subject to certain cybersecurity and technology risks. Various intermediaries in the virtual currency markets may be unregulated, and the general regulatory landscape for virtual currencies is uncertain. The identity of virtual currency market participants may be opaque, which may increase the risk of market manipulation and fraud. Fees involved in trading virtual currencies may vary.