Exhibit 1: April Performance of the Two Sigma Factor Lens

©2024 Two Sigma Investments, LP. This image is for informational purposes only. See https://www.venn.twosigma.com/blog-disclaimer for more disclaimers and disclosures.

Source: Venn by Two Sigma. The median and percentile columns measure the performance of each factor in the Two Sigma Factor Lens relative to the entire history of the factor in USD, using monthly data for the period Oct 1997 - April 2024

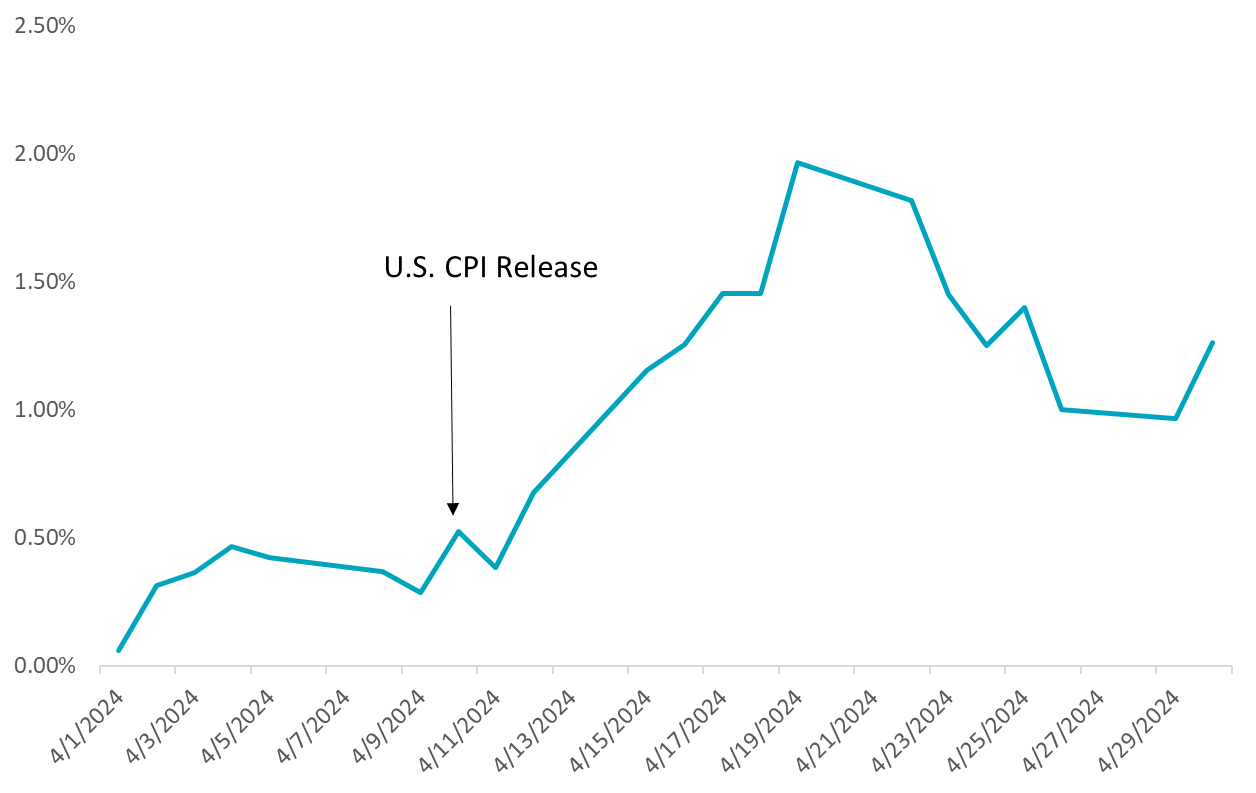

- Value: After U.S. inflation exceeded expectations, the tech sector grappled with prospects of increased borrowing costs and the diminished present value of their future cash flows. Value benefited from this dynamic due to its meaningful net short position to this sector. Below we show the positive contribution to return driven by Value’s short tech position in April, and how it jumped around the release of higher than expected U.S. CPI numbers.

Exhibit 2: Tech Sector Contribution to Return for the Value Factor

Source: Venn by Two Sigma

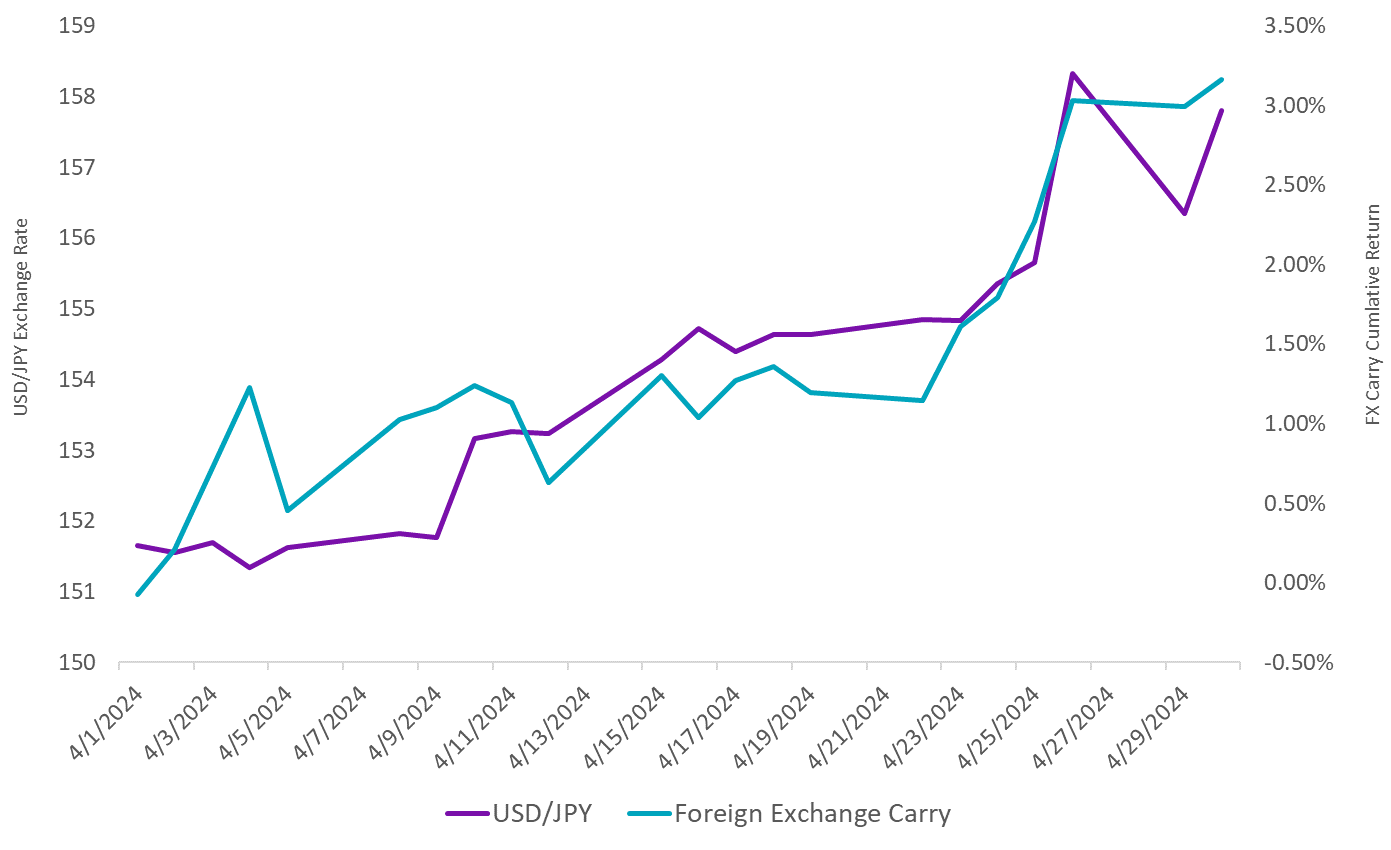

- Foreign Exchange Carry: Interest rate differentials are used to determine this factor’s positioning, meaning it goes long high yielding currencies and short lower yielding ones. Our FX Carry factor encompasses all G10 currencies, but the performance of the USD and JPY were significant in April. The JPY significantly depreciated (short position), while the USD appreciated (long position). This positively impacted FX carry performance. This happened as U.S. interest rates rose due to anticipated extended periods of higher rates, while the Bank of Japan decided to keep rates unchanged.3

Exhibit 3: USD/JPY Exchange Rate and FX Carry Performance

Source: Bloomberg, Venn by Two Sigma

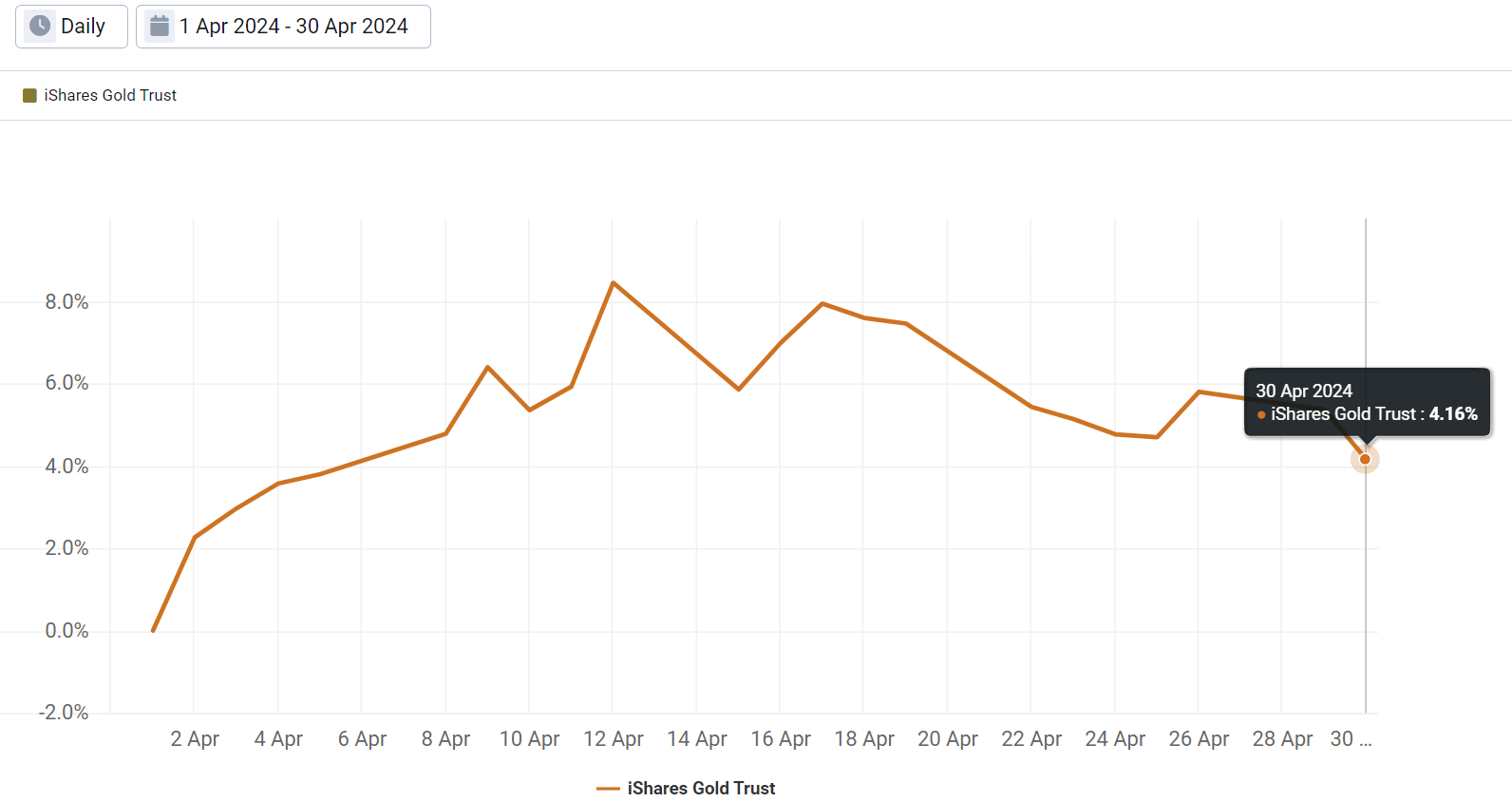

- Commodities: Metals were strong performers in April, contributing to our Commodity factor’s positive return. Gold, representing around 15% of Venn’s raw commodity factor input, was meaningfully positive. Rising rates and a strong USD have historically been headwinds for gold, but geopolitical risk in the Middle East may be causing investors to focus on its perceived safe haven value instead.

Exhibit 4: Gold’s Performance in April

Source: Venn by Two Sigma

- Local Equity: This factor aims to capture home bias, meaning that negative performance implies that U.S. equity markets underperformed global markets. For example, equity markets in the Eurozone and UK outperformed the U.S. in April, in part because their March inflation reports were more favorable. The ECB and BOE are now expected to implement their first rate cuts significantly sooner than the U.S.4

- Trend Following: This factor has been having a strong year, up almost 5% through the first quarter. However, Trend Following relies on consistent market themes, making the April shock to equities a meaningful drag on return for the month. Among its currency, fixed income, commodity, and equity components, only equity was meaningfully negative for the month.

Exhibit 5: Trend Following Component Performance

Source: Venn by Two Sigma

- Equity and Interest Rates: Equity and Interest Rates factors both fell for the month. This happened as markets continue to grapple with sticky inflation and higher-for-longer rates in the U.S. More specifically, Equity and Interest Rates factors were down -0.54% and -0.60%, respectively, when markets learned of higher-than-expected March inflation. It is worth noting that these factors have been responding to inflation prints in a similar fashion more often than not. Since 2022, they have moved in the same direction on roughly 70% of the days when the U.S. CPI was released.

Exhibit 6: Equity and Interest Rate’s Performance on the Day of the U.S. CPI Release, Since 2022

Source: Venn by Two Sigma

References

References to the Two Sigma Factor Lens and other Venn methodologies are qualified in their entirety by the applicable documentation on Venn.

This article is not an endorsement by Two Sigma Investor Solutions, LP or any of its affiliates (collectively, “Two Sigma”) of the topics discussed. The views expressed above reflect those of the authors and are not necessarily the views of Two Sigma. This article (i) is only for informational and educational purposes, (ii) is not intended to provide, and should not be relied upon, for investment, accounting, legal or tax advice, and (iii) is not a recommendation as to any portfolio, allocation, strategy or investment. This article is not an offer to sell or the solicitation of an offer to buy any securities or other instruments. This article is current as of the date of issuance (or any earlier date as referenced herein) and is subject to change without notice. The analytics or other services available on Venn change frequently and the content of this article should be expected to become outdated and less accurate over time. Two Sigma has no obligation to update the article nor does Two Sigma make any express or implied warranties or representations as to its completeness or accuracy. This material uses some trademarks owned by entities other than Two Sigma purely for identification and comment as fair nominative use. That use does not imply any association with or endorsement of the other company by Two Sigma, or vice versa. See the end of the document for other important disclaimers and disclosures. Click here for other important disclaimers and disclosures.