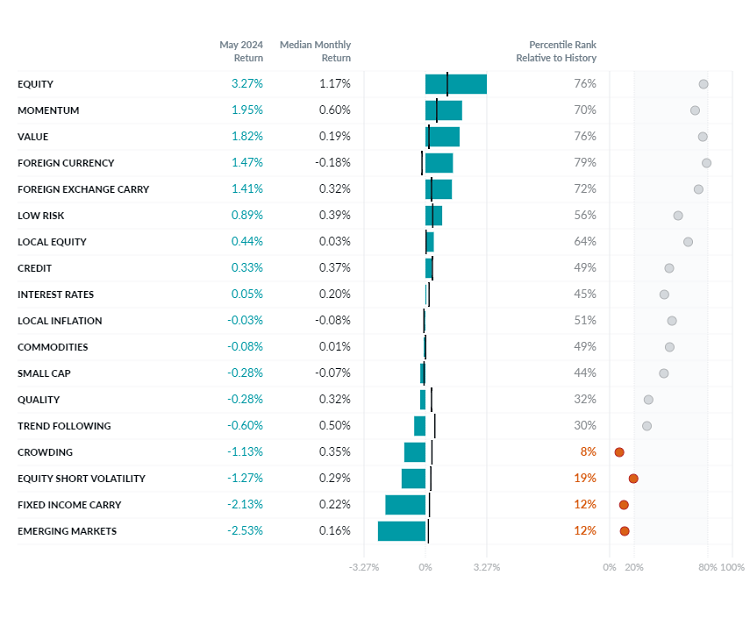

Exhibit 1: May Performance of the Two Sigma Factor Lens

©2024 Two Sigma Investments, LP. This image is for informational purposes only. See https://www.venn.twosigma.com/blog-disclaimer for more disclaimers and disclosures.

Source: Venn by Two Sigma. The median and percentile columns measure the performance of each factor in the Two Sigma Factor Lens relative to the entire history of the factor in USD, using monthly data for the period Oct 1997 - May 2024

Understanding Our Crowding Factor

Before diving into May's performance, a brief overview of our Crowding factor may help to set the stage.

Given that we can’t precisely know the total portfolio of all investors, it is common to leverage market variables that may be indicators of aggregate views. For publicly traded equities, one such market variable is short interest. For this reason, our Crowding factor is short U.S. stocks with high short interest and long those with low short interest. It's true that a stock may be shorted due to investors pursuing other known equity styles, but our Crowding factor aims to capture short interest above and beyond those strategies.

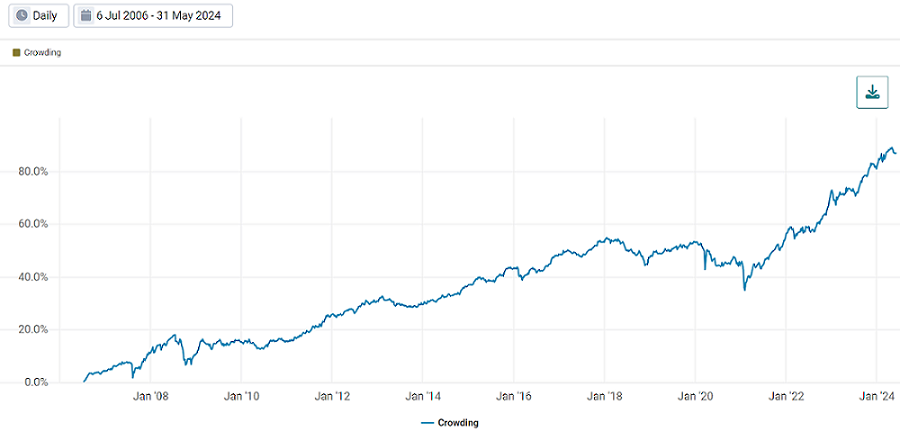

All six of our equity styles represent institutionally popular factors that are associated with return premiums. For Crowding, this means there is an expectation that high short interest stocks will underperform low short interest stocks over time. Historical data of our factor supports this, showing that over time investors have been compensated for short selling risks (Exhibit 2), such as short squeezes—which we will explore next.

Exhibit 2: Historical Performance of Our Crowding Factor

Source: Venn by Two Sigma

Have Meme Stocks Altered the Ability for Short Sellers to Generate Alpha?

Meme stocks are fueled by the fact that they have high short interest. This leads to retail investors coordinating to drive their price higher as they seek to be a part of the meme movement or seek staggering short-term gains. This may then cause short sellers to buy the stock at a higher price to close their position. Somewhat ironically, the actions of both parties work together to push the price higher thus facilitating a “short squeeze”. Given that Crowding aims to short U.S securities with high short interest, meme stocks are likely in its short portfolio.

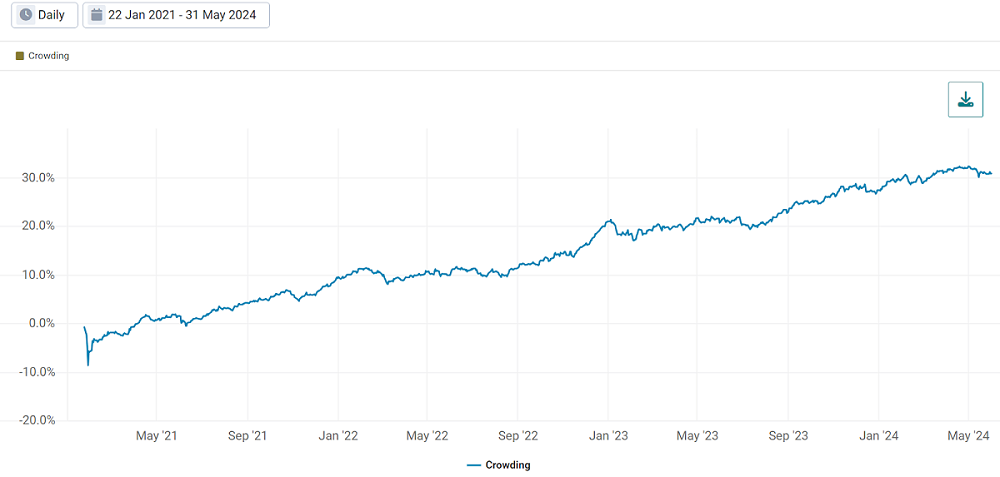

With all of this being said, Crowding is still up over 30% since January 22, 2021, when GameStop acted as the genesis for the meme stock phenomenon over three years ago.

Exhibit 3: Historical Performance of Our Crowding Factor Since the First Meme Stock Short Squeeze

Source: Venn by Two Sigma

More than Memes Driving May Performance for Crowding

While we typically refrain from isolating specific securities within our factors, below we take a closer look at three stocks in our Crowding’s short portfolio that tell an interesting story. These stocks were meaningful contributors to negative returns in May due to their substantial market rallies and significant short positions. Each stock’s rally was driven by unique circumstances, underscoring the varied risks associated with short squeezes. It may be the case that short sellers exposed to these securities experienced disproportionately large drawdowns in the month of May.

- Microstrategy: As the largest corporate owner of Bitcoin, Microstrategy's shares surged 43% following a broader Bitcoin rally and news of its inclusion in the MSCI World Index.

- Novavax: This biotechnology company experienced a 247% increase after securing a licensing deal for its Covid-19 vaccine.

- GameStop: True to its reputation as a meme stock, GameStop’s shares climbed 109%, fueled by X/Twitter activity and coordinated efforts by retail investors.

Crowding: Risks and Reward Revisited

Amid the buzz surrounding meme stocks, the performance of our Crowding factor in May highlights some interesting points. Primarily, it is important to recognize that short squeezes represent a perennial risk for short sellers, and can come from a variety of sources.

This risk has been magnified by the recent meme stock phenomenon, but in the same way it has historically, our Crowding factor has continued to generate positive returns. This highlights that there has still been a positive return premium associated with the aggregate views of investors, above and beyond what can be found in known and popular equity styles.

References

References to the Two Sigma Factor Lens and other Venn methodologies are qualified in their entirety by the applicable documentation on Venn.

This article is not an endorsement by Two Sigma Investor Solutions, LP or any of its affiliates (collectively, “Two Sigma”) of the topics discussed. The views expressed above reflect those of the authors and are not necessarily the views of Two Sigma. This article (i) is only for informational and educational purposes, (ii) is not intended to provide, and should not be relied upon, for investment, accounting, legal or tax advice, and (iii) is not a recommendation as to any portfolio, allocation, strategy or investment. This article is not an offer to sell or the solicitation of an offer to buy any securities or other instruments. This article is current as of the date of issuance (or any earlier date as referenced herein) and is subject to change without notice. The analytics or other services available on Venn change frequently and the content of this article should be expected to become outdated and less accurate over time. Two Sigma has no obligation to update the article nor does Two Sigma make any express or implied warranties or representations as to its completeness or accuracy. This material uses some trademarks owned by entities other than Two Sigma purely for identification and comment as fair nominative use. That use does not imply any association with or endorsement of the other company by Two Sigma, or vice versa. See the end of the document for other important disclaimers and disclosures. Click here for other important disclaimers and disclosures.